Turo car rental – a financial guide

In just under nine years, Turo has quickly dominated the peer-to-peer car rental market. With well over a million rentals with listings in over 2,500 cities as well as over 300 airports, Turo’s sights appear to be now set on disrupting the traditional car rental market by instilling a sense of urgency among industry giants such as Avis and Enterprise to reimagine how car rentals are managed in the 21st century. In this article, we look at Turo – the ‘Airbnb of cars’ – and gauge if it is really worth renting out your car in the long run.

What is Turo?

Turo, like other emerging share-economy companies such as Uber and Airbnb, operates as a peer-to-peer car-sharing platform designed to allow car owners to privately rent out their vehicles out to consumers seeking an easy and (often) cheaper option to rent a vehicle. The Turo peer-to-peer car-sharing model provides the freedom of choice for consumers while also filling the gap for quick and convenient reservations – quite literally at the tip of your fingers.

Turo boasts boundless choice in vehicles as they are not tied to specific manufacturers and models that the larger rental corporations to which they are bound. Turo can offer something for everyone. So, whether you lean towards luxury or eco-environmentally conscious commute – or a balance of both (how about a Tesla Model 3 for 270$ day), Turo offers a wide range of vehicles throughout your selected city.

How Does it Work?

Renting through Turo requires downloading the app on your mobile device. Once you have acquired the app on your mobile device, here’s how it works:

- Creating a Turo account;

- Select your travel dates;

- Find a car in your area;

- Select your budget: prices start around $35$/day to $200+/day for luxury cars;

- Select an insurance plan to cover your trip;

- Submit your rent request — the owner must approve your request.

- If your request is accepted, select a pickup option (some owners will deliver the car to you for an extra charge);

- Meet the owner and get the keys;

- Return the car after your trip is over

Can You Make Money off Turo?

