How Much Do You Have to Make to Afford to Live In a $1000/sq. ft. Toronto Condo?

Despite year-over-year home prices falling, condos continue to boom in the Toronto real estate market.

Unlike every other market segment, condos are increasing in price, rising 7.1 per cent in the 416 this March compared to the same time in 2017, selling for an average price of $590,184.

For that price, prospective buyers may be inclined to skip Toronto houses and look at houses for sale in Hamilton, a city less than an hour door-to-door from Toronto, where large, detached houses with backyards are actually going for less, at just $565,000.

But we all know that die-hard urbanites aren’t going to be happy in Hamilton. Instead, they’ll do anything they can to stay in the downtown core.

The condo lifestyle is a win

Many prefer the condo lifestyle: the maintenance is taken care off, everything is shiny and new and the gym is just an elevator ride away. The added bonus of being close to all the best restaurants, transit and taxis, shopping and their work, are benefits just too hard to give up. Since so many hotels now have “residences” attached, some condos even now include maid service, a bar downstairs and a spa that you don’t even have to go outside to reach.

But the price is steep for the best conveniences and amenities.

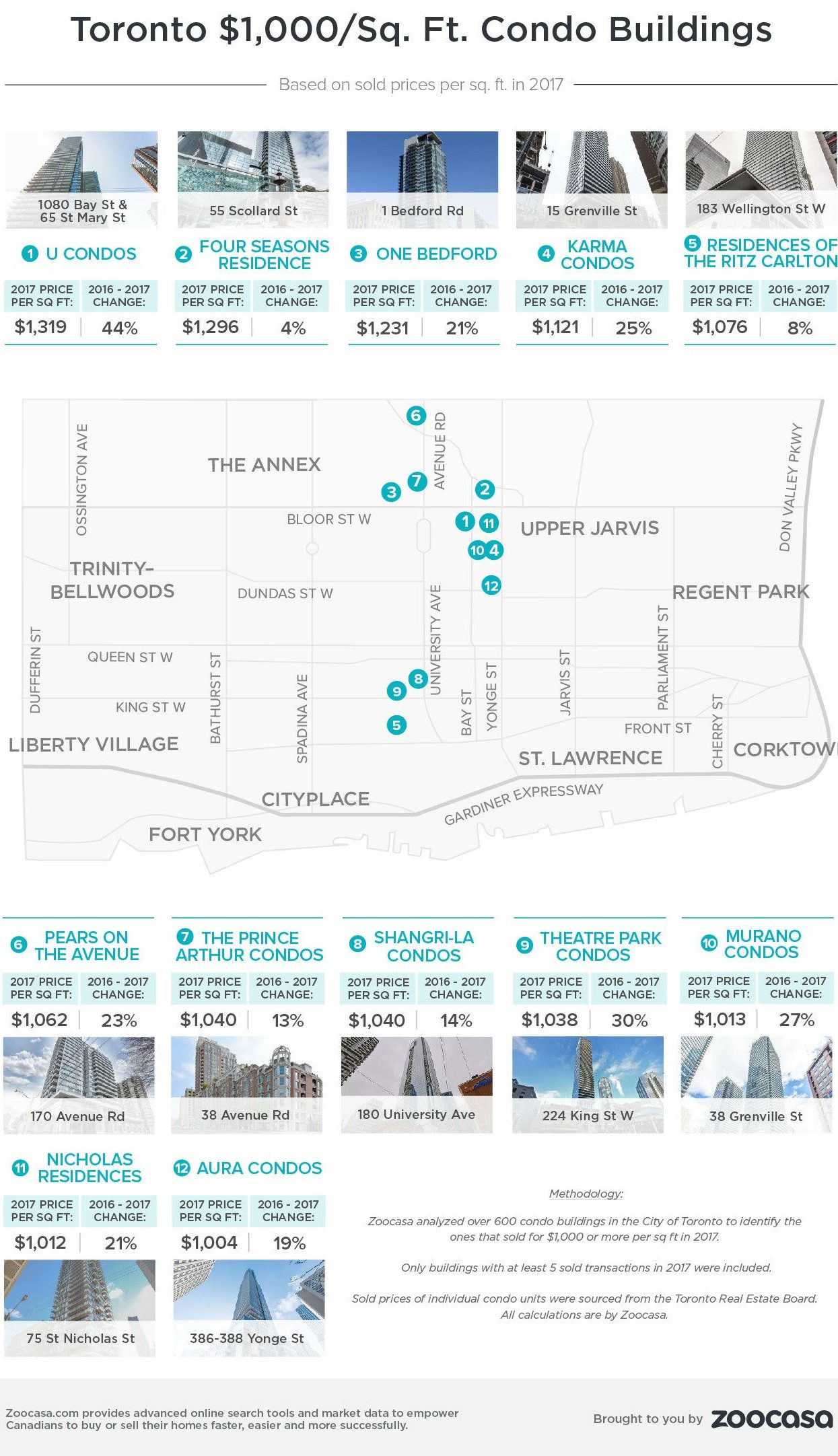

There are at least a dozen condo buildings in Toronto that cost $1,000 or more per square foot, all near Yonge Street or Avenue Road, south of Dupont.

Compare today's top mortgage rates

Looking for a great mortgage rate? Check out the lowest mortgage rates available

Space is a premium

Since developers are building units so small these days, the overall purchase price isn’t that much more compared to a unit elsewhere. Essentially, buyers are proving willing to squeeze into less space.

Let’s take the most expensive condo on the list Zoocasa compiled, (infographic below): U Condos on Bay Street, selling for an average of $1,319 per square foot in 2017.

We’d like to see how much one has to be making in order to avoid being house poor and being certain of getting a mortgage.

Their condos range in size from a tiny 324 square feet, all the way to a massive 2,938 square foot.

How much do you have to make to pay for a $430,000 unit?

Let’s say someone wants to start off in the smallest, studio condo on offer, for $427,356.

