[Infographic] How to avoid paying car rental insurance

- Skip to: Loss/Collision Damage Waiver Insurance

- Skip to: Personal Accident Insurance

- Skip to: Liability insurance

- Skip to: Personal Effects Insurance

- Skip to: Who Should Buy It?

- Skip to: How Much Is It?

- Skip to: Rental Car Insurance Checklist

Should you pay the extra money for car rental insurance? Rental car insurance could cost you an extra $35-$40 a day for all the different coverages, nearly doubling the price of the rental car. Most rental car agencies wait until you’re at the counter to ask you about insurance, forcing you to make a decision under pressure.

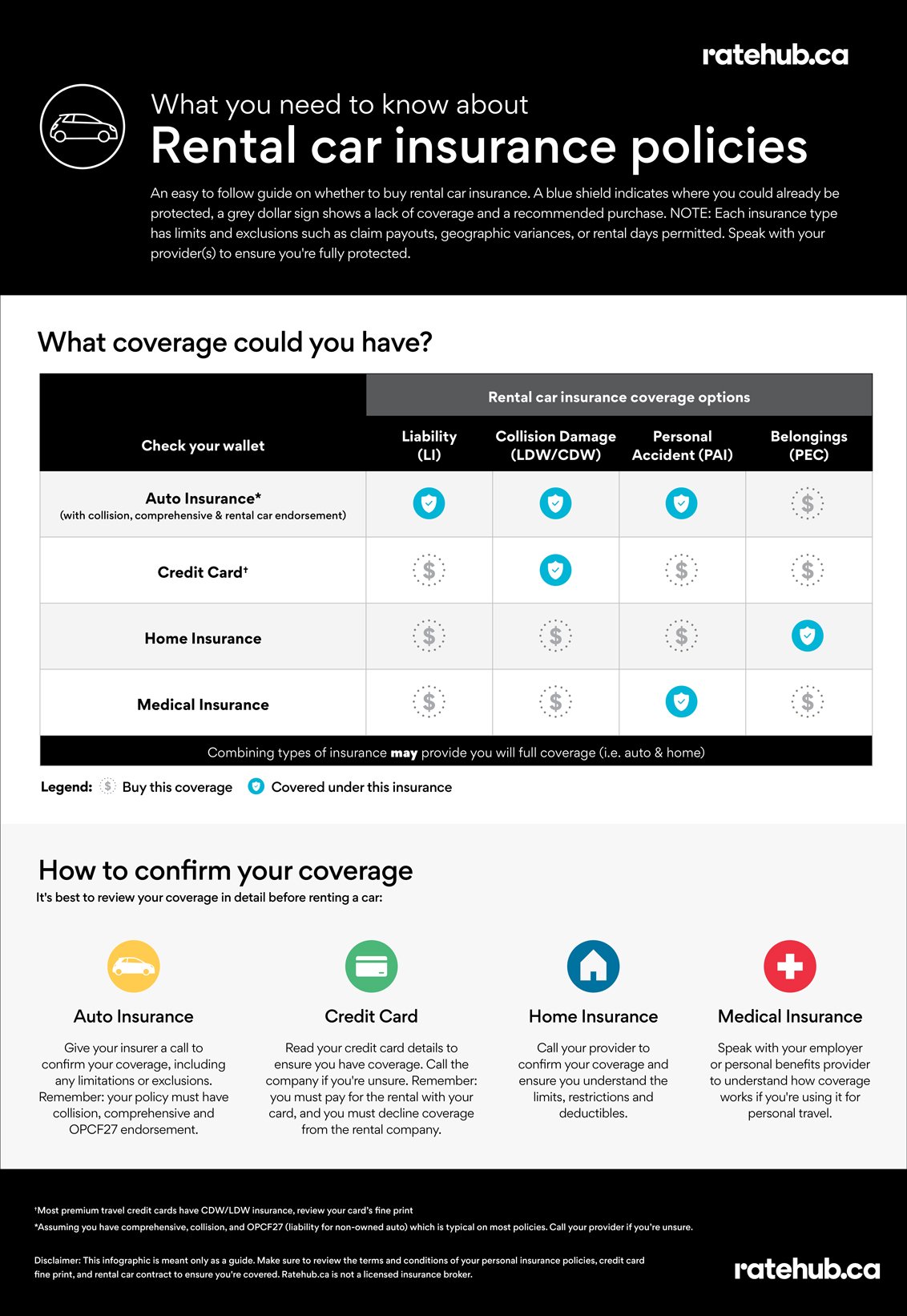

Below, we give you a primer on the 4 different insurance options the rental car agency has on offer and whether or not you’re covered with your current insurance policies or credit cards.

