Is travel insurance worth it? It depends

In our new reality, buying travel insurance seems like a must-have. Sure, WestJet is refunding some flights (with many limitations and exclusions). As the Cruise industry aims to set sail again, they’re immediately exposed to COVID.

Ultimately, the answer to our question, is travel insurance worth it? It depends.

A good rule of thumb is if you can afford to walk away from your travel purchase without financial repercussion, it’s not worth the effort or price to insure it.

Often, your payout is only as high as the items you own (e.g. baggage insurance) or your flight’s value. The claim process is full of hassle. And many times, you won’t qualify for reimbursement due to limitations and exclusions.

However, insurance covering medical expenses, especially those with pre-existing conditions, or seniors, is tremendously valuable. Cancel for any reason insurance with coverage for big-ticket non-refundable bookings or non-refundable deposits, such as a tour or a cruise, is certainly worth it.

The rise of travel insurance demand due to COVID

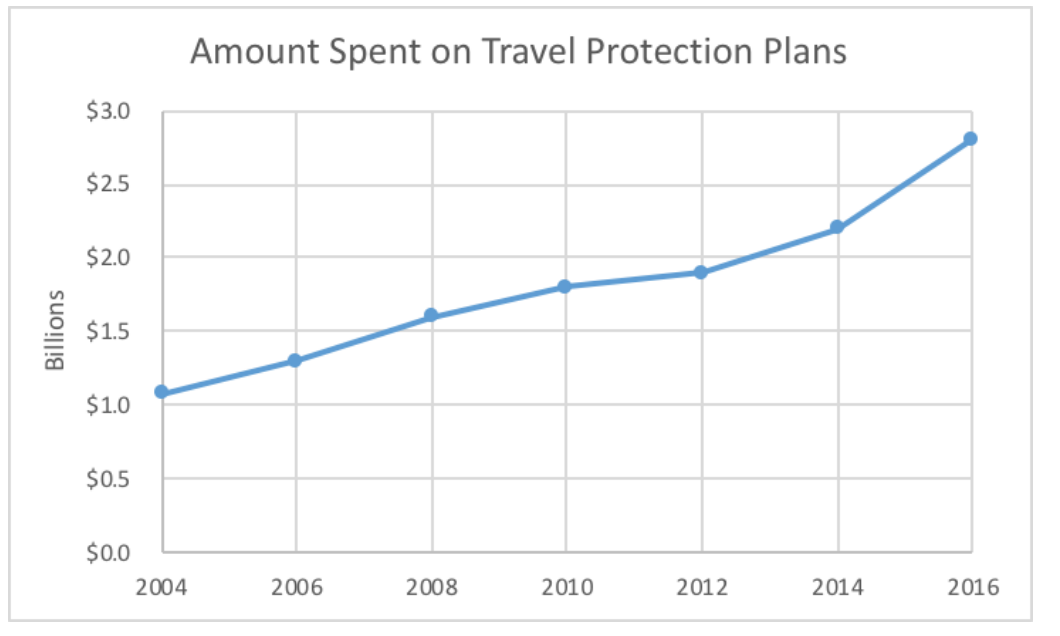

Since the start of the Coronavirus pandemic, the travel insurance demand is up. Still, we don’t have to look far back in history to see how travellers respond. Before 9/11, according to one study, about 7% of people bought travel insurance; afterwards, the figure reached 15%. Research suggests and expects that number to rise to 25% to 30% post-pandemic. This trend is also evident in the total sales of travel protection plans.

source: Flyer Beware

Correlation or causation: Is the industry responding, or are we buying under pressure?

There is possibly a correlation between the increased uncertainty around travel and an increase in the percentage of people buying insurance.

