Lessons Learned From My First Year of Homeownership

Owning a house is exciting. Last October, my wife and I made the big move of purchasing our first home together. The house is something we take pride in, and we want to ensure it has a warm, friendly feeling. That it’s a place when people enter they immediately feel relaxed. Our kids love playing outside, we have extra space to work and live in, and we know that this investment is our own.

In all the excitement, we’ve also gone through a steep learning curve: from discovering leaky windows to figuring out how to repair drywall, there have been countless unexpected adventures in our new residence.

If you’re looking to buy a home, there are always new and unexpected things to learn and discover. Let’s take a look at some of the things I’ve learned during my first year of homeownership.

The unexpected expenses to expect when buying a home

Something will always break, burst or otherwise need repair when you own a home. If you’re purchasing an older home, you can almost be guaranteed that you’ll discover things that need repairing or fixing in your first year. For me, it was discovering that the windows of my house leaked and that the drain trap in my bathtub needed to be changed.

Unless you’re a skilled handyman (which I am not), you’re going to have to pay for someone to come in and repair the issues that you discover. And repairs don’t come cheap. If you’re looking to fix something like windows or doors, be prepared to pay more than you might have been expecting. Because of the pandemic, the cost of lumber and manufactured goods has gone up, and the wait time is going to be a lot longer.

If we were to have the windows repaired before we moved in, we could have anticipated paying about 5% less for the total cost. We also could have expected them to be installed a lot sooner. As it is, the wait time for materials has been about 5 months.

Here are some tips for first-time homebuyers to help with unexpected expenses:

- Pay for a home inspection: even if you’ve already moved into your house, a home inspection can help you identify potentially problematic areas. By having a trained professional examine your house, they can point out things that might need addressing in the near future – as well as things that need immediate attention – so that you can budget accordingly.

- Set up a dedicated savings account: having a separate bank account solely for home repairs will help you out in the long run. Have a portion of every paycheque deposited into this account, and quietly your savings will grow. You might not get a great interest rate on the amount you set aside (even if you use something like a high-interest savings account), but you can be assured that when problems arise, you’ll have part of the funds readily available to use.

- Look into government rebates: when you discover that things will need repairing or replacing in your home, take a look at what kind of government rebates and incentives are available. Both federal and provincial governments offer a variety of rebates for energy-saving repairs and renovations, so you might be able to save a few dollars by applying to the specific programs.

- Make YouTube your friend for simple repairs that can cost a lot if you hire someone to do it. These include drywall patching, basic plumbing (cleaning out your P-trap, replacing a faucet), basic electrical (know how to turn off the breaker to the switch before you work on it, otherwise, it can be simple)

On Property tax (and other first-year homeowner taxes)

Something to keep in mind when purchasing a home is that you’ll also have to be paying property taxes on a yearly basis. Each municipality has a different property tax rate, so research the rate where you live before purchasing a house. And keep in mind that property taxes are based on the assessed value of a home, not what you paid.

In Canada, the city with the lowest property tax rate is also one that has the highest-priced homes.

Vancouver, BC had a property tax rate of 0.24683% in 2020, or $1,234 on a $500,000 property.

Saint John, NB had the highest rate, at 1.78500%, meaning you’d pay $8,925 in taxes for the same valued property.

The city in which I live is taxed at a rate of about 0.7777%, putting it in about the middle range of tax rates.

TIP: if purchasing your first home, be sure to find out if you’ll need to pay individual taxes – like school and water – on top of your property tax. This will affect your bottom line.

While the overall amount you pay in property taxes might not be substantial, it’s a good idea to set aside some money throughout the year so that this payment doesn’t come as a shock. If possible, figure out what your property tax is going to be for the year, then divide it by twelve. Set this amount aside each month, and when it comes time to pay the taxes, you won’t have to give it a second thought.

You can also pay your property taxes with your mortgage payments through your lender.

READ: Should you pay your property taxes through your mortgage lender?

Understanding mortgage amortization

When you get a mortgage, you’re taking a loan out from the bank. They want this money back. That much should be obvious. The amortization period of your mortgage is the length of time it will take you to pay it off.

While this might not be a new concept, you really start to perceive the amortization period differently once you have a mortgage. That’s because when you’re looking for the best mortgage rate, you need to consider the mortgage’s term as well.

When you get a mortgage, you will lock into a rate at either a fixed or variable rate. Fixed-rate means you’re locked into paying a certain amount of interest for the term, variable rate means that you pay whatever the market interest rate is over the term.

The term is the length of time that you’re going to be locked into your mortgage contract. At the end of the term, you re-negotiate the interest rate with the bank or shop for a new rate with another bank or a mortgage broker. Thus, if you have a twenty-year fixed-rate mortgage with a five-year term, there will be four terms, and at the end of each term, you’ll work with your existing lender or a mortgage broker to get the best rate at the time. At the end of the four terms (on a 20-year amortization), your mortgage will be paid off (assuming you keep up your payments or negotiate for a longer amortization, pull out equity for renovations, etc.). If you want to check out how different amortization period lengths can affect your monthly payments over time, Ratehub's amortization calculator is a very useful tool.

When we got our mortgage, my wife and I opted for a fixed-rate mortgage. We did this because the interest rate was the lowest it had been in ages and wasn’t expected to dip any lower. If we wanted to gamble, we could have chosen a variable rate mortgage, but the chances are that it would only increase over the term. In hindsight, in 2021, the variable has proven to be lower, but the rate we got is still low and we can afford the payments.

DID YOU KNOW?: If you choose to go with a variable rate mortgage, you’re free to lock into the rate and change to a fixed-rate mortgage at any time. Though, it’s a little bit more than the variable rate you’re paying.

I want to pay my mortgage off early

This could be a dream of mine, and it’s something I’m working towards. I’m a person that doesn’t like to have debts hanging over me, and because with any new mortgage you’re basically only paying the interest on my mortgage for the first few years, it’s not very attractive to me.

READ: Why paying off your mortgage early may not always be the best idea

Wait – what is that about only paying the interest?

That’s right. When you get a mortgage, your loan balance is going to be quite high. For that reason, most of what you’re paying the lender is the interest on the loan (and property taxes if you worked that with your lender). As time increases, the loan balance will decrease, until eventually, you’ll reach the sweet spot where the balance shifts, and you start paying more towards the principal than the interest – but that’s still a long way off.

Back to paying off the mortgage early

There’s a right and a wrong time to pay off your mortgage. And that all depends on your contract. Certain mortgages allow you to increase your regular mortgage payments, but only by pre-designated amounts. Some might not let you increase them at all. If you do increase the amount you pay, you might not be able to lower it back down until you negotiate your next term. So this might not be the best idea if you’re at the beginning of a mortgage and suddenly find yourself wanting to pay more money.

Your other option is to make a lump sum payment. Again, when you can do this depends on your mortgage contract, so you’ll want to review the document before taking any steps. Some mortgages allow for payments only at specific times, some might only let you make a lump sum payment at the end of the term or end of each year.

If you choose either of these options, be aware that there can be prepayment penalties that occur if you pay over the amount that your mortgage contract allows. As you might have figured out – you want to pay close attention to the terms of your mortgage contract, as there are specific regulations you might not have considered before. It’s why you want to shop for more than just a low rate on your mortgage. If all you want is to make steady payments with no changes, focus on the rate. If you want to double up payments or make lump sum payments, consider speaking with a mortgage broker to help you.

As a way to help pay off our mortgage a little earlier, my wife and I have gone with an accelerated bi-weekly payment plan: instead of paying monthly, we pay every 2 weeks, regardless if there are 4 or 5 weeks in a month. This means that more money ends up being applied to the principal, and less money to the interest. It may not make a huge difference, but every dollar counts when it comes to paying off debt.

TIP: In order to help accelerate our mortgage payments, I’m also stashing away extra money whenever I can into a separate savings account. This way, when I’m able to make a lump-sum payment, I can put down whatever extra money I have and help chip away at the principal.

Making a down payment

Before a bank will give you a mortgage, you have to make a down payment of some kind. Consider this an act of good faith – the lender wants to know you have some money so that they can trust you’ll pay off your whole mortgage.