What is the Loss Damage Waiver / Collision Damage Waiver?

The Loss Damage Waiver (LDW) and/or Collision Damage Waiver (CDW) covers you against theft and collision of the rental car. An LDW/CDW is not an insurance policy, by signing on the dotted line, you’re paying the car rental agency to waive its right to pursue you for damages or losses.

How to avoid paying LDW insurance / CDW insurance

The simple answer is no, you don’t need to buy this coverage. But, you’ll need to make you’re covered appropriately before you turn it down.

Personal Auto Insurance Policy

First, while standard on most car insurance policies, you need to ensure you have an OPCF27 (Ontario Policy Change Form) endorsement. OPCF27 allows you to drive a non-owned automobile. You’ll need OPCF27 if you want to port over your own car insurance to cover the rental car.

You’ll also need to have comprehensive insurance on your policy, which again, while standard on most policies, it’s still optional. If the rental car is stolen or damaged while it’s not being driven, your comprehensive will cover this portion of the insurance.You can waive the LDW.

The Collision Damage Waiver (CDW) can be waived if you have OPCF27 and collision coverage on your insurance policy. This covers the rental car in case of collision. It doesn’t cover other people’s property, like their cars – more on this later.

Both comprehensive and collision insurance are popular options, but not standard or automatic on your policy. You still need to opt-in when reviewing your current policy or when shopping for Ontario car insurance quotes.

Credit Card

Alternatively, you can often use your travel rewards card or cashback credit card to forego this insurance. Visa and American Express credit cards cover you for at least $65,000, or about the cost to replace the car. The same applies if you have a gold, platinum, world or elite Mastercard.

Of course, as with most insurance, there are some stipulations, limitations, and exclusions.

Things to know about loss damage waiver and collision damage waiver

- Any reckless driving (DUI, speeding, etc.) and you could void insurance from any of the providers

- If you’re using your credit card, you need to waive the LDW/CDW insurance on the car rental contract and you need to pay for the full rental using that credit card

- If you’re renting outside of North America, it’s best to call the number on the back of your card to get the finer details of protection. (e.g. MasterCard doesn’t cover Ireland, Israel, or Jamaica)

- Rent cars that are less than $65,000 to replace (since that’s what you’re covered for)

- How long can you rent the car – 15 days is standard, but some cards offer 48 days.

- Understand the restrictions and limits of your coverage (size of the car, location of travel, towing services, etc.)

LEARN MORE ABOUT CREDIT CARD RENTAL CAR INSURANCE

What is Personal Accident Insurance?

Personal Accident Insurance (PAI) provides accidental death and dismemberment coverage to the renter and their passengers. Each rental car agency has a different benefits package for what they cover but typically the driver is covered up to $100,000 and $10,000 for each passenger.

Other coverages could include ambulance charges or other medically-related expenses like rehab or home care.

How to avoid paying for personal accident insurance

If you have your own car insurance policy, then you’re covered if you have OPCF27 as an endorsement. It’s standard on most, but not a requirement, so call your provider. Across Canada, this is also known as Accident Benefits and is a requirement on all auto insurance policies. It covers medical benefits as a result of a collision, whether it was your fault or not. It includes medical costs and additional recovery costs such as rehab, income replacement, and attendant care, as required.

If you don’t have your own insurance, then you should pay for this coverage. Your credit card does not cover injuries related to car crashes unless you have the BMO World Elite Mastercard. If you have life insurance, or a great health benefits plan with short or long term disability, you can opt to waive this fee, but first, understand what you’re giving up.

For instance, if you get injured in the US, who pays for hospital care? Who pays to get you back home? Once you’re back home, can you work? If not, how will you deal with the lost income if you need to take a leave from work?

Are you paying the best price for car insurance?

In less than five minutes, you can compare multiple car insurance quotes from Canada's top providers, free of charge.

What is Liability Insurance for rental cars?

Liability insurance (LI) protects you from being held liable in a collision. If you cause a collision and injure another person, you will want to have liability insurance. Liability will cover the costs associated from the crash including the vehicle and medical benefits to anyone injured.

How to avoid paying for Liability with your rental car

Third-party liability insurance is required on all personal car insurance policies in Canada. If you have an auto insurance policy, with OPCF27, then you don’t have to pay. However, it’s important to know the limits in your contract. Every province and territory have mandated minimum third-party liability coverage of $200,000 – except in Quebec where the minimum is $50,000. Often, drivers will upgrade this coverage to $1 or $2 million to ensure they have enough.

Your credit card does not cover you for third party collision. If you need this coverage, it’s best to buy protection from the rental car agency.

If not, and you’re in a collision – you’ll pay to replace the car and cover any medical costs for the driver and their passengers.

What is Personal Effects Coverage for rental cars?

Personal Effects Coverage (PEC) or Personal Effects Protection (PEP) covers your personal belongings within the rental car, usually up to a stated limit and will often have an associated deductible. Each passenger may receive up to $500 coverage, with a $25 deductible per claim submitted, up to a maximum of $1500.

How to avoid paying for PEC insurance with my car rental?

If you have homeowners insurance or renters insurance, then you’ll have contents insurance and you can waive this fee. You should know your limits before saying no. For instance, unless other specified, there are limits to your personal belongings. Let’s say you’re carrying bicycles, and someone steals them, your home insurance may only cover each bike for up to $1,000. If your bicycles are worth more, consider adding an extended bicycle endorsement when shopping for home insurance quotes or speaking with your provider.

If you use the BMO World Elite MasterCard, it covers personal effects for up to $1,000 per person, with a maximum payout of $2,000. Let’s say someone robs your laptop, you can make a claim on the card.

If you don’t have any home insurance, you can still opt-out of this insurance, but your belongings are at risk.

Are you looking for the best home insurance rate?

In less than 5 minutes, you can compare multiple home insurance quotes from Canada's top providers for free. Comparing rates online could save you hundreds of dollars.

Who should purchase car rental insurance?

While many financial experts agree you shouldn’t use the rental agency’s insurance, there are instances where you should consider buying their insurance to avoid financial disaster.

- If you don’t own a car and don’t have your own car insurance

- You’re a high-risk driver and it’s not worth another claim

- The deductible on your CDW is $1,000 or more (and you don’t have the right credit card)

- If you’re travelling for business, don’t assume your personal policy has you covered

- Renting sports cars, luxury, or specialized vehicles, better to buy the agency insurance

- If you only have the minimum liability car insurance

- International travel (outside of North America)

How much does the insurance for the rental cost?

Based on the 4 types of insurance offerings, if you took all of them, it could cost you $35 to $40 per day over and above the cost of the rental car. If you rent for 1 week, that could cost you around $350 in extra charges that you didn’t need to pay in the first place. It’s smart to understand your coverages and fill gaps as needed. Every agency has slightly different rates for different options. Sometimes, there are tiers within the options. Here’s a rough guide.

- Loss Damage Waiver: $9 to $30 per day

- Liability coverage: $15 to $30 per day

- Personal Accident Insurance: $7 to $10 per day

- Personal Effects Coverage: $2 to $5 per day

The Bottom Line

Create a checklist (use the one below), call your credit card company and, if you have one, your insurance provider. Ask them what coverages you have or where you might have gaps in your coverage. Ask if you can add additional coverage to your existing policy, even temporarily. The most important part is to be protected, then, it’s making sure you’re not paying twice for coverage you already have at your disposal.

RENTAL CAR INSURANCE CHECKLIST

(you can download this list here for easy printing)

Questions to ask yourself

- Is my trip for business or personal?

- Will I be renting for a week or longer?

- Is my rental part of a travel package and if so, is insurance already included?

- What kind of medical benefits do I have? Short term disability, life insurance, etc.

Questions to ask your auto insurance company

- Do I have OPCF27?

- Do I have collision and comprehensive?

- Does my current policy cover me for this rental (location, length of time)

- Do I have to decline coverage at the rental counter?

- Tell me about my accident benefits, can I waive the personal accident insurance?

- What is my liability amount? ($200,000, $1-$2 million)

- Does my policy cover administrative costs, loss of use, or other related expenses?

Questions to ask your credit card company

- Can I use the card for collision or loss damage waiver insurance?

- What are the stipulations around using the card for this insurance?

- Are there any extra coverages with your credit card such as personal effects insurance?

Questions to ask your home insurance company

- What are my contents insurance limits?

- Should I take out an additional endorsement for specialized goods?

Questions to ask your medical insurance (or benefits plan)

- Am I covered if I travel abroad?

- Do you cover all related costs (ambulance charges, hospital stays, etc.)

ALSO READ