Ratehub.ca Banking Behaviour Survey Results

At Ratehub, we believe strongly in our mission of helping Canadians make smarter financial decisions. In order to do this, we need to understand more about how and why Canadians make the financial decisions they do.

We recently conducted a survey of over 1,100 Canadians on their beliefs and banking behaviours. A survey sample of this size is a considered an accurate representation of Canada as a whole, plus or minus 3%.

There was a lot of data covered, but here are a few of the highlights.

We rely on family and friends for financial advice – and that comes with a risk

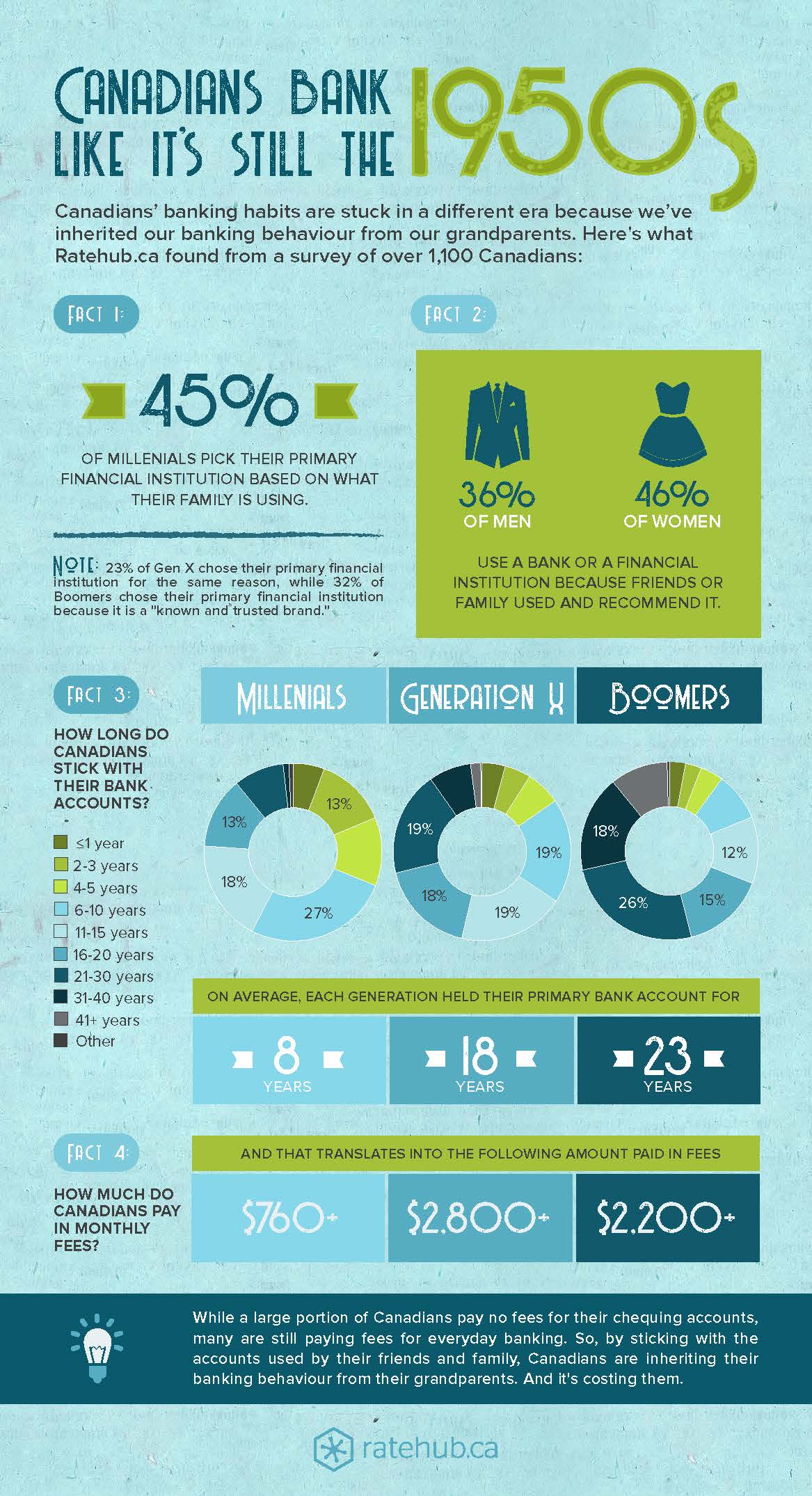

On the whole, 36% of men and 46% of women use a bank or financial institution because a friend or family use and recommend it.

On the surface, this sounds like a perfectly fine way to learn about banks, but this statistic gets a bit worrisome when we look at how long people have held their accounts.

The average millennial in our survey had their account for more than 6 years, with some users in the sample having the same bank account for virtually their entire lives. About 45% of millennials pick their primary financial institution based on what their family is using.

However, the trend of holding onto accounts for extended periods doesn’t stop at millennials. GenX survey respondents held their primary bank account for an average of between 6 and 30 years. Baby Boomers in turn held their account of an average of between 16 and 40 years, with some going back well over 40 years. We don’t break down for older generations, but there’s no reason to believe the trend doesn’t continue beyond this point.

This means that depending on your age, you could theoretically be banking at the same location as your grandparents (or even great-grandparents).

The risk here is that when people stay for decades with the same financial institution they can lose touch with the other account options that exist. Someone who has had the same bank account for 40 or 50 years is rarely aware of the other features current bank accounts can offer.

While your family and friends can be a great source of advice, you should always look at your bank account options on your own as well. Saving a few dollars in fees by getting a free chequing account, or earning a percentage point or so better in your savings account can add up to a massive dollar value over your lifetime.

How does this work?