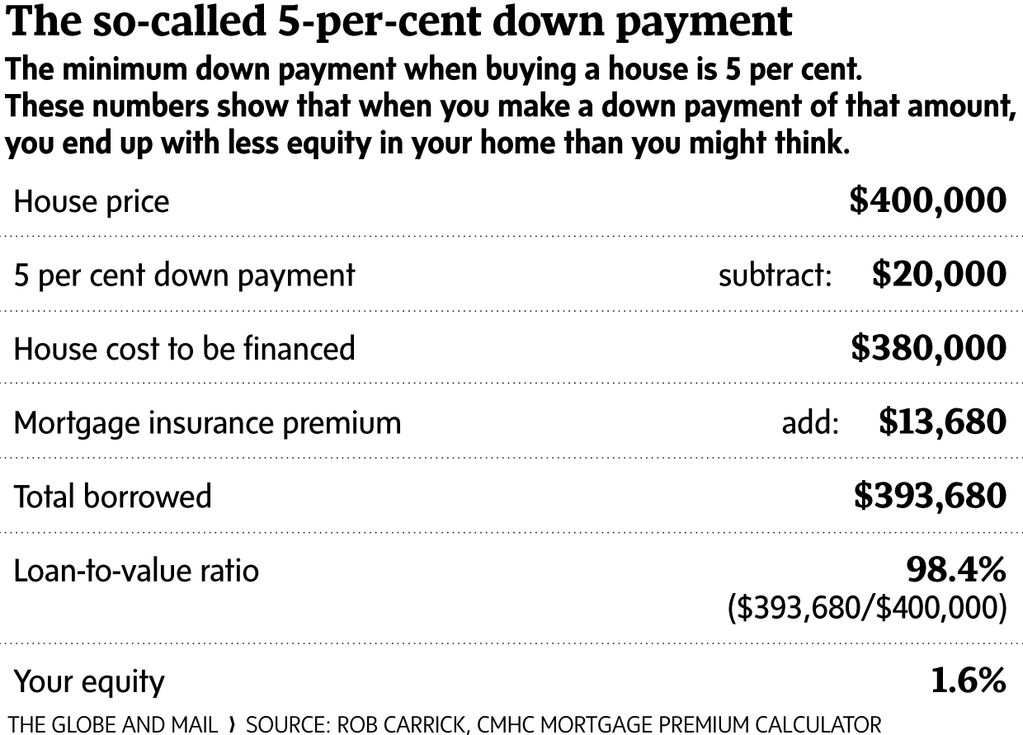

The down payment you make is a percentage of the sale value of the home. If the purchase price is less than $500,000, the minimum down payment you have to make is 5% (with CMHC insurance). If it’s over $500,000, you pay 5% on the first $500,000, then 10% on any amount over that. If the purchase price is over $1 million, you’re going to have to pay a down payment of 20%.

READ: Can I afford a million-dollar home?

While making a down payment of 5% might sound like a good idea, you have to consider a few things. A lower down payment means you’re going to be paying more interest on your mortgage. Also, with a down payment of only 5%, the maximum length of a mortgage contract you can get is 25 years. And to make that attractive 5% down payment even more expensive in the long run, any down payment of less than 20% requires you to have mortgage insurance. This insurance gets tacked on to each payment you make, therefore costing you more out of pocket.

When considering what you can afford to spend on a house, you really need to think about what your mortgage payments will be. If you can, calculate how much you have for a down payment, then figure out what 20% that amount is. That way, you can find out the maximum amount you can afford without having to worry about paying for insurance or high-interest rates.

Don’t forget house insurance, property taxes, utility bills like electricity, water, and gas, either.

The bottom line

Buying a house is a long-term responsibility. Not only are there a lot of day-to-day expenses you need to consider, but you also need to be sure to have enough money tucked away to pay off your monthly mortgage fees. When considering a mortgage, be sure to take the time to use our mortgage calculator to forecast what your payments will be. Shop around for the best mortgage rate possible, and speak with a mortgage specialist to get their insights into the market.

Do you have recent experience getting or paying off a mortgage? Let us know in the comments.