What Potential Buyers Need to Know About Investment Property Mortgages

Flickr: reallyboring

If you’re looking at different ways to invest your money, a popular option chosen by many Canadians is to purchase an investment property. On top of the potential income it could generate for you, adding an investment property to your portfolio brings more tax shelter benefits to you, and the potential capital appreciation could make it a great piece in your long-term investment strategy.

However, qualifying for an investment property mortgage is not the same as qualifying for the mortgage you would borrow for your principal residence. In fact, the minimum down payment amount, the CMHC insurance rates, and the debt ratios used to determine how much you can borrow, are all different from what you know to be true for principal residence mortgages. So, if you’ve been toying with the idea of purchasing an investment property this year, read on to find out how you can prepare yourself for the transaction.

Looking to determine your mortgage payment?

Use the mortgage payment calculator to determine your estimated mortgage payments.

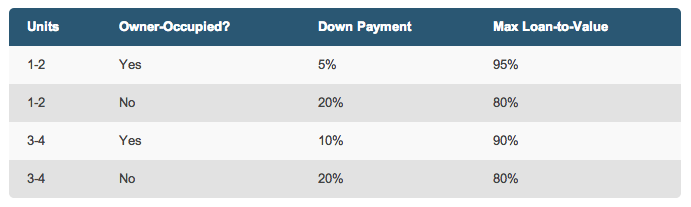

Down Payment

Unlike the minimum down payment you must make on a home that serves as your principle residence – which is 5% of the purchase price – the minimum down payment you must make on an investment property depends on two things: how many units are in the property and whether or not you plan on living in one of the units.

Owner-Occupied:If you plan on living in one of the units of the investment property, you can see in the chart above that the minimum down payment you must make in order to purchase it depends on how many units there are in total. If the property has 1-2 units, your minimum down payment is just 5%. If you’re buying a triplex or fourplex, with 3-4 units in total, you need to put down at least 10%.

Non-Owner Occupied: If you don’t plan on living in one of the units, making it strictly an investment property, then your minimum down payment is always 20% – no matter how many units there are.

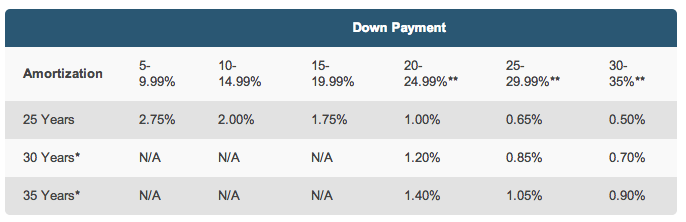

CMHC Insurance

You know the rule for mortgage default insurance on your principal residence: if you put down 20% or more, you don’t have to pay it. Unfortunately, the same rules don’t apply for investment property mortgages. And, again, the numbers change, depending on whether or not you plan on living in one of the units in your property.

Owner-Occupied: If you plan on living in one of the units, the CMHC insurance rates listed above will apply to your investment property mortgage. Notice that if you put down 20% or more, you may qualify for a 30 or 35-year amortization period. Unfortunately, even with 20% down, you still need to purchase CMHC insurance. And for every 5 years you add to your amortization, you need to pay an additional 0.20% premium.

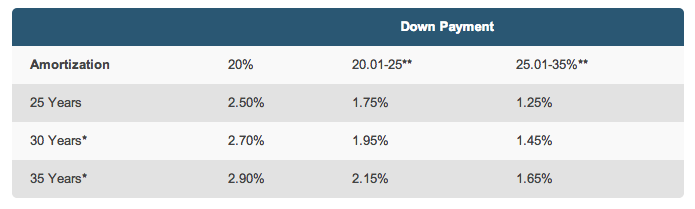

Non-Owner Occupied:If you don’t plan on living in one of the units, not only do you need to put at least 20% down, but you will also be subject to higher CMHC insurance rates. And again, you may qualify for a 30 or 35-year amortization period, but you’ll need to pay a 0.20% premium for every 5 years you add on. Remember that, in both scenarios, CMHC insurance premiums are added to your investment property mortgage and paid off over the life of your loan.

Debt Ratios

When it comes to seeing how much you qualify to borrow, lenders stop looking at whether or not you’ll be occupying one of the units. Instead, they want to know how much rental income you’ll be generating from this investment property – and they’ll plug that information into 1 of 3 debt ratio calculations:

- Rental Offset– With rental offset, your lender will take a percentage of your total expected rental income for the year and use that amount to offset expenses, such as your mortgage payments, property taxes, utilities, etc. Most lenders offer rental offsets between 50-70%.

- Rental Inclusion – With rental inclusion, your lender will take 50% of your total rental income for the year and add it to your personal gross annual income. From there, the standard total debt service ratio (TDS) calculation is performed.

- Debt Service Coverage Ratio (DSCR) – With the DSCR, your lender isn’t looking at your personal debts. Instead, they want to determine if the total rental income from your property each year is going to be enough to cover the mortgage payments (principal + interest).

To see how these calculations work, scroll down to the “Debt Ratios” tab on our investment property mortgages page.

Mortgage Rates

Fortunately, if you can put down at least 20% and meet the qualifying criteria set by your lender, you should be able to access today’s best mortgage rates for your investment property mortgage. I say “some” because there are small lenders who will charge you a premium (like + 0.30%) for an investment property mortgage, while some others don’t offer them at all. To learn more about your options for a mortgage on a potential investment property, sit down and talk to a mortgage broker.