Monthly Mortgage Update: March 2014

The Canada Mortgage and Housing Corporation (CMHC) dominated mortgage news this month, with notable inclusions in the 2014 Federal Budget, as well as an announcement that it will raise its mortgage insurance premiums effective May 1st, 2014. Otherwise, mortgage rate drops made headlines early in the month, but have since remained steady around the 3.00% mark.

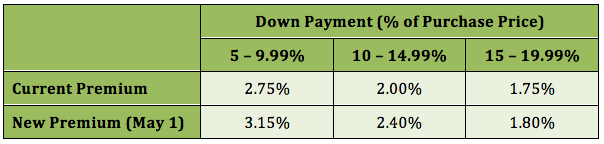

Increased CMHC Insurance Premiums

When the CMHC announced it would increase its mortgage insurance premiums by an average of 15%, the general sentiment in the industry was a resounding shrug. Not only was the move long overdue and expected, Toronto Realtor Mark Savel went so far as to assert that, “the largest effects of the CMHC changes will be felt by coders who will have to update online mortgage calculators“.

Indeed, given the number of mortgage calculators on Ratehub.ca, we have a lot of updating to do.

The mortgage premium increases, which will apply to new mortgages with down payments between 5 and 19.99% (not currently insured mortgages), are summarized in the chart below.

The CMHC assured the change, “is not expected to have a material impact on the housing market”. We ran the numbers ourselves on a $350K mortgage with 5% down, and though the overall premium increases by $1,400, when added to your mortgage and amortized over 25 years, this works out to only $6.99 being added your monthly mortgage payment. For a more detailed breakdown, see our post.

In a press release on Friday, following the announcement, the CMHC’s private competitor, Genworth, announced it, too, would raise premiums across the board by an average of 15%. Genworth’s increases will take effect May 1st, 2014, as well.

Breaking Down the 2014 Fed Budget

There was a lot of information to be distilled in the recently announced 2014 Federal Budget, and much pertaining to mortgages. Here’s a high-level summary of the need-to-knows:

First off, the good news: there are new provisions in place that will bolster small lenders and increase competition in the mortgage industry. And, as you know, increased competition is always a win for consumers. There will be funding improvements and “flexible funding options” for small lenders and more streamlined bank incorporation.

Another positive is that there will be more disclosure requirements on collateral charge mortgages. These mortgages are touted for allowing borrowers to increase their mortgage amounts without needing or incurring lawyer/notary fees, but make it more costly to switch providers at renewal. Translation: you have fewer options at mortgage renewal and are essentially stuck with the rate your existing lender offers you (probably not a competitive one), unless you want to incur a penalty to switch to another lender.

Now to the “bad” news. I put the bad in quotations because, for some, the budget provisions further limit the government’s exposure to the housing market, while others would argue the provisions will translate to less and more expensive mortgage funding and higher mortgage rates.

The CMHC will cut bulk mortgage insurance by 18%, from $11 billion to $9 billion. Bulk insurance is taken out by lenders on mortgages that essentially do not require CMHC insurance (conventional mortgages with down payments of 20% or more). These mortgages are “bulked” together and insured in pools that allow lenders to package them up with less risk and securitize them. James Laird of True North Mortgage says, “lenders can still sell securities backed by pools of mortgages without bulk insurance, but this creates more risk and requires a more sophisticated investor.” With less funders (groups and institutions like pension plans) willing to take on the additional risk, demand should slow and prices will increase. “An increase in funding costs will translate to higher mortgage rates,” Laird says.

The big question mark that remains is whether the government will further intervene with new mortgage rules this year, if the housing market continues to flourish.

Ratehub.ca News

RRSP Deadline

The deadline for making 2013 RRSP contributions is today. You still have time, but not much!

Share Your Mortgage Story

Can you tell us why you selected your mortgage term and share your insights with future buyers? We’re looking for Canadians willing to share their stories on our blog. Email our Editor Cait to volunteer!

Mortgage Monthly Newsletter

Our new monthly newsletter is boasting a 35% open rate with readers clearly enjoying our overview of the best mortgage rates and content every month. Subscribe here.

‘Til next month!

–KL