How to choose between a refinance, a HELOC and a second mortgage

This article was originally published on April 27, 2021, and was updated on August 31, 2023.

A great benefit of owning a home is that it can provide you with some extra cash; it’s possible to tap into equity built up over time, even if you’re still in the process of paying down your mortgage. Compared to other types of credit, such as credit cards and lines of credit, turning your home’s equity into cash can be a much cheaper solution, given mortgage rates are lower than those of other borrowing products.

There are three main ways you can access your home equity. This article will tell you exactly how each of them work.

How to access equity in your home

If you’re considering accessing the equity in your home, you have three methods to choose from:

- Refinance your mortgage to access equity

- Obtain a home equity line of credit (HELOC)

- Take out a second mortgage

There are different qualifying criteria and reasons to choose each method. The first question you need to answer is which option makes the most sense for you. Here’s a quick explanation of each option, with a few pros and cons.

1. Refinance your mortgage to access equity

Refinancing your mortgage involves breaking your current mortgage and starting a new one. Through this process, you have the option to borrow more on your new mortgage than is owing on your current mortgage. That will leave you with cash left over.

Pros: This is a great way to access your home equity at the same rate as your mortgage.

Cons: You’ll pay interest on the cash amount immediately. Refinancing can also incur a break of contract fee, called a pre-payment penalty, on your existing mortgage. You’ll also be re-stress tested as you’ll be moving to a new lender.

2. Obtain a home equity line of credit (HELOC)

A home equity line of credit is a facility on your mortgage that lets you draw out cash as you need it. You will need to already have a HELOC in place to use it. If you don’t have one in place, you’ll have to renew or refinance your mortgage to get one.

Pros: A HELOC is good to have when you think you’ll need access to cash at a later date. You don’t pay interest on the cash until you take it out.

Cons: Home equity lines of credit come with rates that are typically higher than variable mortgage rates, so it's important to shop around for the best home equity line of credit rates available.

3. Take out a second mortgage

A second mortgage is exactly what it says on the box. Instead of refinancing, you can simply take out a second mortgage against the equity that you’ve built up in your home. While you’ll avoid some of the fees of refinancing, a second mortgage is almost always the most expensive way to access home equity, as it comes with higher mortgage rates than your primary mortgage. It’s generally used as a last resort, especially by people with bad credit.

Pros: Allows you to access your home equity without having to re-qualify for a refinance. While more expensive than other mortgages, second mortgages generally have lower rates than credit cards or personal loans, so they can still be used to consolidate debt.

Cons: Second mortgages have significantly higher rates than primary mortgages, as well as refinanced mortgages and HELOCs. Second mortgages are the most expensive way to access your home equity.

Confused about home equity?

Speak to a mortgage broker near you for free, personalized advice

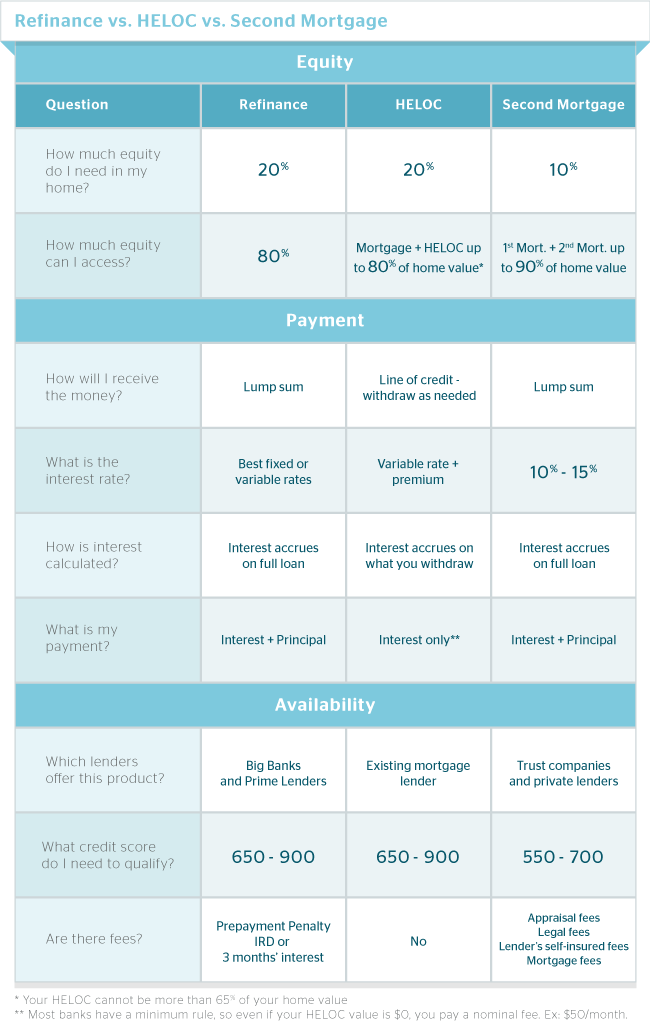

Comparing your home equity options [infographic]

The chart below summarizes the differences between your three options to accessing your home equity. Scroll down and we’ll also look at three case studies that show when each method is the right choice.

