What is a GIC?

It’s true there are no guarantees in life – well, except when it comes to one investment product. In Canada, guaranteed investment certificates (GICs) are a financial tool that lets us invest our money and be guaranteed we’ll see the return of our principal plus a set amount of interest. There are a number of different types of GICs available, all with varying GIC rates, but, in general, the longer you’re willing to invest your money in a GIC, the higher your interest rate will be.

Here’s a quick summary of how GICs work, why banks offer them and how you might be penalized if you try to cash out early.

What types of GICs exist?

There are so many different types of GICs available, but you could split them up into two general categories: fixed rate GICs and variable rate GICs.

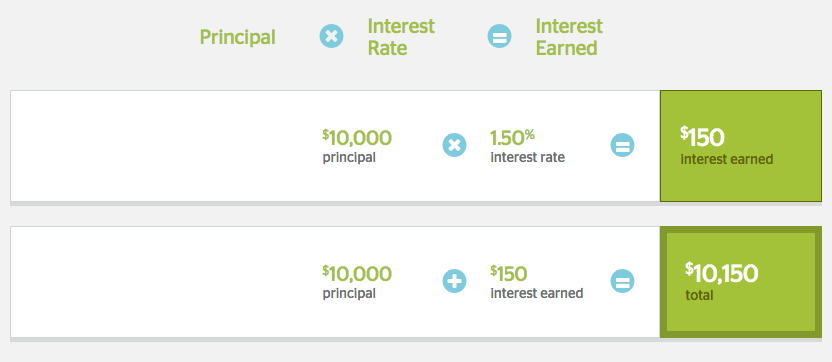

Fixed rate GICs promise a defined amount of interest at the end of the term. For example, you could invest $10,000 in a 1-year GIC at 1.50%. When the GIC matures, you’ll see a return of your principal ($10,000) + $150 of interest for a total of $10,150.

Fixed rate GICs are what you typically see advertised by financial institutions, and are available as cashable GICs, non-redeemable GICs, registered GICs and even foreign currency GICs.

Variable rate GICs, on the other hand, are similar to variable rate mortgages in that they are attached to either Prime rate or the performance of a stock market index. They offer the possibility of greater returns if the market performs well, however, if the market doesn’t perform well, you may see no return at all – other than your principal, which is always guaranteed.

Variable rate GICs are more commonly referred to as equity or market-linked GICs.

Does it cost anything to invest in a GIC?

Unlike some other investment products, there are no fees involved in purchasing GICs. Financial institutions typically require a minimum of $500 be invested, but that’s your investment – there are no fees involved. It’s also worth noting here that, depending on which GIC product you buy, interest can be paid monthly, semi-annually or annually, or be automatically reinvested.

How long can I invest my money in a GIC for?

GICs can also sorted into short-term and long-term GICs. Short-term GICs are simply GICs with terms of less than one year – 30 to 364 days, to be exact. Long-term GICs are sold for 1, 2, 3, 4, 5, 7 or 10 year terms. Short-term GICs typically offer lower interest rates, in exchange for the liquidity of the asset (meaning you could access it sooner). With any term, though, the rule of thumb is that the longer you’re willing to invest your money, the higher the interest rate you’ll receive.

What happens if I need to withdraw my money early?

Financial institutions know that people can fall on hard times or find themselves in financial emergencies; that’s why many people use GICs to fulfill part of their fixed income portfolio. If your money is in a cashable GIC, you can redeem anytime after 30 days (although you may earn less or no interest). With non-redeemable GICs, however, you may not be able to withdraw your money early; this is at the discretion of the bank, as they are under no obligation to let you out of the contract. If you are able to cash out of a non-redeemable GIC early, you may lose all interest earned or have to pay a penalty for early withdrawal.

Is my investment protected?

It depends on how much you invested and/or how long of a term you choose to invest for. Most GICs are protected by deposit insurance, either through CDIC (big banks and many other financial institutions) or through a provincial deposit insurance provider (credit unions). No matter which insurer covers you, only GICs with terms of 5 years or less (nothing over) and up to $100,000 (nothing more) are protected, in the event that your GIC issuer folded.

Why do banks offer GICs?

Generally speaking, banks use the deposits (a.k.a. the money you put in the bank) they get from savers to loan money to borrowers (people who want personal loans, mortgages, etc.). In this regard, a bank acts as an intermediary: it pays an interest rate to a depositor to bring money in, then turns around and lends it out at a higher rate to a borrower. So, GICs are one of the tools banks use to attract funds, in order to make loans.

Why should I invest in a GIC?

As the name indicates, the allure of a GIC is that the principal is guaranteed. Unlike more volatile investments, such as stocks, you won’t be exposed to the possibility of a loss due to market fluctuations, if you invest in a GIC. GICs don’t generally hold the promise of very high returns, however, but are considered safe, conservative investments. GICs can also fulfill the fixed income component of a diversified investment portfolio, which we’ll tell you more about tomorrow.

Flickr: n_corboy