Is Paying Off Your Mortgage Better Than Contributing to an RRSP?

A mortgage loan is likely to be the largest sum of money you will borrow in your lifetime. The average life expectancy in Canada is 80 years of age, so a typical 25-year amortization length corresponds to nearly a third of the average Canadian lifespan – representing a large portion of one’s lifetime to pay interest to a bank! In terms of saving for retirement, is it better to direct your funds towards reducing mortgage debt or towards RRSP contributions?

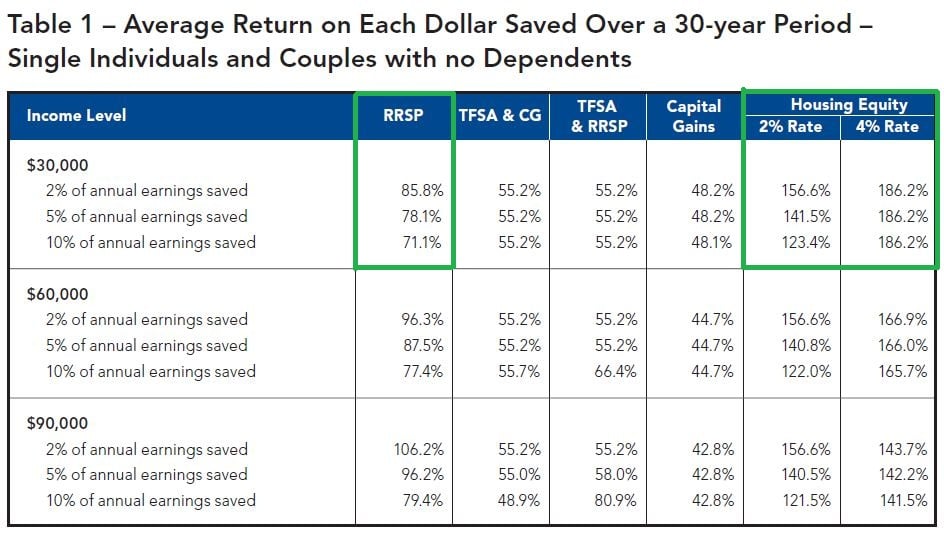

According to a study released by the Certified General Accountants Association of Canada (CGAAC), the return from using additional funds to pay off your mortgage debt faster, may yield a higher return than investing in RRSPs.[i]

We should note the results were acquired under a set of assumptions. For one, individuals are presumed to be making monthly payments to a fixed rate mortgage. At renewal (assumed to be every 5 years), individuals always opted to maintain the current monthly mortgage amount, to shorten the amortization period.

Multiple scenarios were tested at different income and savings levels, as well as different mortgage interest rates. The return on RRSPs was 3% while the mortgage rates tested ranged from 2-4%.

The Results

Looking at the table below, paying off a mortgage faster always outperformed the more traditional forms of retirement savings instruments. This is especially true for lower-income individuals. For those earning $30,000/year and saving 2% of that income, the return on accelerating mortgage payments almost doubled when compared to an RRSP contribution.

*chart courtesy of CGAAC

The real benefit of accelerating mortgage payments as a savings strategy materialises once the mortgage is fully paid off. This is because individuals who saved through RRSPs will have to continue to service their monthly mortgage obligations, whereas individuals who saved through housing equity will be able to allocate an equivalent amount to a savings instrument such as an RRSP.

How do you pay off your mortgage faster?

Prepayment options allow borrowers to pay down their mortgage loan faster by making lump sum payments towards their mortgage principal or by increasing their monthly mortgage payments without penalty.

Most mortgages come with a 5-25% lump sum prepayment allowance and anywhere from 10-100% monthly payment prepayment allowance. This gives borrowers significant opportunity to pay down their mortgage faster.

According to CAAMP’s 2011 Survey, nearly a third of Canadians with mortgages took advantage of their prepayment options this year

If we translate this into absolute figures, 1.86 million Canadians engaged in prepayment options.

Are Canadians really paying off their mortgage faster?

According to the CAAMP survey mentioned above, on average, Canadians are paying off their mortgage seven years faster than their original amortization schedule. This is good news; however, Ratehub.ca found recently that there is still a minority of Canadians who are carrying their mortgage debt into their 70s. Roughly, one in three older Canadians (over the age of 55) still have 16+ years of mortgage debt left to pay off.

Smart retirement planning is essential to maximize your available funds later on in life. Canadians have many options available to them. Traditionally, Canadians have turned to RRSPs, TFSA, and the open market; however, CGAAC revealed that paying your mortgage off faster is a viable option.

The question is, is it a better retirement plan than RRSP contributions? The answer is it depends. Everyone’s situation is different because there are numerous factors that can affect a person’s finances and retirement plans, from annual earnings to number of dependants to mortgage type. In general, it’s always a good idea to pay off your mortgage sooner, rather than later. To understand your mortgage options, speak with a Canadian mortgage broker.