[Infographic] Toronto Mortgage Affordability: 1985 vs. Today

The average house price in Canada has gone up substantially in recent years, rising from approximately $331,000 in 2010 to nearly $449,000 today. At the same time, mortgage rates are at very low levels, allowing Canadians to buy houses at prices that would’ve been prohibitive at historically “normal” interest rates.

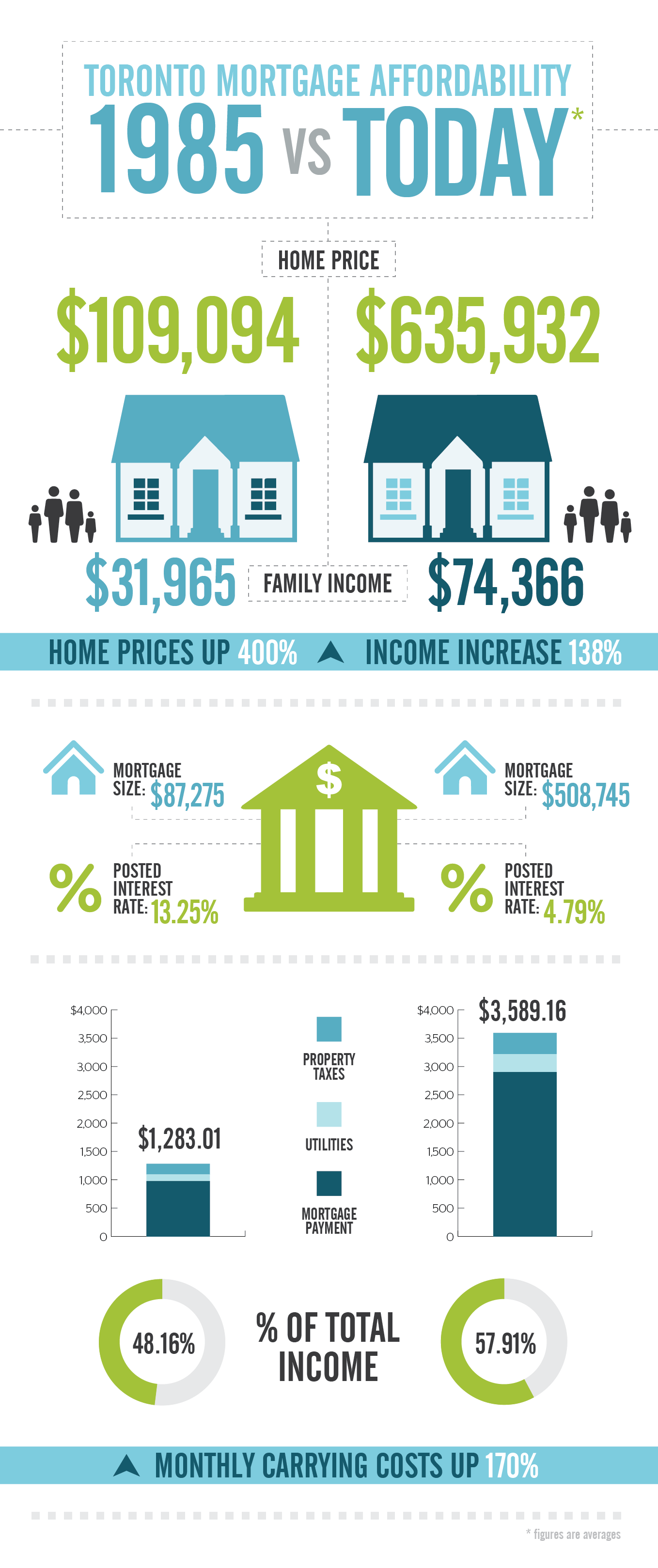

We decided to take a page from a recent National Post article and look at the monthly carrying costs of buying an average-priced house in Toronto now versus in 1985. At that time, house prices were much lower but price alone doesn’t paint the full picture. Monthly carrying costs – driven by interest rates – should also be considered.

The following diagram shows the changes in home price, monthly carrying costs and what percentage of income is required to carry the average home in Toronto. See our notes at the end of the post for details on methodology.

What can we conclude from this 1985/2015 comparison?

First, house prices have risen much faster than income. Second, mortgage rates today are significantly lower than in 1985. It’s because of the latter fact that people are now able to carry such huge mortgages. Yet even with the low rates, total monthly carrying costs as a percent of income still comfortably exceed the level seen in 1985 (57.91% vs 48.16%).

The above chart pertains to the average home sold in Toronto. Of course, the average house price is a blended statistic, taking into account detached and semi-detached houses as well as condos.

So how does the current affordability of condos and detached houses compare to 1985? RBC Economics recently studied this issue and here’s what they found:

- For a standard two-storey house costing $725,600 in Q4 2014, 65.6% of median pre-tax income went to monthly carrying costs, versus an average of 54.3% since 1985.

- For a standard condominium costing $362,600, 33.9% of median pre-tax income went to monthly carrying costs, versus an average of 31.2% since 1985.

Not surprisingly, it’s the detached housing market where affordability is really stretched. Monthly condo carrying costs are slightly above their long-run average but not nearly as much as two-storey houses.

—

Notes on assumptions and methodologies:

- The median down payment in Toronto is roughly 20%. Keep in mind that anything less requires mortgage default insurance.

- Posted and discount mortgage rates can differ substantially. For example, as Ratehub.ca data shows, a 5-year fixed rate of 2.43% is available currently. However, we’ve used the posted rate to be conservative and to make an apples-to-apples historical comparisons.

- Utilities figures are estimates.

- For property tax figures, we’ve used the average home price assessment for 2014 and multiplied this by the average residential tax rate. Note that the assessment value is much less than the average selling price. For 1985, the figure is taken from a Toronto Star article that appeared in 1986.

- We’ve omitted one-time costs such as the land transfer tax and legal fees.