What Does CMHC’s Latest Announcement Mean for Canadians?

I’m going to preface this article with a warning that it involves banking jargon, but will try to distill it to the key takeaways for average Canadians.

Today it was announced in a Globe & Mail article that, effective immediately, the CMHC is limiting banks, credit unions and other mortgage lenders to $350M worth of mortgage-backed securities (MBS) per month under the National Housing Act (NHA). This follows Ottawa’s announcement earlier this year that it would limit mortgage-backed securities that it would guarantee to $85B this year, up from $76B last year.

By the end of July – just 7 months into the year – banks had already tapped $66B of the $85B annual limit, resulting in an immediate need for further intervention from Ottawa.

Mortgage-backed securities function like they sound: they are investments backed by mortgage collateral. Banks and lenders pool mortgages into investment securities insured by the CMHC and then sell units to investors. Because the NHA MBS are insured by the CMHC, the CMHC protects investors who purchase the securities against default. Since the CMHC is a Crown Corporation, Canadian taxpayers are essentially on the hook too – if the CMHC ever ran out of funds, taxpayer dollars would be used to supplement.

Under the National Housing Act Mortgage-Backed Securities (NHA MBS) program, banks have been able to securitize and sell large portions of the mortgages they carry on their books for a lower cost than they otherwise could if they were not backed by the CMHC. Because they come with a low risk, investors require less return, which lowers the cost of funding for banks and gets passed onto homebuyers in the form of lower mortgage rates.

What does this all mean for Canadians?

If you’ve been able to follow this article so far, congratulations, you now understand the most complicated fundamentals of the mortgage industry. If I lost you somewhere along the way, however, know this: the latest CMHC move is both good and bad for Canadians.

On the one hand, limiting CMHC insurance means Canadian taxpayers have less exposure to the housing industry. But on the other hand, Canadian homebuyers may soon be faced with higher mortgage rates, now that banks have less subsidized funding sources.

Other points

While the announcement is likely to impact the big banks, it is less likely to impact smaller lenders and credit unions that would have a difficult time reaching the $350M per month MBS limit. If we look at DUCA Financial Services (one of the five largest credit unions in Ontario), for example, the company only issued 454 mortgages for a total of $97M in all of 2012.

Plus, the CMHC has also introduced a new Canadian Covered Bond Program in the last year, which allows lenders who meet the eligibility criteria to issue covered bonds with non-CMHC insured housing collateral. The bonds are administered by the CMHC but not insured/backed by the CMHC.

Final thoughts

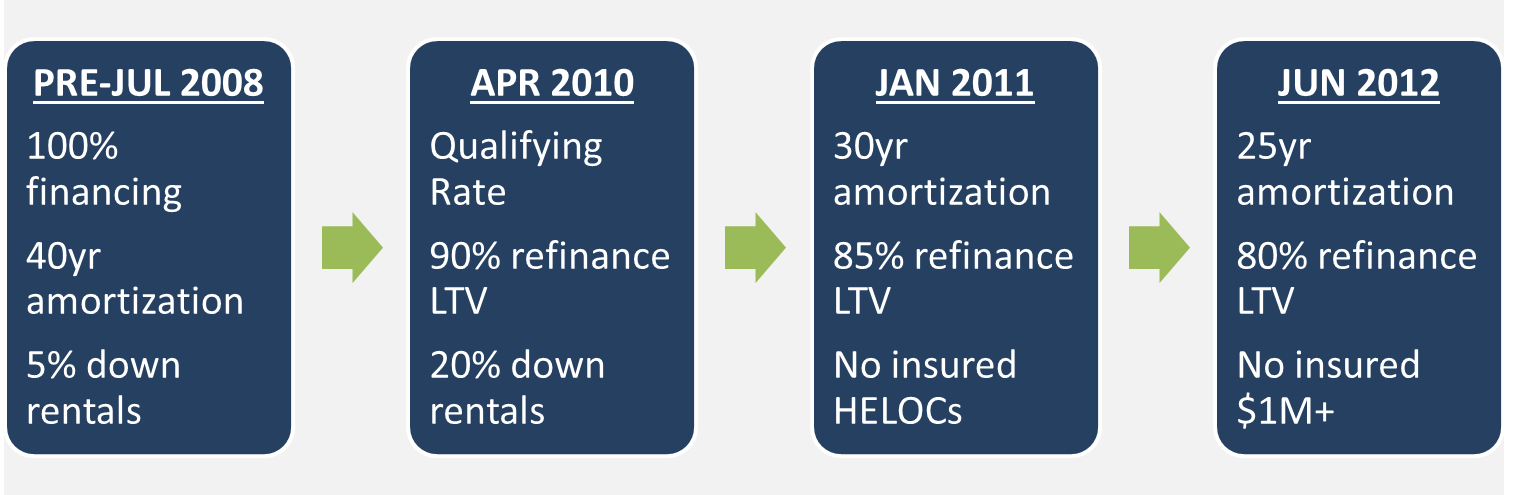

After taking moves to tighten the mortgage market over the past few years, it’s obvious Canadian Finance Minister Flaherty is not satisfied with his results thus far. Is this the last in a wave of changes or are there more to come? Only time will tell.

–KL

Kerri-Lynn (KL) is the Chief Marketing Officer and resident mortgage news commentator at Ratehub.ca.