Notable News of the Week: August 9, 2013

CMHC limits guarantees for mortgage lenders – Global News

This week, the Canada Mortgage and Housing Corporation (CMHC) notified banks, credit unions and other lenders that they will begin restricting each lender to $350M worth of mortgage-backed securities (MBS) per month. CMHC was given the authority to guarantee up to $85 billion in 2013, as part of the National Housing Act Mortgage-Backed Securities (NHA MBS) program. By the end of July, however, CMHC had already guaranteed $66 billion. To better manage the volumes going forward, CMHC introduced this $350 million cap.

Analysts think that the new cap will make it more difficult and expensive for banks to lend to their customers. Converting loans into mortgage-backed securities was a way for lenders to utilize funds from a broad range of investors and offer mortgages at a lower rate. Without this option, added costs will likely be passed onto customers in the form of higher mortgage rates. TD Economist Diana Petramala predicts that mortgage rates will rise anywhere from 0.20-0.65 per cent, as a result.

ATB dumps posted mortgage rates – Canadian Mortgage Trends

ATB Financial has decided to abandon the long-standing practice of having two sets of mortgage rates: posted rates and discounted rates. This is a big move for the lending institution, as ATB has been using two sets of rates for decades. Posted rates were traditionally used by banks to offer discounts to loyal customers. Now, however, the two sets of rates lead to inefficient discretionary pricing models and complicated interest rate differential (IRD) calculations.

ATB Financial is the first large financial institution to depart from posted rates, as all the other major banks still use this technique. Moving away from posted rates helps both the bank and its customers. Posted rates are often less transparent which could force customers to look elsewhere for a better rate. By only offering one set of rates, there is full transparency and customers can see exactly what is available to them.

Condo ‘softness’ to continue, Royal Lepage says – Yahoo! Finance Canada

According to Royal LePage, the market for Canadian houses is in a position to trend upwards this year, while the condo market will remain slow for awhile longer. Sales volumes and house prices are expected to strengthen in late 2013, while the condominium sector will continue to see “softness” in the short term.

The Chief Executive of Brookfield Real Estate Services believes that, overall, the market is in the late stages of a downward trend. Brookfield’s Phil Soper said, “The low interest rates that Canada has been experiencing are appealing for would-be buyers but consumer confidence hasn’t completely rebounded.” Soper believes that the condominium market can rebound with changes in demography, city planning and customer preferences.

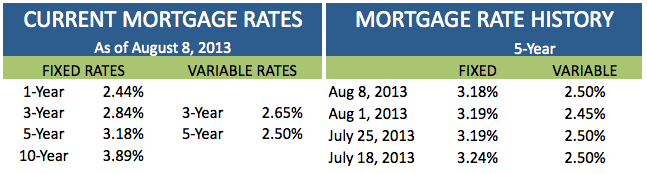

A look at current mortgage interest rates and 5-year mortgage rate history.

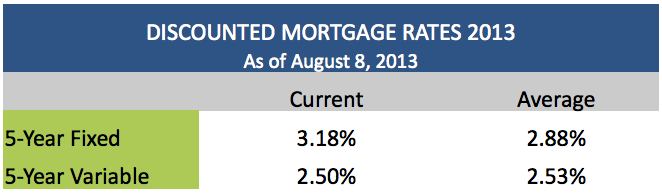

The average discounted mortgage rates in Canada in 2013:

A history of weekly 5-year fixed mortgage rates and 5-year variable mortgage rates.