Case Study #1: Ruby’s Refinance

Home Value: $800,000

Outstanding Mortgage: $520,000

Current Mortgage Term and Rate: 5-year variable at 6.05%

Years into Term: 3 years

Objective: Access equity for post-secondary school

Ruby wants to access some equity from her home so she can pay for her child’s post-secondary education. She’s decided to refinance her mortgage, because she wants to access a lump sum of money and lock in a better mortgage rate than the one she currently has.

Through a refinance, Ruby can access up to 80% of the value of her home – less what she currently owes on her mortgage. This means Ruby can access a maximum of $120,000 of equity:

Home Value x 80% – Outstanding Mortgage = Available Equity

$800,000 x 80% – $520,000 = $120,000

According to our mortgage refinance calculator, Ruby will have to pay a one-time pre-payment penalty of $7,865 (three months’ interest) to break her current mortgage. However, doing so will give her access to the equity she needs for her child’s education, as well as a lower mortgage rate.

However, Ruby only needs $55,000 for her child’s tuition, and so her outstanding mortgage increases to just $575,000 than the $640,000 it would have become had she accessed her maximum available amount of $120,000. This effectively reduces her monthly payment, from $3,544 to $3,423 because of her new 5-year fixed rate of 5.24%, which will save her thousands of dollars over the remaining term.

It’s important to note that if the pre-payment penalty was too large, Ruby could have considered blending and extending her mortgage instead.

Case Study #2: Harry’s HELOC

Home Value: $800,000

Outstanding Mortgage: $600,000

Current Mortgage Term and Rate: 5-year fixed at 4.34%

Years into Term: 1 year

Objective: Access equity for a kitchen remodel

Last year, Harry bought his first home. Fortunately, he was able to make a large down payment, so he already has a good amount of equity in his home. Unfortunately, his kitchen is seriously outdated and needs a massive renovation.

With the renovation expected to last eight months, Harry has decided to get a home equity line of credit (HELOC) to finance his kitchen remodel. This lets him access equity as he needs it.

Through a HELOC, Harry can access up to 80%* of the value of his home – less what he currently owes on his mortgage. This means Harry can access $40,000 of equity:

Home Value x 80% – Outstanding Mortgage = Available Equity

$800,000 x 80% – $600,000 = $40,000

*It’s important to note that the HELOC amount can’t exceed 65% of the home’s value, but $40,000 ÷ $800,000 = 5%, which is much less than 65%.

Opening a HELOC is a good option for Harry, because the cost of refinancing would be very high. According to our mortgage refinance calculator, he would have to pay a$6,510 pre-payment penalty to refinance.

A HELOC also gives Harry access to a revolving line of credit, so he can borrow money as he needs it throughout his kitchen renovation project. Note that Harry will now have to make a monthly HELOC payment in addition to his existing mortgage payment.

Looking for a great HELOC?

Compare the best HELOC rates available in one place, for free

Case Study #3: Suzy’s Second Mortgage

Home Value: $325,000

Outstanding Mortgage: $260,000

Current Mortgage Term and Rate: 5-year fixed at 3.69%

Years into Term: 2 years

Consumer Debt: $25,000 total on 3 credit cards, all at 19.99%

Objective: Borrow money to consolidate debt

Suzy wants to consolidate $25,000 of credit card debt she has accumulated over several years. A second mortgage is the right choice for Suzy, because her late and missed payments on this debt have left her with a bad credit score.

With a second mortgage, Suzy can access up to 90% of the value of her home – less what she currently owes on her mortgage. This means Suzy can access $32,500:

Home Value x 90% – Outstanding Mortgage = Second Mortgage

$325,000 x 90% – $260,000 = $32,500

Of course, there are some other fees involved, including an appraisal fee, legal fees and second mortgage application fees. But if Suzy could access a second mortgage of $32,500 with an interest rate of 10.00%, she could consolidate her debt at an interest rate much lower than what her current credit cards are charging her. The $7,500 difference ($32,500 – $25,000) can be used to pay the fees.

With a second mortgage, Suzy will now have two monthly payments to make: her existing first mortgage payment and her new second mortgage payment.

The bottom line

When it comes to home equity, there are a lot of options available, and each is right for a particular person at a particular time. Picking the right option for you could save you thousands in interest and fees, so take your time to research each method and speak to a mortgage broker if you have any unanswered questions. You'll get expert, personalized advice at no cost or obligation to you.

Also read: