What is the Penalty if I Break My Mortgage with Tangerine?

If you’re locked into a mortgage term then decide to either refinance your mortgage, transfer it to another lender, or sell your house or condo, you need to know there will be a penalty that follows. The prepayment penalty, as it’s known, is your lender’s way of making you pay them some of the interest charges they would lose by letting you break your mortgage contract early – and it’s not always cheap.

If you have a Tangerine Mortgage and are considering breaking your mortgage before the term is up, here’s how your penalty will be calculated.

What is a prepayment penalty?

A prepayment penalty is a charge issued to you by a lender if you break a mortgage with them. A mortgage is a financial contract, and the prepayment charge is your mortgage provider’s compensation for you leaving early. Because there are several variables in the calculations, prepayment penalties can vary greatly, even from the same lender.

Looking to refinance your mortgage?

Check out the lowest interest rates available right now!

Calculating your Tangerine mortgage penalty

Even though all the banks are supposed to host their own prepayment penalty calculators now, they often ask for information that isn’t readily available and surround the tool with jargon that can leave even the most educated borrower confused. In seeing this, we decided to take on the responsibility of calling every bank to find out how their penalties are calculated and then building a mortgage penalty calculator of our own.

First, depending on what type of mortgage rate you have (variable or fixed), Tangerine will charge you one of two fees:

- Three months’ interest, or the

- Interest rate differential (IRD).

If you have a variable rate mortgage, your prepayment penalty will be the equivalent of three months’ interest. If you have a fixed rate mortgage, however, you have to pay the greater of the two fees. Here’s how they work.

Method 1: Three Months’ Interest

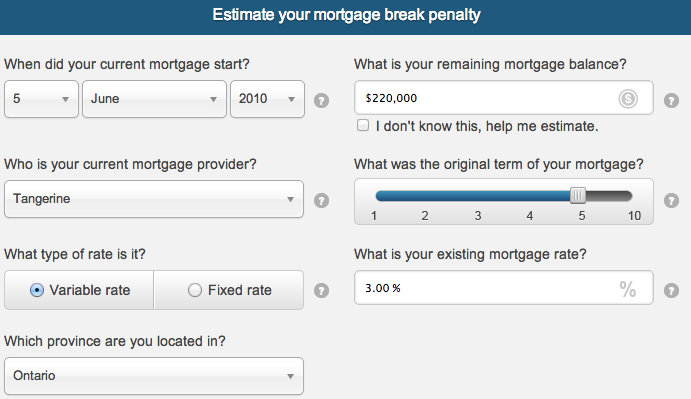

Three months’ interest is exactly what it sounds like: the amount of interest you would’ve paid Tangerine if you stayed in your current mortgage term. While some lenders use their Prime rate in this calculation, Tangerine uses your current mortgage rate. Since their current 5-year variable rate is 3.00%, we used that number in this example.

To calculate three months’ interest, Tangerine would multiply the current mortgage rate (we used 3.00%) by the outstanding mortgage balance ($220,000 in this example) and again by 0.25 (represented as 3/12 for the three-month period out of the year). Because this example is in Ontario, Tangerine would also charge a discharge fee (explained below).

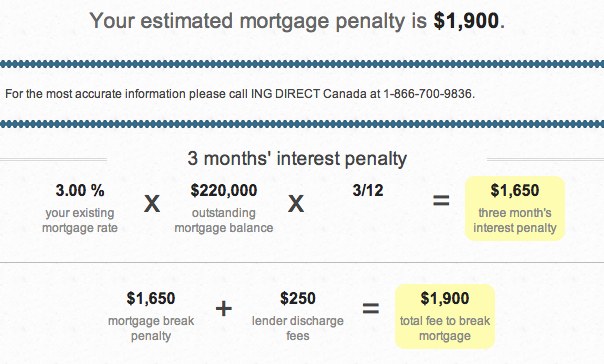

In this example, because you had a variable rate mortgage, Tangerine would charge you the three months’ interest penalty of $1,650. Tack on the $250 discharge fee applied to all Ontario mortgage holders and your total prepayment penalty would be $1,900. But what would the penalty be if you’d had a fixed rate mortgage instead?

Method 2: Interest Rate Differential

The interest rate differential (IRD) is a calculation used to determine how much interest a bank would lose by letting you break your mortgage term early and then making you pay it. To calculate the IRD, Tangerine looks at your current mortgage rate, how many months are left in your term, and the mortgage rate they could charge someone today for a new mortgage term that’s similar in length to the remainder of your term.

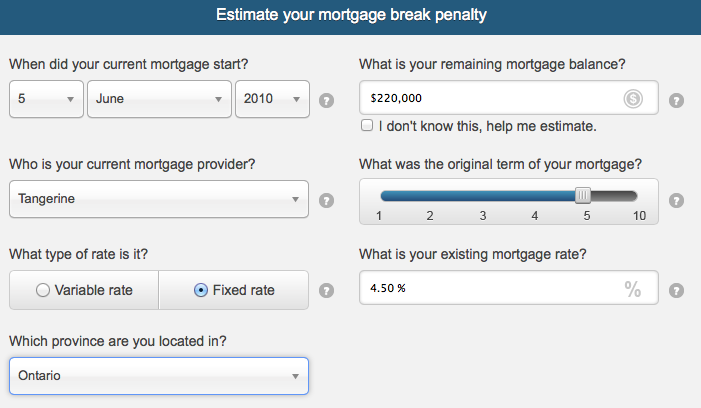

If we use the same numbers from our example above, we can see the remaining balance of your mortgage is $220,000 and you have 11 months left in your mortgage term. From there, Tangerine would determine which of their mortgage products someone would need to get today, in order to make up the remainder of your term (in this case, it’d be a 1-year fixed rate mortgage term).

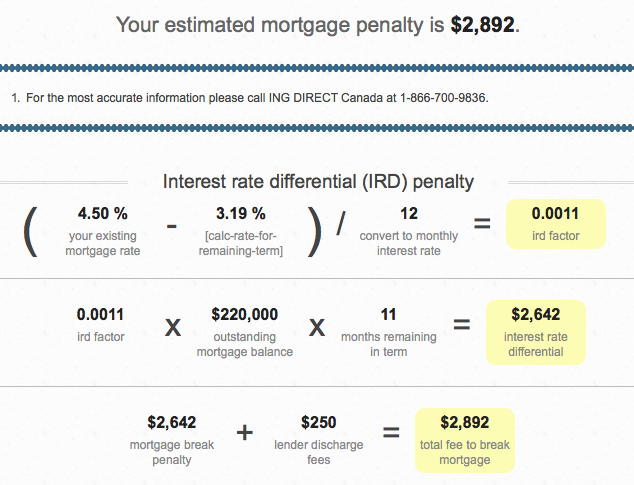

To calculate the IRD, Tangerine would first find the difference between your current mortgage rate (4.50%) and today’s rate for a 1-year fixed mortgage (3.19%). After that, Tangerine would divide the difference by 12 months to determine the IRD factor. The IRD factor is then multiplied by the remaining balance of your mortgage and again by how many months are left in your term, to determine the IRD – or the amount of interest they’d be losing by letting you break your mortgage term early. And because this example is in Ontario, Tangerine would also charge a discharge fee (explained below).

In this example, because you had a fixed rate mortgage, Tangerine would charge you the greater of three months’ interest or the interest rate differential (IRD). Since we know three months’ interest was only $1,900, you would have to pay the IRD of $2,892.

Looking to refinance your mortgage?

Check out the lowest interest rates available right now!

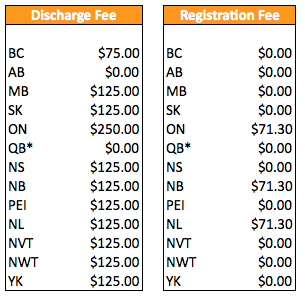

Other Tangerine Penalty Fees

Even though our calculator gives a good estimate of what your prepayment penalty will be, there may be other fees involved. The first is a discharge fee, which we’ve included in our calculator. The fee is charged for the act of having to discharge your existing mortgage from Tangerine and it changes from province-to-province. The second charge is a registration fee, which is charged for the act of having to register the title of the home in your name again. Tangerine only charges a registration fee in three provinces.

*Note: Residents of Quebec pay these fees through a notary (real estate lawyer), instead of through Tangerine.

Tangerine Prepayment Privileges

If you want to try to lessen your prepayment penalty, you could take advantage of Tangerine’s prepayment options. Tangerine will let you increase your original monthly mortgage payment amount by 25% once a year and/or make a lump sum payment of up to 25% of your original mortgage amount on any regular payment date. If you made a lump sum payment right before breaking your mortgage, you could potentially lower your prepayment penalty by a substantial amount.

The bottom line

Breaking your mortgage is a big financial decision and can have major financial implications, as you can see! That being said, don’t be frightened by a high prepayment penalty. This penalty is often worth paying if you’re able to refinance your mortgage with a lower interest rate. Refinancing also gives you some other options with your mortgage that might be worth paying for.

Whatever you decide to do, do it with your eyes open. Tools like our mortgage affordability calculator and mortgage payment calculator are a good first step, but don’t be afraid to get in contact with a licensed mortgage broker to go over your options.

Also read: