What if My Co-Purchaser and I Don't Both Qualify as First-Time Home Buyers?

Image: http://www.pallspera.com

If you’re a first-time home buyer, you may or may not be aware of some of the credit and rebate programs that are available to you. On top of the Home Buyers’ Plan, which I’ll talk about in this post, there are a number of federal and provincial programs that can help you not only get into the market but keep some of your money in your pockets too. Each program comes with its own set of qualification requirements, which are pretty easy to understand. However, things can get tricky if you’re buying a property with someone else (spouse, partner, family or friend) and only one of you is a qualified first-time home buyer.

This is the situation Ratehub.ca’s CEO, Alyssa Richard, is currently in with her boyfriend. He’s purchased a home once before, so is no longer eligible for any of the first-time home buyer programs in Canada. However, they are now looking at purchasing a home or investment property together in 2014, and what they discovered about Alyssa being a first-time home buyer in Toronto is what inspired this post! To find out how this situation could affect buyers across the country, I decided to do a little digging and map out everyone’s options.

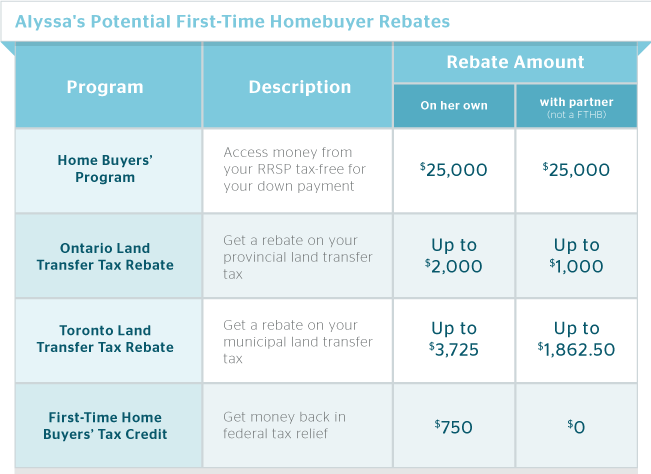

Note: The rebate amount for the Home Buyers’ Program has now increased to $25,000 per buyer.

Federal Programs

Let’s start by going over the First-Time Home Buyers’ Plan (HBP). Every Canadian who meets the eligibility requirements for the HBP is able to withdraw up to $35,000 tax-free from their RRSPs to use as a down payment. If only one of the two buyers is a first-time home buyer, they can still withdraw this amount, so long as they have not lived in a home owned by the other buyer within the past four years. That’s good news!

But then there’s the First-Time Home Buyers’ Tax Credit (HBTC), which is part of Canada’s Economic Action Plan. As long as you can show $5,000 in eligible expenditures (including land transfer tax), you will receive a $750 rebate with your income tax return. To qualify, neither you nor your co-purchaser can have lived in a home that one of you owned in the year of your home purchase or any of the four preceding calendar years; if you have, you’re out of luck.[1] (Special rules apply for those who are eligible for the Disability Tax Credit.)

Provincial Programs

Now let’s talk about all the different provincial programs and rebates for first-time buyers.

In Ontario, even if one buyer has bought before, the one who has not can still claim half of the Ontario Land Transfer Tax Refund for First-Time Home Buyers. The refund helps first-time home buyers recover some of the cost of the province’s land transfer tax, up to a maximum of $2,000 – or $1,000 if only one purchaser is a first-time buyer.

In Toronto, all buyers are faced with a double-whammy – a municipal land transfer tax (MLTT), as well as the provincial land transfer tax. Fortunately, qualified first-time buyers are eligible for a rebate of the MLTT, up to a maximum of $3,725.

“With the provincial and municipal rebates combined, there’s $5,725 available [to Toronto first-time homebuyers],” explained Toronto mortgage broker James Laird. “If only one is a first-time home buyer, they can still claim half. People typically aren’t clear on that.”

This piece of news is what prompted Ratehub.ca and I to do a little digging. In Alyssa’s situation, purchasing a home in Toronto with her boyfriend who has already owned once before doesn’t leave her empty-handed. Here’s a list of the potential rebates she could claim by purchasing a home on her own as a qualified first-time home buyer compared to purchasing with her boyfriend who is not.

Elsewhere in the country, both purchasers have to be first-time buyers in order to qualify for provincial rebates.

For example, the Nova Scotia First-Time Home Buyers' Rebate helps first-time buyers get back 18.75%, up to a maximum of $3,000, of the provincial portion of the HST on newly-constructed home purchases. Neither of the two buyers who will occupy the home can have owned a home in Canada in the last five years.[2]

A non-refundable tax credit was introduced as part of the Saskatchewan budget of 2012, based on an amount of $10,000 for first-time home buyers. This provides a tax credit of up to $1,100, based on the lowest Saskatchewan personal tax rate[3]. To be eligible for this credit, neither you nor your co-purchaser can have owned and lived in another home anywhere in Canada, in the year of your home purchase or any of the four preceding calendar years.

Like Ontario, first-time buyers in Prince Edward Island are subject to a property transfer tax. Unlike Ontario, if one of the two buyers has owned a home before, neither is eligible for a rebate of the tax[4].

Similarly, buyers in British Columbia also face what can be a hefty property transfer tax. And while one buyer having owned a home before strips away any chance of a rebate for the other, there are potential exemptions in place for this tax if you are considered a first-time buyer and meet certain conditions[5]. One option is to put both names on the title, but adjust the amount of ownership for each party to keep the tax as low as possible.

“The party who is a first-time buyer would register the property 99% in their name and the party who has owned before would register the property 1% in their name,” explains Vancouver mortgage consultant Karen Gibbard of Gibbard Group Financial. “This way, the two buyers can maximize the exemption, if the other qualifying criteria is met, and only pay the tax on the 1% that the non-first-time buyer owns.”

Another option is to put the person who is not a first-time buyer as a guarantor on the mortgage, but not on the title. Keeping the first-time buyer on the title means that person will qualify for the full exemption – but this option isn’t for everyone.

“Clients proceeding with this option need to give it serious consideration,” Gibbard says. “If only one person is going on title, the clients should make sure there is a will in place, and potentially life insurance. If something unforeseen happens and the person on the title passes away, there could be probate taxes payable that will be based on the value of the real estate.”

Vancouver real estate lawyer Tony Spagnuolo agrees. “There are estate planning issues and also family relations issues that could come up [with this option].”

The bottom line: Just because one of two purchasers has owned a home before, that doesn’t mean the first-time buyer is out of luck. You may still be eligible for some of the federal and provincial first-time buyer credit and rebate programs available. Even if you can only claim half of the amount, it’s worth doing so to get a little money back in your pocket. Take the time to do your due diligence and talk to your mortgage broker before signing for those keys.

This post was written by freelancer Gail Johnson for Ratehub.ca.

[1] http://actionplan.gc.ca/en/initiative/first-time-home-buyers-tax-credit

[2] http://www.novascotia.ca/snsmr/access/land/first-home-buyers-rebate.asp

[3] http://www.gov.sk.ca/news?newsId=6438307e-7045-4653-806a-02941d19b4c3

[4] http://www.taxandland.pe.ca/index.php3?number=1037867&lang=E

[5] http://www2.gov.bc.ca/gov/topic.page?id=BBD16E2D7C1841A7BBD420E3AC5380F1#qualify

Also read: