GIC Laddering

Reading up on personal finance? Looking for ways to maximize your savings and investments? Instantly compare the best accounts in Canada and boost your ROI.

It’s easy to see why guaranteed investment certificates (GICs) are a part of many investors’ fixed income portfolios. Not only are GICs a low risk investment that come with a guaranteed return, they can also offer some fairly good interest rates – depending on how long you’re willing to lock in your money for, that is.

In general, the longer you’re willing to lock in your money in a GIC, the higher the interest rate you can get. For example, a 1-year GIC term might be worth 1.50% while a 5-year GIC term could be worth 2.50%. In this example, the 5-year GIC term’s interest rate is obviously more appealing, but handing over your money for that length of time isn’t an option for all investors.

Fortunately, if you like the idea of investing in GICs, but don't feel comfortable placing your total investment amount in a long-term GIC, there's another investment strategy you can consider: GIC laddering.

What is GIC laddering?

GIC laddering is a simple way to maximize the return from your GIC investments, without locking in all of your money into one long-term investment.

The laddering process is fairly simple: Start by dividing the total amount you want to invest by five. Take those five smaller amounts and invest them in five individual GIC terms: a 1-year, 2-year, 3-year, 4-year and 5-year. When each term matures, reinvest the new amount (original investment + return) in a 5-year GIC term. And that’s it – just repeat, repeat, repeat.

By laddering, a term matures every year, which means every year you have two options: access some money if you need it, or keep investing. As long as you’re investing in a laddering strategy, your overall annual return rate is expected to be much higher than what you would get if you had invested all of your money in consecutive short-term GICs. Let’s look at an example.

Find the best GIC rates in Canada

Watch your savings grow faster, when you invest your money in the GIC products with the best interest rates

Example of GIC laddering

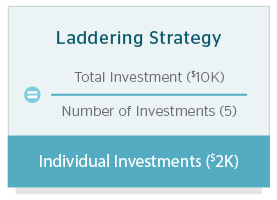

Let’s say you have $10,000 you want to invest in GICs. After searching for the best GIC rates, you choose a lender to invest your money with. From there, the process to ladder your GICs is simple.

Step 1

Divide and invest

The first step is to divide the total amount you want to invest by the number of individual investments you plan to make (5). In this example:

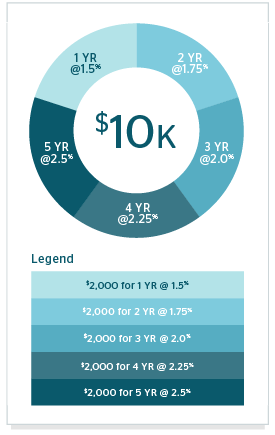

You now have $2,000 to invest in five individual GIC terms, ranging from 1 to 5 years. Using some example interest rates, your investments for Year 1 could look like the pie chart on the right.

If you add up each of those interest rates, and divide the total by the number of investments you made (5), you can see that your average return for Year 1 will be:

Return

That’s an extra 0.50% of interest earned for the year, compared to what you would’ve earned if you had put your entire $10,000 investment into a 1-year GIC term at 1.50%.

Step 2

Reinvest at maturity

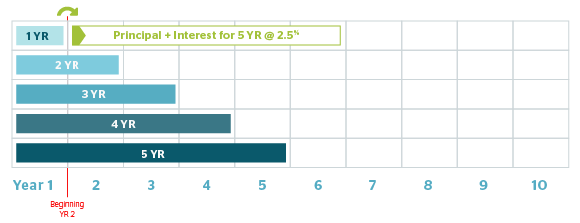

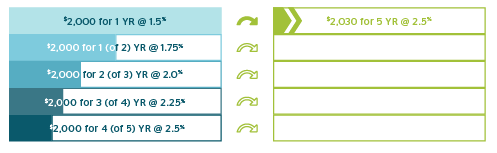

One year later, your 1-year GIC term will mature. After earning 1.50% interest for the year, your $2,000 investment will be worth $2,030.

In the laddering process, every time one term ends, you reinvest that money into a new 5-year GIC term.

If we assume interest rates have remained unchanged, your five investments would then look like this in Year 2:

Beginning of YR 2

If you add up those interest rates again, and divide the total by 5, you can see that your average return for Year 2 would be:

Return

Note that a weighted average return is immaterial in this scenario and renders the same result as the simple interest calculation. The weighted average is calculated as:

- Weighted Average = w1*x1 + w2*x2 … wn*xn where

- w = relative weight (%)

- x = value

That’s an additional 0.70% of interest you would earn in the second year of your laddering investment strategy, compared to if you had put your investment in another 1-year GIC term at 1.50%.

Step 3

Repeat, repeat, repeat

After 5 years, all of your original investments will have matured, and each will now be in 5-year GIC terms. For the sake of this example, let’s assume interest rates and GIC product offerings stayed the same for all those years. If that were the case, your investments would look like this in Year 6 (assuming annual compounding):

Beginning of YR 6

And your average annual return for Year 6 would be:

Return

That’s an entire 1.00% more interest that you would earn that year, compared to if you had been repeatedly purchasing 1-year GICs terms at 1.50%.

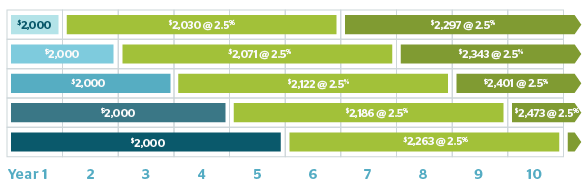

The chart below shows how GIC laddering would affect your overall return, if you maintained this strategy for 10 years.

10,000 Invested in a GIC Laddering Strategy Over 10 Years

After 10 years of GIC laddering, your original $10,000 investment would be worth $12,676; that’s nearly a 27% return.

But what would your investment be worth if you hadn’t used a laddering strategy?

$10,000 Invested in 10 x 1-Year GIC Terms

If you had simply purchased a new 1-year GIC term at 1.50% each year, your $10,000 investment would be worth $11,605 after 10 years; only a 16% return, in comparison.

Benefits of GIC laddering

As you can see, there are some obvious benefits to adding GIC laddering to your investment portfolio:

-

You can maximize your returns – By spreading your money across different GIC terms, you create the potential to earn much more than you would if you only invested in short-term GICs.

-

You can take advantage of rising interest rates – Because one of your investments will mature each year, you will have the opportunity to get the current best rates when you reinvest in a new 5-year GIC term.

-

You can access 20% of your investment every year – Remember that one of your GICs will mature each year, which makes this a somewhat liquid investment strategy. If you find yourself needing a little extra money to pay for an unplanned expense, you have the option of keeping any money from matured GICs.

-

There’s very low risk – The name of the product says it all: it’s guaranteed, so long as you purchased a GIC with a fixed interest rate. So, while your rate of return may be low, you will always walk away with your principal plus any interest accrued.

Risks of GIC laddering

While your risk level is low with almost any GIC, there are a couple of things you should be mindful of1, if you’re considering making GIC laddering part of your portfolio:

-

Returns may not keep pace with inflation - While the example above showed a 27% return over 10 years, that’s still just a 2.7% average rate of return per year. The rate of inflation (which is the rate at which the prices for goods and services goes up or down) in Canada might be low today, but it has been as high as 2.38% over the last 10 years2. If the interest rate on your GIC is lower than the rate of inflation, your purchasing power with the investment when it matures will actually decrease.

-

Variable return GICs may not perform well - This is true for any investment you make, where the return is based on the performance of the stock market. However, since GIC laddering is meant to be a fixed income investment strategy, including products that have a variable return over a fixed interest rate means you’ll run the risk of not coming out ahead.

References and Notes

- These are true for any investment that’s locked in/non-redeemable.

- http://www.inflation.eu/inflation-rates/canada/historic-inflation/cpi-inflation-canada.aspx