Gifting GICs: Be Aware of the Tax Implications

Let’s say you have a 15-year-old child and want to help him or her start an investment portfolio at an early age. You decide to purchase a 3-year $5,000 guaranteed investment certificate (GIC) in the child’s name, earning 1.50% compound interest annually. In some respects, this is a wonderful thing to do, not to mention generous.

This type of strategy is common among parents and grandparents, but many people are not aware of the tax implications of gifting a GIC to a child.

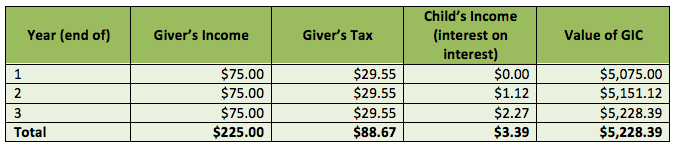

Even when the child is technically the owner of the GIC, for tax purposes, some of the income generated by the investment is deemed to be in the hands of the parent or guardian who made the gift; this is referred to as “attributed income”. In our example, the $5,000 GIC @ 1.50% interest would earn $75/year in non-compounded interest. It is this amount which is considered to be “first generation” interest income of the parent, not the child.

However, any “interest on interest” that the GIC earns is considered so-called “second generation” income and is taxed in the hands of the child. (In our chart below, we assume that the GIC earns compounded interest. We’ve shown how much is attributable to the parent ($75/year), and how much is attributable to the child (interest on interest). Attributed income must be reported on the GIC giver’s taxes every year until the child turns 18. At this point, they are considered an adult and must report all interest earned on the investment as their own income.

Why give a GIC to a child in the first place when you can just buy the GIC yourself? The key advantage is that the second generation income is reported on the child’s taxes and, unless they’re a music or acting prodigy earning Justin Bieber-esque money, odds are their tax rate will be much lower than yours (indeed, they probably won’t pay any taxes at all unless they have other income).

In the following chart, we break down the giver’s interest earned and taxes paid for the scenario we described at the beginning. We’ll assume that the giver of the GIC lives in Ontario and pays tax for the year 2015 at the 39.41% marginal tax rate. The calculations are done under the assumption that the rate stays the same for the next two years. Let’s also assume that the child does not have enough total income to exceed the basic personal exemption amount, thus, he or she will not pay any taxes on the GIC interest income (i.e. the interest on interest).

As financial advisor Kevin Dorey writes, there are a few ways to get around the “attribution” rule (i.e. the fact that interest income is taxed as if it were earned by the adult who gave the GIC). One option is to give the child cash instead of a GIC. The child can then buy the GIC, if they wish to. Second, money for a GIC can be loaned to the child at acceptable market interest rates (it cannot be an interest-free loan). Third, you can simply wait until the child is 18 before gifting them a GIC; this will avoid the hassle of finding out that your generosity will also result in a payment to the CRA.

Flickr: Josey