Let’s say that your parents pay $15 per month in fees on their bank account. They give you some advice and you pick an account that charges $10 per month from the same bank, thinking you’ve found a good deal.

Now, on the surface you do have a good deal. You pay lower fees than your parents and will save money over the long run. However, you chose the same bank as your parents because that’s the one they had experience with. If you had switched to completely different bank you might be able to get a no-fee bank account Tangerine chequing account, saving you $10 per month. There are other no-fee providers as well, so we recommend you shop around.

Looking for a chequing account?

Check out our chequing account comparison tool

The $10 per month difference might not seem like a lot, but it adds up over time. If your account could earn 2% in interest, that $10 per month adds up to $1,327.20 over a 10-year period. If you hold that same account for 30 years like your parents might have done, the difference grows to $4,927.25.

That’s almost $5,000 you could miss out on by not shopping around., and that’s not counting any benefits from sign-up bonuses or other features you would regularly use. Doing your research can pay off in growth for your bank account.

Men hunt for deals, and that seems to pay off in the long run

Men and women act differently. This should come as no surprise, but it does come at some cost.

Men are more likely to sign up for a new bank account based on a promotional offer (12.79% for men vs. 8.85% for women). This might not seem like a large difference, but there are a number of bank account promotions right now offer free movies, merchandise, or even free money.

The financial differences go beyond promotions and sign-up gifts:

- Men are more likely to choose financial products based on rate comparisons (35.82% of men vs. 22.6% for women)

- 20.9% men vs. 10.17% women choose financial products based on print or online ads

- 34.12% men vs. 27.12% women choose financial products based on promo offers

The longer-term impact of this is that men are more likely than women to pay no fees on their account:53.73% for men vs 42% for women.

This means that women are getting fewer promotions and paying more fees for their accounts. Over time, this can add up to a significant change in the amount of money women can save when compared to their male counterparts.

This isn’t an insurmountable barrier though. Comparing rates and shopping around for the best chequing account, savings accounts, and GIC rates can be easier than you think, and the results are certainly worth the effort.