The Fed’s Taper and its Effect on Canadian Mortgage Rates

Flickr: rlinger

Back in November, “selfie” was crowned the word of the year for 2013 by Oxford Dictionaries. Of course, it’s a term that has significant mainstream appeal so the honour makes sense. Had there been a separate category for economics, however, surely the word “taper” would have finished first, as the Financial Times suggested.

Unlike the selfie, though, the taper’s significance isn’t limited to poor online dating photos and world leaders taking pictures of themselves. Selfies will never affect Canadian mortgage rates, but the taper already has.

Quantitative Easing and the Taper

Before going any further, a brief explanation of the taper is in order. In the midst of the financial crisis, the Federal Reserve – the U.S. central bank – lowered its short-term overnight interest rate all the way to zero, and it did not stop there. With the goal of lowering longer term interest rates, which are set by the market and not directly by the central bank, the Fed started purchasing vast quantities of U.S. government bonds and mortgage-backed securities in a program known as quantitative easing.

In doing so, the Fed effectively created new money and took bonds off the market and onto its balance sheet, with the goal of lowering long-term interest rates. The Fed actually pursued a few rounds of quantitative easing, eventually taking the Fed’s balance sheet to just over $4 trillion, from roughly $800 billion pre-financial crisis.

By the first half of 2013, the central bank started making noises about “tapering off” the program. After some false dawns, the actual taper was announced in December.

Tapering in this context does not mean reversing what has already been bought, but rather “buying less” in the future. Specifically, the Fed will buy $75 billion of debt securities in January, with the aim of further reducing the purchases in future months.

What Does this Have to do with Canadian Mortgage Rates?

First, it’s important to understand the effect the taper has had on U.S. long-term bond yields. By purchasing large amounts of bonds, quantitative easing aimed to suppress long-term bond yields (bond yields move inversely to prices), so any taper would seem to put upward pressure on them.

(Counterintuitively, long-term U.S. bond yields actually rose during episodes of quantitative easing. For a [technical] explanation of why this happened, see this commentary by Swiss money manager Franz Lischka.)

Even though the actual taper was only made official last month, the market started pricing it way back in May. As Michael Dolega, Senior Economist at TD Economics noted last summer, “The 10-year Treasury yield soared from roughly 1.65% before taper talk to about 2.80% in late August”.

Today, they sit at 2.86%.

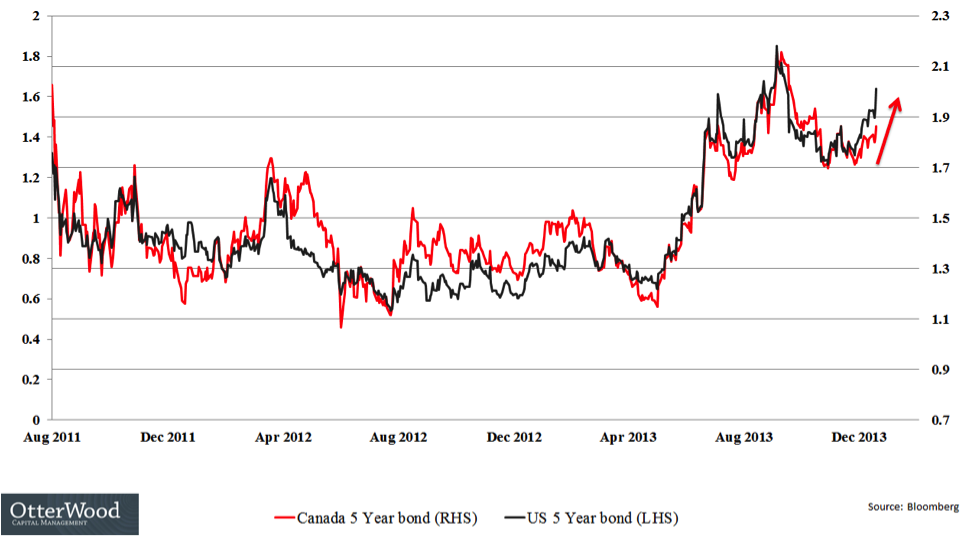

Importantly, as the following chart from Otterwood Capital below points out, U.S. and Canadian bond yields tend to follow each other pretty closely. Dolega explained via email that, “Canadian rates tend to track U.S. rates due to the high level of integration of their economies and an implicit relationship in monetary policies”.

Moreover, the U.S. market acts as something of a “price setter” for the Canadian market, thereby leading the way. Generally speaking, higher U.S. bond yields will push Canadian rates higher, too.

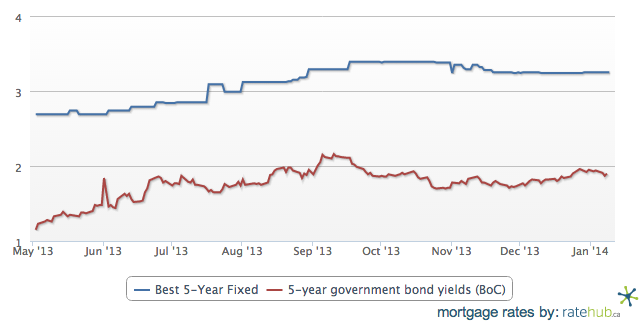

To complete the link, recall that Canadian mortgage rates are heavily influenced by longer term Canadian bond rates. As this chart from Ratehub.ca shows, 5-year fixed mortgage rates have also risen substantially since last May:

Putting this all together:

- The expectation of the taper led to higher U.S. bond rates….

- …which led to higher Canadian bond rates…

- …which fed through into higher Canadian mortgage rates.

A Curveball in 2014?

Overwhelmingly, market participants expect U.S. bond yields to keep rising in 2014, as a result of an (allegedly) stronger U.S. economy and further (expected) tapering by the U.S. Federal Reserve. This would in turn push Canadian mortgage rates up even further.

Case closed? Not quite. What if current investor expectations are wrong?

Another scenario is very possible and bears considering. Should investors come to the realization that the U.S. economy is actually weaker than they currently perceive, they may start to believe that the taper will be abandoned and that short-term interest rates will stay near zero for longer. A taper-reversal could, in the short-run, send yields back down again sharply. In keeping with the process we described above, this would translate into lower Canadian bond yields and lower Canadian mortgage rates.

If history is any guide, any new round of quantitative easing could cause investors to flee U.S. Treasuries, fearing future inflation. In this regard, it’s worth noting the lament of a former Fed official who told the Financial Times last year that, “We are looking at perpetual quantitative easing”.

Indeed, the big story of 2014 might be just how overblown all the 2013 taper talk really was.

This post was written by freelancer Andrew Hepburn for Ratehub.ca. Andrew is also a contributing writer at Maclean’s, Canadian MoneySaver and Business Insider. You can follow him on Twitter.