What's the penalty if I break my mortgage with CIBC?

This piece was first published on April 12, 2020, and was updated on January 5, 2023.

Whether you’re refinancing your mortgage, transferring it to another lender, or selling your home before your term is up, you’ll likely have to pay a pre-payment penalty (also called a pre-payment charge).

What is a pre-payment penalty?

The pre-payment penalty is your lender’s way of penalizing you for breaking your mortgage contract early. What your pre-payment penalty will be ranges based on a lot of factors, which we’ve explained below. To help you get an estimate of what your penalty fee might look like, we developed a mortgage penalty calculator.

Looking to refinance your mortgage?

Check out the lowest interest rates available right now!

Calculating the pre-payment penalty

Even though the banks have to host their own pre-payment calculators, the legal jargon used on many can still leave even the most well-informed homeowners confused. Because of this, we decided to take on the responsibility of researching and explaining each bank’s calculations in the simplest terms possible, so no one is left in the dark about how these penalties work. The first bank we are going to look at is CIBC.

Depending on if you have a fixed- or variable-rate mortgage, CIBC will charge you one of two fees:

- Three months’ interest, or the

- Interest rate differential (IRD).

If you have a fixed-rate mortgage, you will pay the greater of three months’ interest or the interest rate differential. If you have a variable-rate mortgage, however, you will always pay just three months’ interest. Let’s review how both calculations work.

Method 1: Three months’ interest

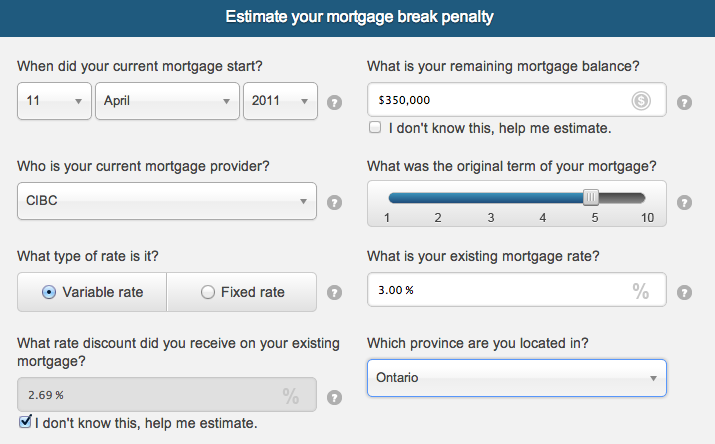

Three months’ interest is exactly that: the amount of interest you would have paid in a three-month period on your current mortgage. Instead of using your current mortgage rate, however, CIBC uses its Prime rate. Let’s look at an example we put through our penalty calculator.

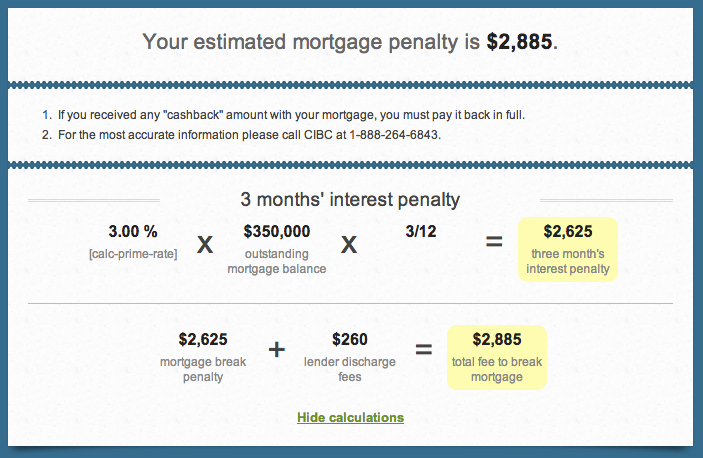

Assuming you still owe $350,000 on your mortgage, three months’ interest is calculated by multiplying the interest rate (because CIBC uses its Prime rate, you will need to enter that manually and right now it is 3.00%) by the mortgage balance and again by 0.25 (represented as 3/12 for the three-month period out of the year). As you can see below, this equals $2,625.

However, on top of the three months’ interest, you’ll also need to pay a fee to discharge your mortgage. In Ontario, CIBC’s discharge fee is $260, so we added that into our calculation.

Using CIBC’s Prime rate may be advantageous for any homeowner whose current mortgage rate is higher than that. However, for someone with a discounted rate that is currently less than Prime, they will actually end up paying more than the interest they would have paid in a normal three-month period.

In this example, because you had a variable-rate mortgage, CIBC would charge you the three months’ interest penalty fee of $2,625 + $260 to discharge your mortgage for a total of $2,885. If you have a fixed-rate mortgage, however, you still need to find out if three months’ interest is more or less than the interest rate differential.

Method 1: Interest rate differential (IRD)

To calculate the interest rate differential, your lender looks at the difference between two interest rates and how many months you have left to pay off your current mortgage term, then finds the amount of interest they’d be losing by letting you break your term early.