Our prospective buyer is willing to forgo a bedroom to be in this neighbourhood, near the University of Toronto, Yorkville, and all the hospitals. He wants to put 20 per cent down, amortize for 25 years and manages to get a five-year fixed interest rate of 3.49 per cent.

That means he’ll be putting down $85,471 right off the bat for a remaining mortgage of $341,885.

Monthly mortgage payments will be $1,705. But of course, we must add both maintenance fees and property tax as outlays.

Maintenance fees (to pay for the sauna, gym, air conditioning, the concierge and an outdoor garden), are roughly $250 for a unit of this size, while property tax is $195.

That totals $2,200 monthly before any internet or hydro is factored in.

The new, tighter mortgage rules

Now, because of the new OSFI — the bank regulator — rules put into place this January 1, it’s far harder to qualify for a mortgage than just last year.

Canadian Housing and Mortgage Corporation recommends that housing expenses not exceed 32 per cent of one’s gross income.

So, to see if these monthly housing expenses of $2,200 are affordable, we multiply them by 3.32. We can see our borrower must gross $7,304 each month, or $87,648 annually to comfortably qualify for a mortgage for this unit.

But OSFI feared, that should interest rates rise — as they have already done a quarter of a percentage point this year — buyers won’t have enough income to cover their mortgage. The risk that they will default, or have less money to spend in the economy, will rise.

Higher incomes needed to reduce risk

To counteract this risk, OSFI devised a stress-test: borrowers must be able to afford a mortgage should rates rise.

Therefore, all federally regulated banks must ensure that borrower’s income can support a mortgage at the contract rate plus 2 per cent, or the Bank of Canada’s rate, whichever is higher.

Whereas last year, our buyer’s income could have qualified on the mortgage rate he was actually able to get — 3.49 per cent — he must now be qualified at 5.49 per cent. (Despite only having to pay the contracted rate.)

This brings the monthly mortgage he would be required to afford to $2,085 from $1,705. Plus the same maintenance and utilities, he would need to be able to handle monthly housings costs of $2,530.

When we multiply this monthly housing cost by 3.32, we see that our buyer must be making a monthly income of $8,400, or $100,800 annually to afford this condo.

Thus, for the smallest unit in this building, borrowers should be making over $100,000 a year.

Photo by Scott Webb on Unsplash