How to compare savings accounts: the fine print

This blog is sponsored by EQ Bank. The views and opinions expressed in this blog, however, are my own.

Let’s face it. Nobody likes to read the fine print. But if you’re looking for the best savings account to park some money away for things like an emergency fund or even just general savings, digging into the account features and oh-so-tiny legal subscript can be worth your time.

Don’t just assume all you need to do is go with the bank account that offers the best advertised interest rate at the moment. You’ve got to scratch below the surface and investigate a bevy of features to make sure you’ve really hit paydirt.

Here’s a roundup of what to look out for when you’re on the search for a savings account that will keep delivering over the long term.

Promo rates vs regular rates

If you’re signing up as a new account holder with a bank be sure to check if the interest rate advertised is a standard rate or a promo rate.

Some savings accounts offer an accelerated promotional rate for a temporary period of time, but after the promo period ends (typically after four to six months), the interest will drop significantly – often by quite a few percentage points.

On the other end of the spectrum, some high-interest savings accounts – like EQ Bank’s Savings Plus Account – offer a high interest rate as standard that won’t expire after a predetermined date.

EQ Bank’s Savings Plus Account

![]()

![]()

-

- 1.25% everyday interest1

- No minimum balance

- Free Interac e-Transfers®

- Cheap international money transfers

Savings accounts with limited-time promotional rates do have their advantages. Particularly, if you’re a personal finance optimizer who’s used to juggling multiple bank accounts and is always on the ready to move money around to chase the next best offer.

But if you just want to keep things simple, set your money aside, and avoid constantly hopping between banks, be careful not to dismiss an account just because it doesn’t offer the most attention-grabbing rate. The standard 1.25%1 interest rate offered by EQ Bank’s Saving Plus Account, for instance, is the kind of solid standard rate of return ideal for someone who wants to keep things simple and avoid micro-managing their everyday finances.

More importantly, if you just want to stick with the same savings account, you’ll want to avoid being lured by a promotional interest rate only to learn a little too late that the numbers don’t add up to much over the long term. And if you do decide to chase a promotional rate, be sure to read up on when the promo ends and mark your calendar to move your money out and switch accounts at the right time. After all, what’s the point of signing up for a big rate if it drops significantly after just a few short months?

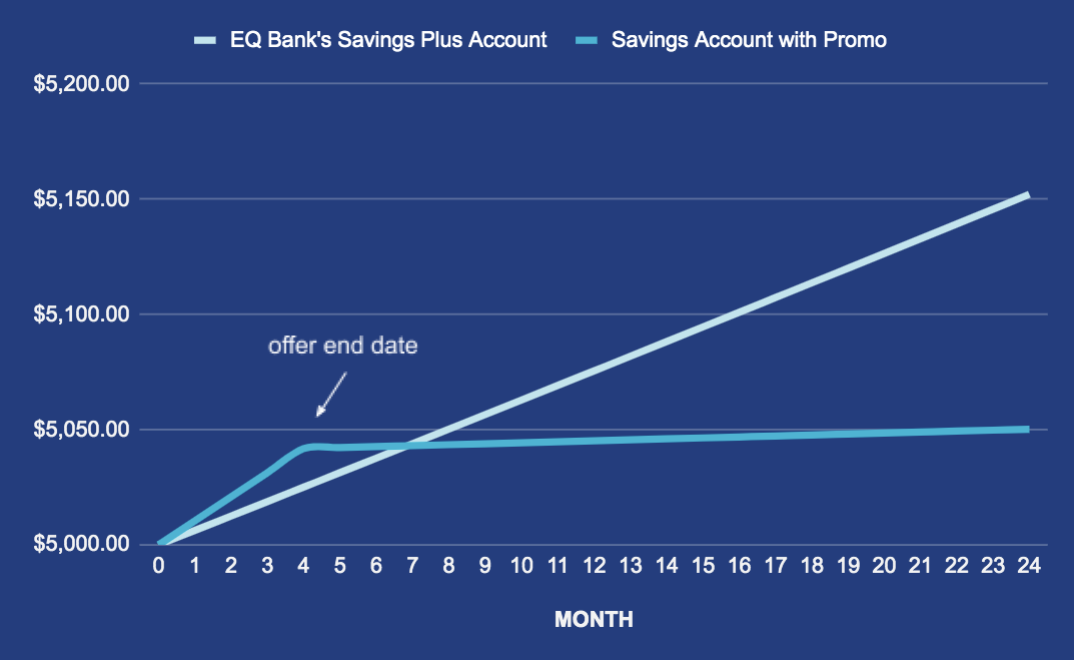

As an example, we’ve run the numbers to compare two years’ worth of gains on a $5,000 deposit held in the EQ Bank’s Savings Plus Account versus an account that has a limited promotional offer of 2.5% for four months and a regular rate of 0.1% afterwards. Here’s how the returns would compare:2

Interest on new deposits

Sometimes, even if you’re already an existing customer, banks might offer you a higher promotional interest rate for a limited time on a savings account you’ve already had opened for a while. But it’s important to be aware that this higher interest rate will normally only apply to new deposits. That means that the money you’ve already had sitting in the account before the promo kicked in will earn interest at the regular rate while only additional amounts of money you deposit will be subject to the higher rate.

Minimum balance

Some banks require you to maintain a minimum balance in your savings account in order to earn a higher interest (minimum balance requirements are actually a pet peeve of mine). Meanwhile, other banks dish out interest rates in tiers and require you to keep the account open for a set number of days or months in order to unlock the highest interest rate advertised.

With accounts that don’t impose any minimum balance requirements or tiered earn rates – like EQ Bank’s Saving Plus Account – you’ll earn a flat 1.25%1 interest regardless of the size of your balance (even if it’s just $1), keeping things simple. The one thing to note regarding EQ Bank in particular: there’s actually a maximum balance as you can hold up to $200,000 across all EQ Bank accounts.

EQ Bank’s Savings Plus Account

![]()

![]()

-

- 1.25% everyday interest1

- No minimum balance

- Free Interac e-Transfers®

- Cheap international money transfers

Transaction fees

Some banks will charge fees on transactions on savings accounts. Transactions usually encompass any type of action involving moving money in or out of your savings account (i.e. Interac e-Transfers®). Some savings accounts won’t charge you any fees so long as you move money between two accounts from the same bank. Moving money between different banks, however, may result in a fee.

It’s crucial to read up on any transactions associated with an account so you aren’t surprised by charges that can eat away at your savings.

Not all banks charge clients for moving money to a different financial institution. With EQ Bank’s Savings Plus Account, for example, Interac e-Transfers® are free, allowing you to move up to a maximum $10,000 per week at no extra cost. Plus, you can move larger sums of money with Electronic Funds Transfers (up to $30,000 per transaction) and deposit cheques ($100,000 per cheque) at no extra cost.

When interest gets paid

Make sure you also pay attention to when your bank pays out interest because it can impact your overall returns. For example, EQ Bank’s Savings Plus Account (as with most savings accounts at Canadian banks) calculates interest daily based on your total balance and pays it out monthly. This daily calculation of interest and monthly payout can be a boon because, thanks to the power of compound interest, your returns could really start to add up as you continually earn interest on top of your previously accumulated interest.

In some cases, however, your interest may be paid out or calculated differently so be sure to get clear information about how it will be paid. Sometimes during a promotional rate period, a bank may only pay out the bonus amount in one mass amount at the end of the promo, meaning that you could miss out on compound interest gains.

EQ Bank’s Savings Plus Account

![]()

![]()

-

- 1.25% everyday interest1

- No minimum balance

- Free Interac e-Transfers®

- Cheap international money transfers

The bottom line

While you might think the only factor you should consider when picking out a savings account is the advertised interest rate (and in many ways, it’s arguably the most important), you’ll still want to dig deeper into the fine print and account features to ensure you’re paired with the right savings account for your financial personality and long-term savings goals.

1 Interest is calculated daily on the total closing balance and paid monthly. Rates are per annum and subject to change without notice.

2 This line chart is for illustrative purposes only and is based on comparing the current interest rate offered by EQ Bank’s Savings Plus Account versus an example savings account.