Instead of looking at your current interest rate and finding the difference between that and a new rate, CIBC finds the posted rate from the day you signed your original term and subtracts today’s posted rate for a product that would cover the remainder of your term from that. Sounds complicated, right? It can be, which is just another reason we knew we had to create this calculator!

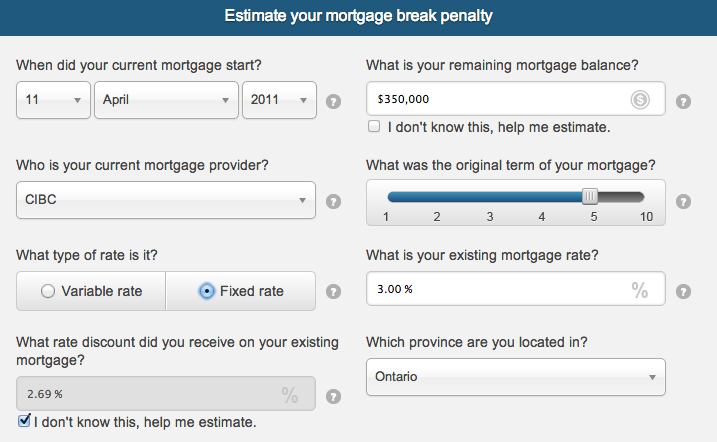

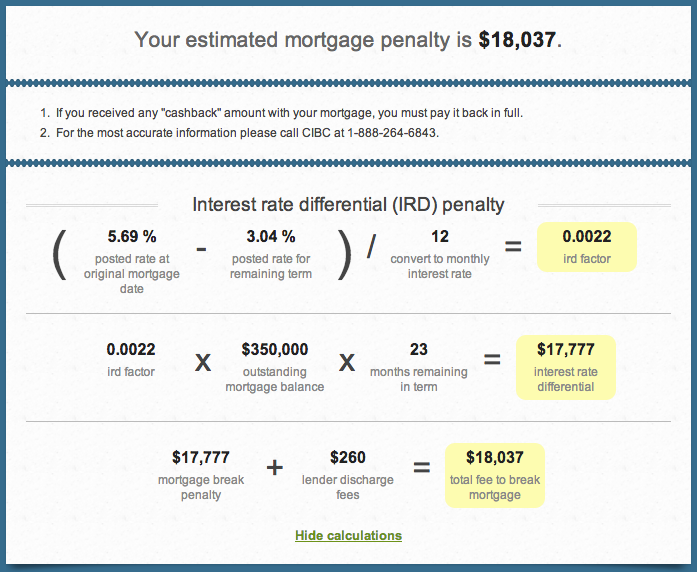

Using the same numbers as in our previous example, let’s say your mortgage balance is $350,000 and you have 23 months left in your term. CIBC would first find a product that would cover the remainder of your term – in this case, you would need a 2-year fixed-rate mortgage, because CIBC would round up 23 months to two years.

Then, CIBC would find the difference between the old posted rate (which was 5.69%) and today’s posted rate for a 2-year fixed-rate mortgage (let’s use 3.04% for this calculation) and your interest rate differential calculation would look like this:

And don’t forget to tack on that $260 discharge fee.

In this example, because you had a fixed-rate mortgage, CIBC would charge you the greater of three months’ interest or the interest rate differential (IRD). Since we know three months’ interest was only $2,625, you would have to pay the IRD, which is $17,777 + $260 to discharge your mortgage for a total of $18,037.

Other penalty fees

While our calculator gives you a good estimate of what you’ll have to pay to break your mortgage term early, there can be a number of other fees involved. One of them is a discharge fee, which we’ve included in our calculations; this fee varies from province to province.

If you live in Ontario, New Brunswick or Newfoundland, you will also have to pay a registration fee of $71.30 for CIBC to register your new title. In all other provinces, you have to pay this at your municipal land title office instead of through your bank.

In Quebec, you will pay all other fees through a notary. It’s important to note here that you may also have to pay a notary or real estate lawyer to complete this entire transaction.

Finally, if you took out any cash back when you entered or renewed your mortgage, CIBC may you ask you pay that back in full. The bank’s pre-payment charge calculator states that it “assumes that you are required to repay [CIBC] 100% of the cash back amount.”

Looking to refinance your mortgage?

Check out the lowest interest rates available right now!

CIBC pre-payment privileges

If you want to try to lessen your pre-payment charge, CIBC will let you make either a 10% or 20% lump sum payment each year, depending on what is written in your current mortgage term agreement. For example, if your current agreement says you can make a 20% lump sum payment each year, you can do that before breaking your mortgage in an attempt to lower your pre-payment charge.

The bottom line

There are plenty of good reasons to break your mortgage with CIBC, depending on your circumstances. The most important thing is to be fully informed when you make the decision. If any of this is confusing, don’t be afraid to get in contact with a mortgage professional, such as a mortgage broker. A broker can take you through the process and make expert recommendations, at no cost to you.

Also read: