CMHC housing stats: First Quarter 2012

The Canadian Mortgage and Housing Corporation (CMHC) is the leading provider of mortgage loan insurance and authority on Canadian housing policy and programs. Every quarter they release a report on the state of the Canadian housing market and its direction. With so much talk of a housing bubble in Canada, the CMHC collects information and makes forecasts that can add perspective to the conversation.

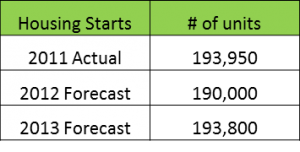

Canadian Housing Starts

In November of last year, the CMHC forecasted 2012’s annual housing rate to be 181,000 units. They’ve since increased their latest projection to 190,000 housing starts with this latest report, which isn’t too far off from 2011’s housing start numbers (194,000). By 2013 though, the housing agency expects the numbers to rise back to 2011 levels. Overall housing starts will decrease slightly in production this year, but will vary greatly in different regions across Canada. CMHC expects the provinces west of Ontario to show positive growth, whereas anything east of Ontario, including Ontario itself, will see a contraction.

Data from CMHC

The real question is whether Western Canada will have enough demand to meet the amount of supply hitting the market in the coming future. CMHC believes the rental vacancy rate in BC, Alberta, and Saskatchewan will decline this year due to factors such as new migration and job creation. According to the Globe and Mail, the top four Canadian cities with the highest rates of population growth over the last 5 years are Calgary, Edmonton, Saskatoon, and Kelowna (in that order).[1]

What does it mean?

With high average home prices, strong housing production, and low Canadian mortgage rates in the western provinces, the ingredients for a market correction are present. But if a correction does occur, it is likely to be a ‘softer correction’. Douglas Porter, the deputy chief economist at BMO says that “while the report’s warnings should not be dismissed as completely improbable, it’s clear that the market is backing off bubble territory as price increases subside.” He went on to say, “Given the rebound we’ve seen in employment in the last year in Canada and the fact that interest rates are still at extremely favourable levels, I can’t get that pessimistic on the outlook for housing”. [2]

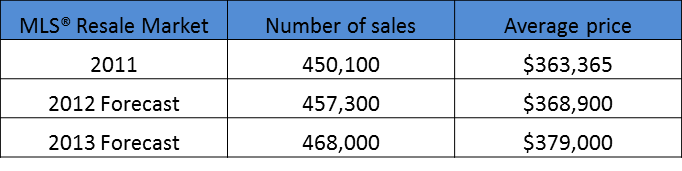

Canadian Home Prices

The concerns over a housing market crash has forced Ottawa to keep a close eye on the housing industry, but CMHC believes balanced market conditions will remain in most local markets. The CMHC also expects the average MLS® price to remain relatively stable in balanced market conditions, assuming mortgage rates remain flat before they start increasing moderately in late 2012 or early 2013.

What does it mean?

The Canadian housing market is currently in a balanced state and the meteoric rise of home prices has already started to wane across most regions. According to CTV, Canadian homes will continue to remain affordable because mortgage rates are hovering at historic lows, but home affordability could change if rates start to rise.

Mortgage Rate Outlook 2012

CMHC is forecasting that posted 5-year fixed mortgage rates will not hit a ceiling higher than 5.40% this year and 5.90% next year. Currently, the four of the top five biggest banks in Canada (CIBC, BMO, RBC, and TD) list their 5-year fixed posted rates at 5.24% and offer discounts equal to 120 basis points or 1.20%, for a discounted 5-year fixed rate of 4.04%.

Mortgage rate forecast for discounted 5-year fixed rates [CIBC, BMO, RBC, and TD only]:

CMHC also believes variable mortgage rates will remain near historic low levels over the same period.

What does it mean?

Most economists, including the Canadian Mortgage and Housing Corporation believe Canada will remain in a low mortgage rate environment for the next one to two years. That gives a one to two year buffer for borrowers to pay down their mortgages and increase their equity, so if rates eventually do rise, they’ll be in better standing with their mortgage debt by then.

[1] The Globe and Mail [2] CTV BC