Monthly Mortgage Update: December 2013

Writing the monthly mortgage update requires a lot of reading, sifting, data aggregation and overall work. “Good” content often does. There is a lot of content out there, but less good content than one would hope for. I am referring to company and personal blogs, such as this one. In the mortgage industry, you can count the good content providers on two hands, one of which is often referenced heavily in these monthly updates.

In 2014, we’re trying to put Ratehub.ca on the hand count. Our editor and content writers have really moved things along the last couple months, too.

I read literally hundreds of mortgage and real estate articles each month, to stay informed on the industry and share important news with our community via our social media and this monthly update. This month, what I’ve read has been overwhelmingly negative, and more so than the new norm for the Canadian real estate industry, which has become a bit of a punching bag.

And with that out of the way, here are the (disheartening) top stories of the month. Read on at your own peril!

Canadian Housing Affordability is Down

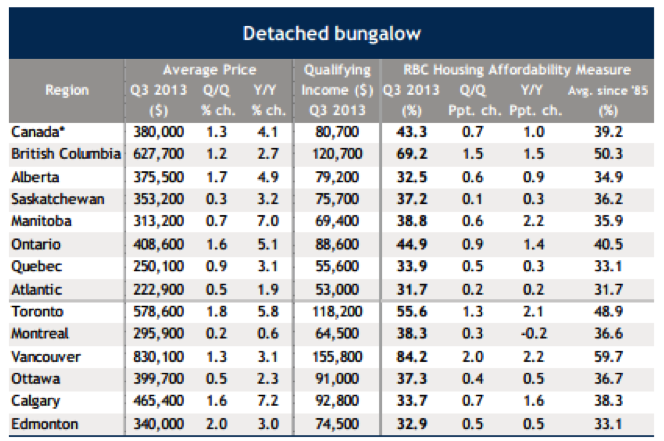

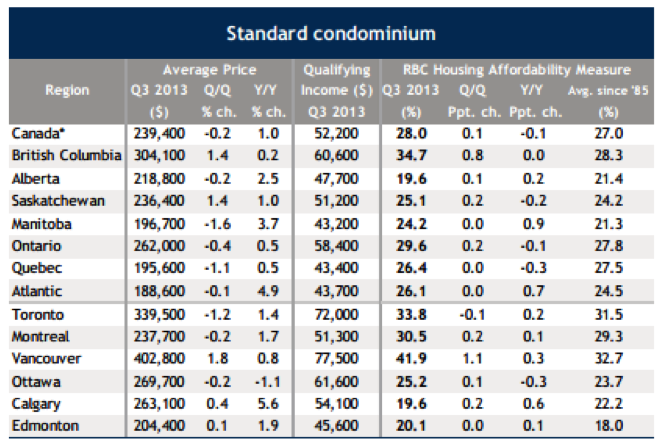

According to RBC’s most recent Housing Trends and Affordability report, housing affordability in Canada has deteriorated since its last quarterly report, which also showed a drop. The average household needed 43.3% of its pre-tax income to service the cost of owning a bungalow at current market values, including mortgage payments, utilities and municipal taxes.

While the average number is only moderately higher than historic norms, there is a wide disparity amongst local markets. In Vancouver, for example, the affordability measure for a bungalow reached 84.2% of an average household’s pre-tax income (a 2% rise from Q2), while in Toronto it rose 1.3% to 55.6%.

Tara Perkins at the Globe and Mail pointed out the impact was largely confined to the markets for detached bungalows and single-family homes, which are indeed becoming more of an unaffordable luxury in many parts of Toronto, Montreal and Vancouver.

The most recent Canadian Real Estate Association (CREA) numbers reported the average resale price of a home rose 8.5% year-over-year to $391,820 in October. And Rob Carrick astutely posed this question to Canadians: “Anyone get an 8% raise lately?”

Source: RBC HOUSING TRENDS AND AFFORDABILITY November 2013

IMF Calls for Scaled Back Role of CMHC

The International Monetary Fund (IMF) released a statement this month asserting Canada is exposing itself to risk by insuring mortgages through the Canadian Mortgage and Housing Corporation (CMHC), and recommended scaling back the federal housing agency.

The Globe and Mail broke down the IMF’s concern as twofold: the current system exposes the government – and taxpayers – to losses in the housing sector, and it distorts the allocation of resources by giving banks more incentive to lend in low-risk mortgage markets rather than to businesses.

