Why Are GIC Rates So Low? And Where Are They Headed?

Let’s not kid ourselves: GIC rates aren’t exactly shooting the lights out these days. That’s not to say you can’t do ok, especially if you shop around. But historically speaking, GICs nowadays don’t yield as much as they used to.

Why are GIC rates so low? The first thing to understand is that interest rates, in general, are very low at the moment. This applies to everything from high-interest savings accounts to Canada Savings Bonds to highly-rated corporate debt. In other words, to understand why GIC rates are so low, we need to ask why interest rates are low.

In part, there has been a trend towards lower interest rates due to persistently low levels of inflation in developed countries such as Canada. Savers are willing to accept lower “nominal” rates when inflation slows; this is because they do not require as high an interest rate to maintain their money’s purchasing power. For example, if inflation is running at 5%, then as a saver you would typically want to earn, say, 6% (or just another above 5%) so your money keeps pace with inflation.

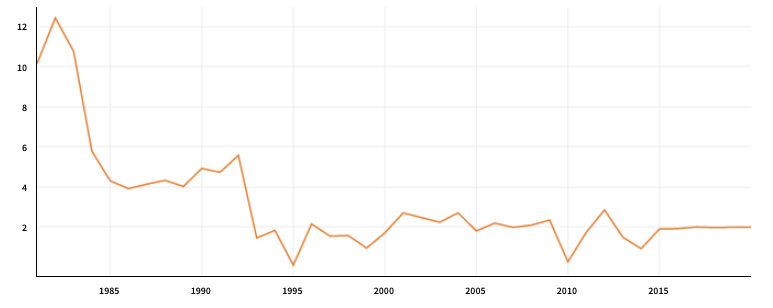

As the following chart of the Consumer Price Index illustrates, from double digits in the 1980s, inflation is Canada has hovered in the low single digits for many years now.

Source: Quandl

Slowing inflation is only part of the low interest rate story, however. At present, some GICs do not earn a rate of interest equal to the inflation rate. Why is this?

The answer can be found in central banks’ responses to the global financial crisis. To fight the global recession, key central banks lowered their interest rates dramatically. The Bank of Canada interest rate currently sits at 0.75%, which it was lowered to back in January. The rates that central banks control are typically short-term, but they affect everything from mortgage rates to personal loan rates. So when the Bank of Canada lowers rates, it tends to result in cheaper mortgages, loans, etc.

Why does this influence GIC rates? Banks are, not surprisingly, in the business of making money. And they essentially make money by borrowing at one rate from savers, and lending it out at higher rates to borrowers. If a bank is lowering its mortgage rate to stay competitive with other financial institutions, it’s likely to hold steady or even reduce the interest rate it pays on deposit products, such as GICs.

To sum up the story so far: low inflation and the financial crisis response by central banks have led to the very low interest which we see today. But you’re probably wondering, where are GIC rates headed?

With the caveat that no one has a crystal ball, it would be surprising if GIC rates were substantially higher than they are today in the next few years. As house prices have continued to climb alongside consumer debt levels, the Bank of Canada understandably will be wary of raising interest rates much, if at all in the foreseeable future. A Bank of Canada interest rate hike would hurt consumers and potentially cause undue stress in the housing market.

In addition, the oil price crash motivated the Bank of Canada to cut rates to support economic growth. Unless oil somehow shoots back up to $100/barrel, it would be very surprising if the central bank raised rates given the fallout in oil-dependent provinces.

All this said, it’s worth keeping in mind that GICs do offer a return, even if it’s not huge. And perhaps most importantly, your principal is guaranteed while you earn that return. GICs do not come with the same possible rewards as other assets, such as equities, but they also don’t come with the same risks to your investment.

Flickr: Bruce McKay

Also read: