What Homebuyers and Variable Rate Mortgage Holders Should Know About Prime Rate

Flickr: daryl_mitchell

For months, homebuyers and homeowners across the country have been wondering if and when rates, and subsequently payments, would go up for variable rate mortgage holders. Just yesterday, Finance Minister Jim Flaherty said that Canada would be facing global pressure to raise interest rates in 2014. While Bank of Canada Governor Stephen Poloz has show no signs that he would raise interest rates this year, there’s nothing saying there couldn’t be a Bank of Canada interest rate hike in 2015. If you’re worried about how high rates could go, a lesson on the history of Prime rate might help put you at ease.

What is Prime Rate?

Technically, Prime rate is the interest rate that banks charge their best customers. In practice, though, it’s more useful to think of it as a benchmark that gives you an idea of the spread between the bank’s borrowing cost and its return from lending, as well as how good a customer the banks thinks you are.

Let me explain. Prime rate is tied to the Bank of Canada interest rate, the rate at which the central bank wants to see the banks lend to each other overnight. The key interest rate, in other words, shapes the banks’ short-term cost of borrowing. In Canada, the key interest rate has been at 1.00% since September 2010. Prime rate, on the other hand, currently sits at 3.00%, which yields a 2.00 percentage point spread. Now, the rate the bank will charge you for borrowing money is generally a percentage above or below the Prime rate, depending on things like your credit rating, income and pre-existing debt levels, as well as — that’s right — your negotiating skills.

Prime Rate and Variable Mortgages

When it comes to mortgages, Prime rate is the basis for variable rate mortgages. Fixed rate mortgages are, in general, long-term loans correlated to the banks’ long-term costs of sourcing funds, which is tied to the yields on Canada Bonds. The interest on variable rate mortgages, then, generally fluctuates with short-term rates. The interest rate banks offer on fixed rate mortgages, on the other hand, depends on long-term rates.

Now, short- and long-term rates do not necessarily move in unison. Recently, for example, long-term rates in Canada and the U.S. have climbed a bit, but short-term rates, which the BoC and the Federal Reserve control directly, are expected to stay very low at least until the end of 2014; that’s why variable rate mortgages are so attractive right now. The obvious catch, though, is when short-term rates do rise, so will the monthly payments on any adjustable rate mortgages.

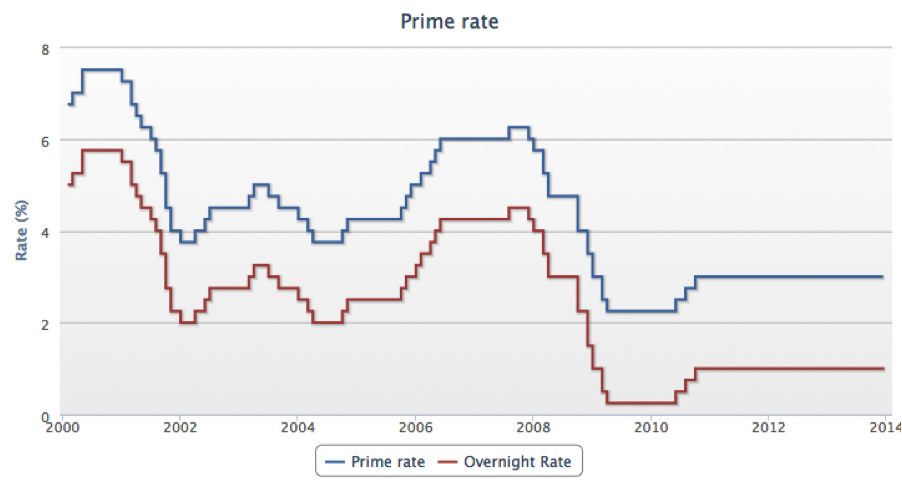

So, how far up could short-term rates go and how fast? You’d think the answer would depend on the key interest rate, which the BoC raises when the economy is growing and inflation is rising, and lowers when economic activity is slowing and inflation is cooling – and that’s correct. But Prime rate has, at times, swayed a little from the pattern of the key interest rate.