Peter Routledge, Director of Equity Research at National Bank Financial, told the paper he estimates about 60% of Canadian residential mortgages have some form of third-party insurance; that’s the majority of the housing market, so any move by the government to follow through on the IMF’s recommendation would have big consequences – not to mention Finance Minister Jim Flaherty uses the CMHC as an instrument to cool the housing market when the government does intervene.

When you consider that the CMHC was created post-WWII to promote affordable housing, how does it continue to serve this purpose today?

Well, for starters, the insurance premiums it offers on high-ratio mortgages (those with less than a 20% down payment) help Canadians, especially first-time homebuyers, access lower mortgage funding costs. Where the CMHC’s role makes less sense, as it’s been suggested, is with portfolio insurance on mortgages with higher down payments (conventional mortgages). Portfolio insurance allows lenders to bulk insure pools of conventional mortgages with down payments exceeding 20%.

In fact, the Globe and Mail reported 30-year mortgage amortizations, which are still available on conventional mortgages, are being monitored closely by Canada’s banking regulator – the Office of the Superintendent of Financial Institutions (OSFI) – as more lenders offer them, despite the government’s obvious intention when it cut the maximum amortization on high-ratio mortgages to 25 years last year.

Rob McLister at Canadian Mortgage Trends reported the government is already considering measures to curb portfolio insurance. Apparently, the Department of Finance confidentially circulated a discussion paper to lenders last month suggesting term limits on this insurance, meaning a lender would need to repurchase the insurance at renewal. Now, lenders commonly buy bulk insurance for the life of a mortgage. This could significantly increase mortgage renewal costs and, as McLister suggests, compel small lenders to raise rates.

Here’s another policy to consider that would serve the CMHC’s original charge: vary the fee structure for first-time versus veteran homebuyers.

Government to Impose a New “Risk Fee” on CMHC

Perhaps in response to the general pessimism surrounding the CMHC of late, the federal government announced a new “risk fee” on CMHC starting next year. The fees of 3.25% would apply to new premiums written, as well as charge 10 basis points on new portfolio insurance, and is expected to cost the housing agency about $50 million a year, according to the Canadian Press.

Since the beginning of 2013, private sector mortgage insurances have been paying Ottawa a 2.25% fee, but the CMHC charge will be greater because the government backs 100% of mortgages CMHC insures. For private insurers, such as Genworth, the government only guarantees 90%.

CMHC told Ratehub.ca, “these new fees are not anticipated to have an impact on the availability or cost of mortgage funding, nor the cost of buying a house. CMHC is reviewing the impact on our low-ratio portfolio insurance product provided to lenders.”

So, if there are no plans to pass on the costs to Canadians obtaining mortgage insurance, where will the money come from and where will it go? In a statement to Canadian Mortgage Trends, a CMHC spokesperson said, “the receipt of all fees from mortgage insurers are treated as part of the Government of Canada’s general revenues”.

The government can, and already is, imposing limits on the CMHC via rules and regulations. However, this 3.25% surplus will be collected by the government so that it has additional capital in the event that delinquencies become so large they force the CMHC out of business, and the government has to step in, in theory. This theory could maybe be improved upon if the surplus were to be held in trust by the government or CMHC instead of being pooled into other government revenue and spending.

Again, this is all very preliminary, so let’s see how the story continues to unfold.

Ratehub.ca News

Infographic

Our love of infographicing (which undoubtedly should have triumphed over “selfie” as the Oxford Dictionaries’ Word of the Year) lives on with our examination of the spending and savings habits of Canadians, as reported in CAAMP’s latest Annual State of the Residential Mortgage Market report.

Guess the Home Price ($) Facebook Series

Over the next couple months, we’re going to be highlighting the bidding wars and general market pricing happening in Toronto’s real estate market with a fun Facebook series which poses the question: was the home overpriced or underpriced?

Alternative Mortgages

You may have noticed we’ve put alternative mortgages into the spotlight on our blog as of late. This is not without merit: alternative lending is a growing market now, with recent tighter mortgage conditions. Read up on our blog!

Mortgage Monthly Newsletter

Don’t forget to sign up for our new monthly newsletter. Get all our best content and a mortgage rate update in one monthly bulletin. Subscribe now or miss out on a condensed version of everything important.

‘Til next month!

–KL

Kerri-Lynn (KL) is the Chief Marketing Officer at Ratehub.ca. Her mortgage recaps can be found monthly on our blog.