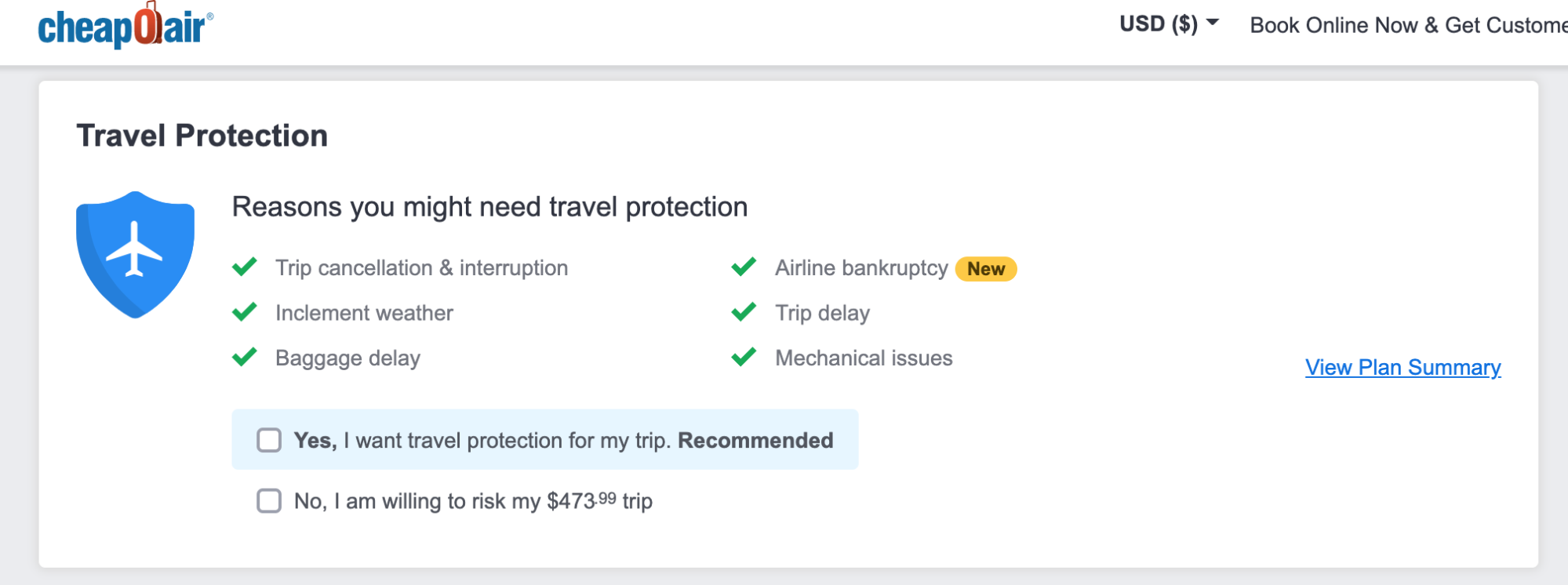

However, there could be other factors. Let’s look at some of the new online tools allowing companies to aggressively sell insurance.

In this example, the “no” button sells fear – “No, I am willing to risk my $473.99 trip.” Not only is it frightening, but it’s also a bit misleading. If you read the fine print, there are remarkably few situations where you’d qualify for a refund.

Many of us spend little time reading the fine print of the policies we’re buying. All we know is we’ve bought coverage, so we skim the details, but rarely do we look at exclusions.

For instance, many policies don’t cover acts of war, terrorism and, yeah, you guessed it – pandemics – the same events which correlate or cause the demand increase for trip protection.

What does travel insurance cover?

It’s difficult to generalize what coverage exists, how claims payout, and what exclusions there may be for each travel insurance policy. However, it is possible to break down the most common categories of insurance and dig through each one to get a better understanding.

Should I buy travel medical Insurance?

Emergency medical travel insurance covers significant medical incidents that may occur while travelling.

Depending on the country, your risk may be low of contracting an illness, but insurance is all about risk. So, understand that the cost of medical services could bankrupt any traveller, no matter the country.

Typically, with medical travel insurance, you have coverage for medical emergencies, including hospital stays and emergency life-saving surgeries. NOTE: If you’re going to a country with less-than-superb medical services, one important feature to include is emergency medical transport services. An ambulance ride isn’t usually covered.

We can’t emphasize it enough, but It’s crucial to read the fine print. For instance, if your medical history is outside the normal, be sure the coverage is extensive and explicitly states it will support you. It may be hard to find insurance to cover seniors or anyone with pre-existing conditions. Often, there may be a small surcharge. Still, generally, medical travel insurance is about $1–$2 per day depending on the duration of travel, medical history, and age.

Also, sometimes you have to do some of your own research. For example, If you need medicine to survive, is that medication available at your destination?

NOTE: Keep in mind that medical insurance does not cover all travel activities. If you plan to skydive, bungee jump, or even a traditional activity like a marathon, your travel medical plan may not cover you. You may need to add on insurance specific to your planned activity.

At Hopupon.com, we recommend getting medical travel insurance on every trip – from a quick business trip to an extensive getaway with multi city flights.That’s because costs can quickly become unaffordable.

Remember, much like how you don’t want to pay for your medical bills at home, travelling adds more complication. For example, this guy was quoted $265,000 by his insurer to get him home, and he had travel insurance!

Is Trip cancellation insurance worth it?

Trip protection insurance insures you for unexpected events occurring before and during your trip. Trip protection is both cancellation and interruption.

It specifically includes all non-refundable bookings – flights, hotels, tours, etc., regardless if it is a single city or one with a multi city trip. Awesome, right? Pay attention to the wording, though – are all your travel expenditures non-refundable?

Check all your bookings to see what is and isn’t refundable. If what you’re booking is refundable, like many hotel rooms, then you’re buying insurance that covers nothing. On the other hand, if everything on your excursion is non-refundable, often big tour groups, then this insurance may cover a lot. The price of coverage, however, remains the same.

To further explain and understand the differences, know that sometimes trip protection is sold in two parts, trip cancellation (before the trip starts) and trip interruption (after the journey begins), but they’re often sold together as a package.

The difference between trip cancellation insurance and trip interruption insurance

Trip Cancellation insures non-refundable deposits on prepaid travel plans. It might also cover cancellation penalties that a transportation carrier or tour guide may charge.

Trip interruption insurance covers the cost if you need to return home sooner (or sometimes later) than expected. This insurance will reimburse you for non-refundable portions of unused prepaid travel arrangements. Sometimes it even covers payment for transportation home.

Now that we understand those differences, there’s a further breakdown. Just as interruption and cancellation are available together as trip protection, trip protection breaks down into general and cancel-for-any-reason.

General coverage vs. cancel-for-any-reason

Trip protection insurance typically comes in two categories.

General coverage

The cost is between 4% and 16% (average is around 6%–7%) of your flight cost for general coverage. However, it’s embedded with a laundry list of exemptions, exceptions, and limits.

Sadly, your actual cancellation or interruption reason is rarely going to fall into these categories. Even if it does make it past the gates of acceptance, making a claim typically requires a significant amount of documentation. Unfortunately, there is no hard data available on how many claims are rejected as proof. But, here is a consumer affairs forum with negative reviews outlining why, even though these consumers had travel insurance, their claim was denied.

For example, many insurers require written evidence. Suppose you were going to claim a travel delay benefit (e.g. traffic accident en route). In that case, you have to prove you left early enough to get there at the time the transportation carrier supports. So, for most airlines, if you’re travelling internationally, that means you’d be at the airport 3 hours ahead of time.

If you need to make a claim, your travel insurer requires evidence via a police report of the traffic delay. If an accident caused the delay, and you weren’t in the accident, you might need to note where it happened, then call, and go through the rigamarole to get the report.

You also need the foresight to note this while rushing to get to the airport on time. Depending on your salary, the trip’s cost, and the potential reimbursement, the effort required to submit the claim may not be worth the effort. Unless you have cancel-for-any-reason coverage, which, as the name implies, doesn’t need much documentation, but it’s expensive.

How much does cancel for any reason travel insurance cost?

Cancel for any reason will allow you to cancel for any reason. But, of course, with premium coverage comes premium costs. For instance:

- Costs up to 40% of your total trip cost.

- Typically covers 50% to 75% of the cost of a cancelled trip.

- May have restrictions on how far in advance you have to cancel.

It might be a better idea to book a refundable plane ticket(s), tours and hotel stay whenever possible.

Should I buy trip protection insurance?

If you booked a tour and the entire trip was not refundable – then yes, it would make sense to buy trip protection insurance. Typically refund rules are more straightforward than insurance rules. If you can, book everything as refundable and forgo the insurance altogether.

On the other hand, If you are booking your flights and accommodations independent of each other, know that many hotels and individual tours have refund policies. If so, only your flight needs to be insured and depending on how you bought it, it may not be worth the cost. In fact, a sound travel credit card may simply refund the points to you.

So, is trip protection insurance worth it?

Trip cancellation and Interruption insurance often fail to protect what consumers think they are getting. Insurance providers oversell their coverage and benefits until you read the fine print.

However, getting to the fine print usually takes a few clicks and requires a fair amount of time to read through. That time is often limited with a price guarantee, which doesn’t give you, the consumer, enough time to consume all the necessary information before their booking expires. And don’t forget the fear they’re selling you – that’s some pressure!

Because of these pressure tactics and misleading marketing, we can assume it’s being oversold to consumers. In fact, check out this 2018 market study showing that 90% of travel insurance products in the US were travel protection, while only 6% were of medical insurance.

However, the decision is personal and dependent on the situation. I would say it’s about peace of mind, but if you have to walk on nails to claim a refund, well, that doesn’t sound peaceful.

Is luggage insurance a rip-off?

While it’s often grouped together with trip protection, sometimes you can buy baggage insurance on its own. You’ll usually get your money back following a claim because the airline is the only party involved, and they have all the details. Sadly, there are a few factors which you should be aware of.

- It must be after a certain amount of hour(s) for any claim.

- After 21 days (or long after your trip), only then do they consider it lost.

- There is a maximum value on each item, group of items, and luggage, regardless of what’s inside.

- Typically, there’s 2 payouts – delay and lost luggage. Meaning, any money spent abroad may not be recoupable if it is returned to you.

- Depending on the insurance, you may need receipts for all items – which can be difficult for your cherished 90’s Nirvana tee.

Instead, carry valuables in your carry-on or leave them at home.

What about existing coverage? Doesn’t my credit card protect me?

Now that you understand all the different coverage types or travel insurance, it’s time to see what else exists. Take the time to understand your current insurance coverage with your health plan, credit cards, school, or workplace benefits.

Most premium rewards credit cards come included with travel medical emergency insurance, travel accidents, flight delay, and lost baggage. So long as you buy your flights and hotels with your card. If your family members are on the same booking, coverage extends to them as well.

Credit card travel insurance coverage usually applies to people 65 or younger, without pre-existing conditions, and for trips up to 15 days.

The National Bank World Elite is Ratehub’s pick for Canada’s best credit card for travel insurance: including $5,000,000 in travel emergency insurance for trips up to 54 days. Also includes coverage for seniors of 15 days for those up to 75 years old.

Whenever you make a claim, time of the essence. There are usually cut off dates from the date of the incident and when you can make a claim.

It’s important to know what you have, understand the gaps in your coverage and then make sure any new policy you are buying fills in those gaps. Don’t buy insurance if you can walk away from what you’re insuring without worrying about your pocketbook.

The bottom line

If you’re still a bit confused, then, as a general rule, know there is more value in travel medical insurance than trip protection.

Again, travel medical insurance can cover costly medical bills that are unlikely to occur, but they can put you in serious financial problems without it. In comparison, trip protection often costs the same but doesn’t cover as much, and claims could be full of hassle.

Trip protection can be a good option when you have a significant number of non-refundable bookings within your trip. It’s probably not worth it if it’s only the flight. Don’t be fooled by pressure tactics to get this insurance if you don’t need it.

Read the fine print. As with most things in insurance, the answer depends on your situation and your risk tolerance.

ALSO READ

- Do you need travel insurance to travel in Canada?

- Rental car insurance: How to avoid paying extra fees

- Details on credit card trip cancellation and interruption insurance