The History of Prime Rate and Lessons for the Future

As you can see in the chart above, the spread between Prime rate and the key interest rate (otherwise know as the overnight rate) hasn’t always been 2.00%; that’s because it’s up to the banks to decide whether or not to follow the BoC’s lead.

In December 2008, for example, when the BoC slashed its overnight rate from 2.25% to 1.50% at the height of the financial crisis, Canada’s big banks did not entirely follow suit. Instead, they cut their Prime rate by only half a percentage point, rather than 0.75%, amidst worries about high financing costs. Banks, then, do have some discretion over whether to pass on rate cuts or hikes to their customers.

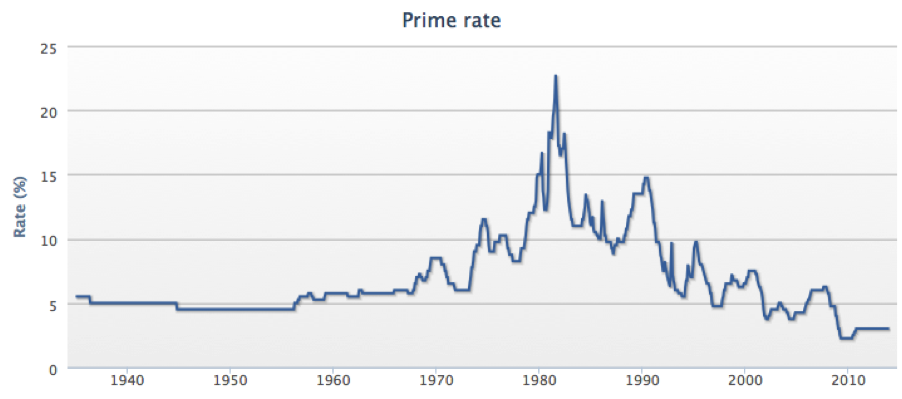

Another telling graphic is the one that charts the pattern of Prime rate all the way back to 1935, when it, along with the BoC, came into being.

Having looked at it, you’re probably wondering two things: (1) Could rates possibly stay low for 20-some years, as they did between 1935 and 1956? And (2) Could they ever return to the 1981 high of 22.75%?

The answer to (1) is easy: Disregard anything that happened that far back. The way the financial system and monetary policy worked at the time has little in common with the way things work now. The key interest rate back then was the Bank Rate – a rate the BoC charged to lend to financial institutions – and from 1935 to 1956 it was fixed. Besides, banks used to be subjected to credit controls, such as a 6% cap on the interest rate on bank loans that was lifted only in 1967.

The answer to (2) is a bit more nuanced. The obvious thing to note is that inflation in Canada in the late 1970s and 1980s was very high, peaking at 12.50% in 1981. Prime rates above 20%, then, reflected the efforts of the BoC to battle these runaway price increases: the key interest rate reached 17.14% in February 1981. Today, with inflation running at 1.20% on a year-over-year basis, well below the BoC’s 2.00% inflation target, we’re in no danger of seeing those rate hikes any time soon. The worry, right now, is that inflation is too low – not too high.

Another reason why Prime rate is very unlikely to return to prior peaks — and why it’s been at unprecedented lows since the financial crisis —is that banks nowadays face much fiercer competition to narrow the spread between the key interest rate and Prime rate. Until 1967, Canadian banks had been able to act as a cartel in setting rates, rather than competing to attract customers with cheap loans and mortgages. Large companies – the banks’ so-called wholesale customers – have much more latitude to raise funds outside the traditional banking system. Banks need to keep Prime rate low, in order to lure these big clients. Also, banks have started charging us fees for service costs they once used to cover through higher interest rates. And finally – though this is not an exhaustive list – since 1980, banks have been allowed to have mortgage loan subsidiaries that could raise deposits without having to hold reserves against them; this increased the supply of funds banks could lend out, allowing them to charge lower interest rates to borrowing customers.

There is little question that, in a year or two, short-term interest rates will start to go up. Everything, though, seems to indicate that the coming climb will be a slow and gradual one – all the more reason to read up on Prime rate, and do your due diligence on the opportunity-cost of those cheap variable rate mortgages.

This post was written by freelancer Erica Alini for Ratehub.ca. Erica is also a contributing writer at Maclean’s and Canadian Business. You can follow her on Twitter.

Also read: