How much mortgage can I afford?

This piece was originally published on December 30, 2019, and was updated on September 11, 2025.

When you first begin the househunting process, one of the most important - if not the most important question to ask yourself is, "How much mortgage can I afford?" You want to make sure that you have enough to purchase your new home, handle closing costs and still have enough left over to avoid the trap of being "house poor".

You also want to know what type of mortgage will suit your needs best. This is always important, but can be a little tricky to figure out in the current rate environment, where rates are elevated, but rate cuts are expected later in 2024 and into 2025. Check out this helpful video below, then read on for more detail on how to determine how much mortgage you can afford.

WATCH: How much mortgage can you afford in 2025?

What is mortgage affordability?

A few things determine mortgage affordability; the household income of the mortgage applicant or applicants, the monthly expenses of the applicant(s), and the expenses associated with home ownership (property taxes, utility fees, condo fees, etc.).

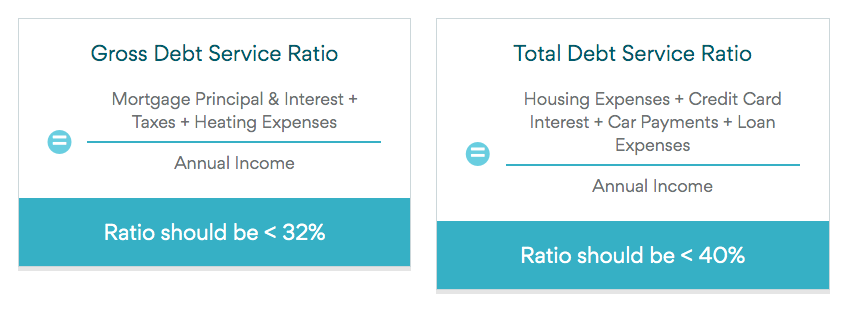

Perhaps the most important factor that impacts mortgage affordability is a homebuyer’s debt service ratios. Lenders use two different debt service ratios when determining affordability: gross debt service ratio (GDS) and total debt service ratio (TDS). See below for a guide to calculating both those debt service ratios. Keep in mind that lenders may allow for maximum GDS ratios of 39% and TDS ratios of 44%, respectively. But, this is the mark for homebuyers with superb credit ratings.

If you’re someone who isn’t fond of math, you’re in luck. Our handy mortgage calculator can do the work for you.

Let’s take a look, using an example, to determine mortgage affordability.

How much mortgage can I afford?

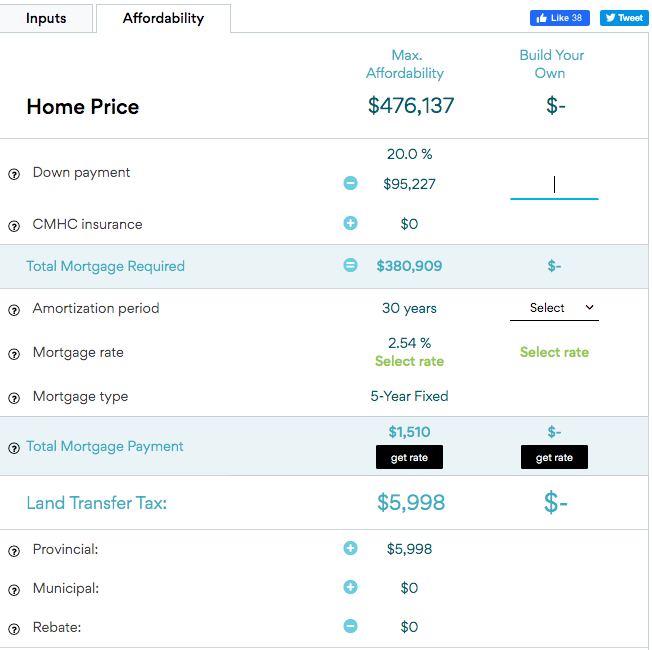

As previously mentioned, you’ll need to know a few things; your annual income, your debt payments, and your living costs. While the first two are easy, the third might be more difficult because it can fluctuate based on the property you purchase. Luckily, the mortgage affordability calculator can estimate living costs for you.

So, let’s assume you make $80,000 per year and have $300 per month in debt payments ($100 in credit card payments and $200 in car payments). We’ll let the affordability calculator determine your living costs. In this example, they are estimated at $425 per month in property taxes and $99 in heating costs.

With those figures put into the calculator, you simply click “how much can I afford” and you’re on your way.

The maximum affordability for the buyer estimates we used is a home that costs $476,137.

You can also play around with the affordability calculator to figure out what your monthly payments might be.

The calculator uses a default example of a five-year fixed rate of 2.54%, which, at press time, is one of the best mortgage rates in Canada.

It also assumes a down payment of 20% (which, in this case, is $95,227) and an amortization of 30 years.

With these assumptions, the example buyer we used would pay a total of $1,510 in mortgage payments per month.

What else can the mortgage calculator do?

You can play around with the calculator to determine your own affordability. You can also use it to determine how much cash you’ll need up-front to purchase a home (land transfer taxes, insurance, etc.), as well as your total monthly expenses.

Compare today's top mortgage rates

Looking for a great mortgage rate? Check out the lowest mortgage rates available

The bottom line

Before getting your hopes set on a particular home or budget, use the mortgage affordability calculator to figure out how much house you can afford.

Also read: