Notable News of the Week: July 5, 2013

Rising rates creating increasing dilemma for homeowners – Financial Post

For the last couple of years, locking in your mortgage at a record-low 5-year or even 10-year fixed rate was an easy decision. Today, however, rising rates are causing an interest rate dilemma not seen in years. With 5-year fixed rates rising to as much as 3.5%, more buyers are considering going variable where the average 5-year rate being offered is around 2.6%. Canadians can blame the U.S. Federal Reserve for easing up on its bond buying program. As a result, bond rates have climbed and mortgage rates are following suit.

Unfortunately, it’s just another reason first-time buyers may be pushed out of the market. “It’s hurting them but also benefiting the rental market,” said Benjamin Tal, Deputy Chief Economist with CIBC Markets. On the other hand, for those who can still afford to buy, rising rates have resulted in a surge in the housing market. According to Tal, “the surge in the housing market we are seeing happens every time there is a fear of rising rates — consumers try to get into the market before it’s too late.”

Toronto’s soaring condo market ignites fears of a U.S.-style crash – The Globe and Mail

Liberty Village has become one of the hottest places to live in Downtown Toronto, with new condominium projects popping up non-stop over the last five years. Currently, more than 55,000 condo units are under construction in Toronto, many of which are located in Toronto’s condo alley, which begins in Liberty Village and continues East for three miles. Because low interest rates spurred so many Canadians to jump into the condo market, developers have had no reason to stop building. Condo prices rose with the demand and are now 25% higher than they were in 2009.

Unfortunately, after going up and up for almost five years straight, high-rise condo sales were down 6.4% in May. Today, the growing inventory of unsold condos worries the Bank of Canada who says this could create, “the risk of an abrupt correction in prices and residential construction activity.” Canadian banks have strict lending requirements for developers, usually requiring them to sell 70-80% of the units before they can begin construction. However, the biggest concern remaining is that a high-level of purchases from investors may have boosted construction above demographic requirements.

Canada’s housing boom has pushed one in 10 families deep in debt – Financial Post

According to a recent poll from Ipsos Canada, 10% of Canadian families are considered to be highly indebted. The Bank of Canada defines households as highly indebted if their household debt is greater than 250% of their gross income. The poll found that the percentage of households with debts greater than or equal to 250% of their gross income reached a record 13.5% last year.

The increase in household debt was driven by the housing boom and is identified by the Bank of Canada as one of the biggest risks to the Canadian economy. Fortunately, the percentage of indebted Canadians fell to 11.4% in the first quarter of 2013. Statistics Canada also reported that the ratio of household debt to income fell to 161.8% in the first quarter of 2013, from 162.8% in the third quarter of 2012. This measure is another sign that debt levels peaked last year and have now begun to decline.

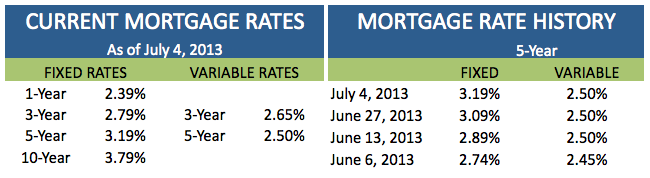

INTEREST RATES IN CANADA

A look at current mortgage interest rates and 5-year mortgage rate history.

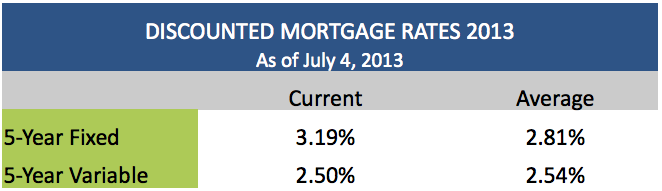

The average discounted mortgage rates in Canada in 2013:

A history of weekly 5-year fixed mortgage rates and 5-year variable mortgage rates.