Is now a good time to start investing?

- Passive investing is a popular investment strategy used by many to build wealth.

- It’s more about buying and holding broadly diversified funds that track the markets, not actively trying to beat the market.

- Inflation causes your purchasing power to go down.

- The markets go up in the long run.

- Time in the markets beats trying to time the markets.

- Robo-advisors and self-directed investing are better options than investing in mutual funds.

You don’t have to be good at math, interpret fancy charts, and know Wall Street terminologies to invest in the stock market. The mainstream media makes you believe you need a finance degree to be an investor, but it’s not the case. Ordinary Canadians can, and many are, already investing on the stock market. Now is as good a time as any to begin investing if you’re trying to build long-term wealth.

By “investing”, I’m referring to passive investing, which is a proven strategy for building long-term wealth. It’s buying and holding assets for long periods of time, not trading stocks everyday. Most passive investors buy index funds to track specific markets, such as the world’s total stock market or S&P500. These funds are well diversified and less risky compared to investing in individual stocks. Here’s what you need to understand to start investing today.

High interest savings vs. investing

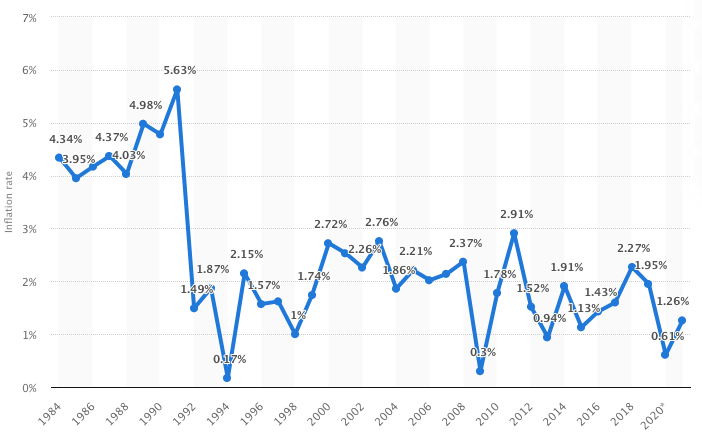

Inflation makes the money you have today worth less tomorrow. Assuming you’re able to save $10,000 in a high interest savings account earning 2% interest each year. After one year, your $10,000 would earn you an extra $200 in interest from the bank. A good deal considering you take no risk and you get $200.

But, the prices of goods and services that you consume go up each year due to inflation. In other words, the prices you pay today are not what you’ll pay in the future making the $200 you made, worth a little less.

A look at historical inflation rates in Canada. Adopted from Statistica.com

High interest savings accounts preserve the value of your money but aren’t effective for building wealth. To build wealth, start investing. Understand that whenever you invest you’re also assuming more risk, but this comes with the possibility of a higher reward. This is why you can expect to get more money by investing versus saving.

Perhaps it’s riskier to not invest because inflation ensures that you lose if you do nothing.

The markets move upward in the long-run

We may be in the midst of a down-market but this doesn’t mean you shouldn’t invest.

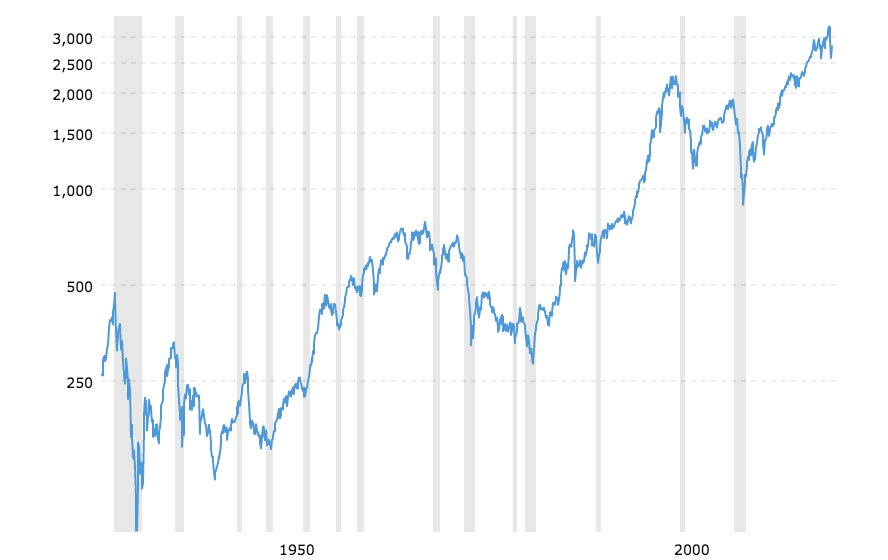

The whole point of investing is to build wealth and keep your money from losing value. Based on historical data, the stock market’s average annualized returns for the S&P 500 Index was 11.69% from 1973 to 2016.

So, buying the S&P 500 index in 1973 and holding until today, despite the market crashes during the period, the value of your investments are still worth more than your original investment. It’s because the economy grows, values of stocks on the indexes increase, dividend payments, and compounding interest.

After each crisis, the markets rebounded and went on to reach all-time highs.

S&P 500 Index – 90 Year Historical Chart. Source: macrotrends https://www.macrotrends.net/2324/sp-500-historical-chart-data

For first-time investors, down-markets present a great opportunity to buy indexes and stocks at a cheap price. You can take advantage of panic selling and negative sentiment towards the market. You don’t need to wait for down-markets to begin investing. The truth is, it’s hard to know when the market is going down or be at an all time low for you to buy-in. Trying to time the market isn’t a smart idea because as your money sits on the sidelines you’re missing out on profits you could be getting.

Even if you invest at market peaks, when prices are at an all time high, unless you sell your assets, you can still win. When the markets are down, you only lose when you sell. It’s all because you’re locking in your losses.

The market goes up and down on a daily basis but over time it trends upward. The time you spend in the market is more valuable than trying to time buying into the market. To further illustrate the point, there’s a story about Bob, the world’s worst market timer. Before many stock market crashes, Bob would invest large sums of money, and despite what many think, he made out fine in the end. If you’re still a disbeliever, to see all the data make sense, you can read Bob’s story, “ World’s worst market timer.”

Ready to start investing?

I hope my writing is convincing enough to know now is the best time to begin investing. The most valuable advice is to not panic, practice discipline, and keep a diversified portfolio. You’ll beat inflation and maximize your profit. If you’re ready to begin investing, there are a few options available to you:

Robo-advisors

Robo-advisors are great if you want to invest but don’t have the confidence to start. Robo’s charge a small annual fee, usually between 0.3-0.5%, which is added to the cost of underlying exchange traded funds (ETFs) in which they invest your money. The fee scales with the amount you invest with them, but at least your money is put to work for you.

Discount brokers

Discount brokers are a good option if you are fee conscious and want to manage your investments. You have to know the ETFs in which you want to invest and place the trades yourself. If you are considering this option, I recommend Questrade. Questrade lets you buy ETFs for free and they give you access to a rebalancing tool to help you manage your investments. I consider them to be the best brokerage in Canada for passive investors.

Mutual funds

Mutual funds, which the big banks offer, are another option, but beware of their high fees. In Canada, mutual funds have an average management fee of 2%. With mutual funds, you’re paying your banks’ asset managers to try to beat the market. Many professional investors underperform, with only a select few who consistently beat the market. It’s why passive investing is so popular, and with inflation, mutual funds hardly seem worth it.

The bottom line

In closing, whatever option you chose please keep the following in mind:

- Don’t invest if you have high interest debt.

- Build an emergency fund before you start investing

- Never have all your eggs in one basket (i.e. stocks) remember to diversify

- Stick to your plan and don’t panic when markets are down

- Have a long-term outlook when building wealth

- Be mindful of fees, they can eat a huge chunk of your nest egg.

This article is a guest contribution from Brendan Lee Young of Passiv. Passiv is portfolio management software that makes DIY investing easier. It integrates with your brokerage account and you automate your portfolio management. With Passiv users can invest and rebalance their portfolios in one-click.