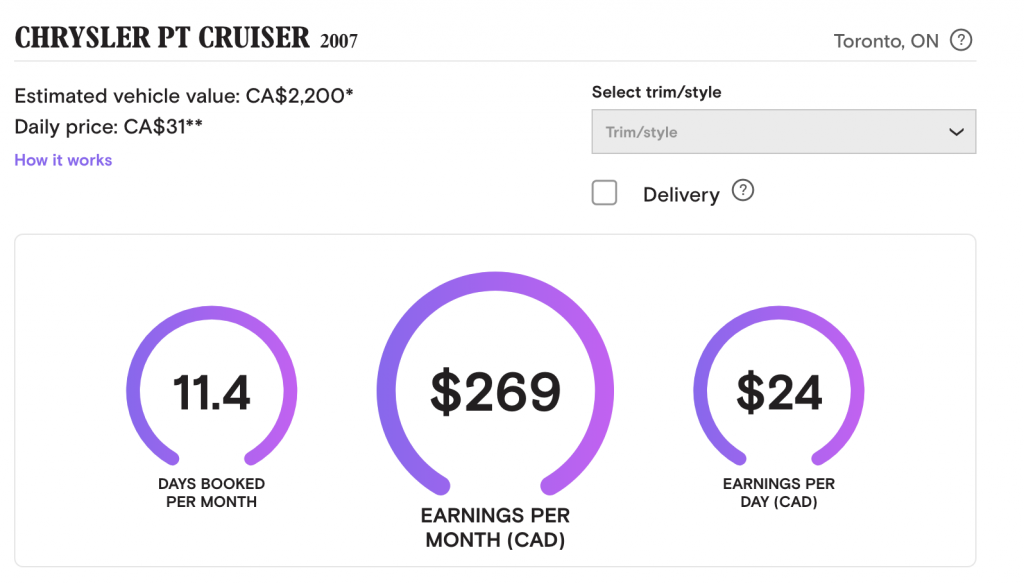

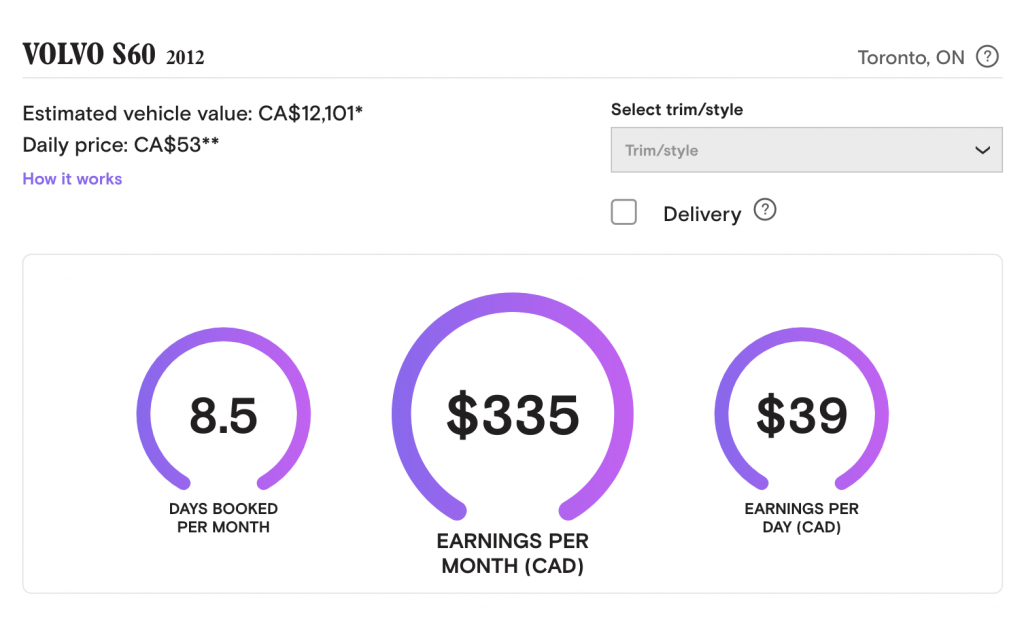

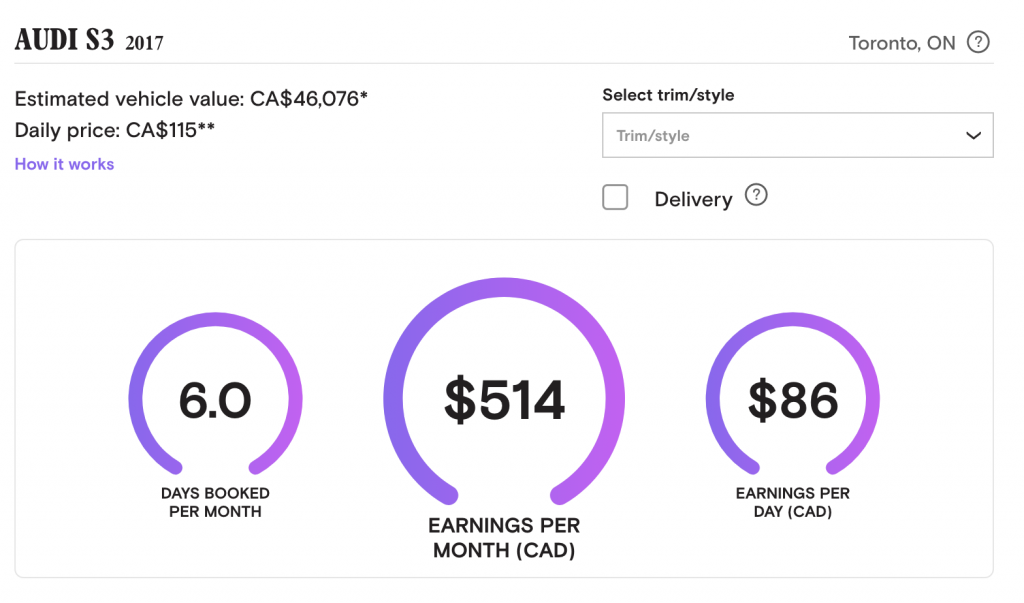

A quick scan will suggest that reports of earnings can vary. Similar to Uber and Airbnb, the amount you can make is really dependent on a number of factors but ultimately rests on how attractive you can make your product. For help with this, Turo provides what they call the “carculator” where you can enter your vehicle’s year, make, and model to get a sense of what you might potentially earn.

Using Turo’s carculator I calculated three different cars to see what I might yield as a lower, mid, and upper range income scenarios:

Lower end: Turo Chrysler PT Cruiser

Mid Range: Turo Volvo S60

High End: Turo Audi S3

While these earnings give you a small sample of what you might expect, Turo also provides tips on how to attract guests and increase earnings such as: making your advert on the Turo app more eye-catching through professional photos, ensuring your availability is generally flexible, and offering features such as delivery service, as well as discounts and extras.

Turo also encourages micro-entrepreneurship with blog posts dedicated to showcasing individuals purchasing a mini-fleet of vehicles with the sole purpose of making money such as a Toronto man who claims that he made up to 100$ a day by renting out his Tesla to strangers across the GTA.

Turo Car Requirements

As a prospective car-owner, and considering Turo, you might want to know that your vehicle must meet Turo’s car requirements. All vehicles must:

- Be registered and located in the provinces of Alberta, Nova Scotia, Ontario, or Quebec;

- Be no more than 12 years old;

- Meet Turo’s insurance requirements;

- Have a fair market value of up to CA$75,000;

- Have fewer than 200,000 kilometres;

- Have a clean (e.g. not a “branded” or “salvage”) title;

- Have never been declared a total loss;

- Meet Turo safety and maintenance requirements; and,

- Abide by Turo’s Exclusivity policy

Are Renters Covered with Turo?

Turo notes that customers do not need their own personal car insurance coverage in order to book a car with Turo. According to Turo:

“liability insurance offered by Turo via its partner Intact Financial Corporation will supplement your existing coverage. Some hosts on Turo have opted to decline a Turo protection plan where they are able to offer commercial rental insurance directly to guests. Guests who book those vehicles are subject to the host’s commercial insurance policy instead and waive Turo’s protection.”

In other words, as a renter, you do not need your own auto insurance policy to rent a car with Turo but you should consider opting for the most comprehensive vehicle insurance package offered at the point of sale as the owner of the vehicle you are renting is already covered through Turo’s Intact commercial insurance policy. In summary, the takeaway for liability insurance with Turo is the following:

- Turo has a liability policy that pays for damage you do to other cars and drivers, but not for damage you do to the car you rent;

- The liability policy generally does not cover your medical expenses;

- Turo protection policies cover collision (the damage you do to the car you rent – not wear and tear);

- Your personal liability insurance covers you as a driver, but your personal collision coverage only covers one car. That means you can’t expect your own personal insurance policy to cover collision damage while you drive a Turo car (in other words, your insurance will not cut it).

As a renter, Turo offers three options under their insurance plan packages: Premier, Standard, and Minimum. Here’s how they breakdown:

Premier Plan

- Liability coverage up to $2,000,000.

- Physical damage to the car covered up to the actual cash value of the car.

- In each case, coverage is primary and your out-of-pocket exposure is limited to $0.

- There is no coverage in any guest plan (i.e., you are fully financially responsible) for mechanical or interior damage.

- The Premier plan is not available for trips booked in Deluxe or Super Deluxe vehicles.

Standard Plan

- Liability coverage up to $2,000,000.

- Physical damage to the car covered up to the actual cash value of the car.

- In each case, coverage is secondary to any other insurance you may already have.

- There is no deductible for supplemental liability coverage.

- For the physical damage protection, once you’ve exhausted your own insurance for physical damage, your out-of-pocket exposure is limited to $500, regardless of fault.

- There is no coverage in any guest plan (i.e., you are fully financially responsible) for mechanical or interior damage.

Minimum Plan

- Liability coverage up to $2,000,000.

- Physical damage to the car covered up to the actual cash value of the car.

- In each case, coverage is secondary to any other insurance you may already have.

- For the physical damage protection, once you’ve exhausted your own insurance for physical damage, your out-of-pocket exposure is limited to $3,000, regardless of fault.

- There is no coverage in any guest plan (i.e., you are fully financially responsible) for mechanical or interior damage.

Decline Coverage

- Liability coverage up to $2,000,000.

- No protection at all for physical damage: the guest is liable for all costs related to physical damage to the vehicle, regardless of fault.

Are you paying the best price for car insurance?

In less than five minutes, you can compare multiple car insurance quotes from Canada's top providers, free of charge.

If you go with a basic package, Turo’s plan will only pay for the minimum liability and you risk paying out of pocket in the unfortunate event of an accident. In short, your level of coverage will always depend on your personal coverage (in the rare event they offer extensive coverages and top-ups to third party insurers) and the plan you select with Turo. If you have a personal auto insurance policy that offers such a premium and you select Turo’s highest level of coverage, chances are that you will be over-insured and pay too much into plans that offer similar coverage. That being said you will still need to complete a Rental Vehicle Insurance Endorsement form or an “Ontario Policy Change Form 27” which provides you with physical damage coverage for vehicles you drive that are not your own – including rental car insurance under Turo. This means that if you cause damage to a vehicle while driving, it will be covered (typically up to a limit of $50,000). The endorsement is – of course – subject to a deductible, and the coverage will include all drivers listed on the policy.

Finally, as a “Canadian host,” you will want to make sure that your personal car insurance provider is recognized by Turo under their list of approved insurance agencies which include, but not limited to: Intact, Jevco, RSA, and Desjardins

Bottom Line

If you are a renter and prefer unlimited selection and convenience over form booking and pricing, then Turo might be for you. If you are a vehicle owner looking to make money off your vehicle, the answer is a bit more nuanced to consider.

For car owners, the consensus in Ontario suggests that if you are not an outlier seeking to rent out a micro-fleet, you need to consider Turo as a service that can provide supplementary income and probably shouldn’t rely solely on income generated through Turo to be able to make your monthly payments. Moreover, some insurance providers might require you to disclose that you are participating in a ride-share program, which could potentially raise your premiums over time.

Overall, it comes to convenience and needs. For renters, Turo’s approach operates as a ‘Uber-style’ service offering a wide selection of cars across selected cities for consumers seeking rentals on an ad hoc and immediate basis. For car owners, if you are looking to make a bit of extra cash while sitting at the office or at home on the weekend, Turo might be right for you – just ensure that you do your homework and maybe shop for new Ontario auto insurance quotes and read up on the fine print on liability.

ALSO READ