How Cash Back Mortgages Work and Who Offers Them

When buying a home, some homeowners might want to buy all new furniture, complete a home renovation or two, or simply have a safety net of cash for the first few months of homeownership. For many, though, the thought of having extra cash when purchasing a home is nothing more than a dream. Fortunately for those people, some lenders offer something called a cash back mortgage which can help make that dream a reality.

With a cash back mortgage, you receive a lump sum cash rebate when your mortgage closes, commonly around the 5% mark – though it can be anywhere from 1.00% to 7.00%, depending on which lender you choose. The rebate is tax-free and can be used for almost any purpose, such as to pay for closing costs, complete renovations, buy furniture or pay down other high-interest debts.

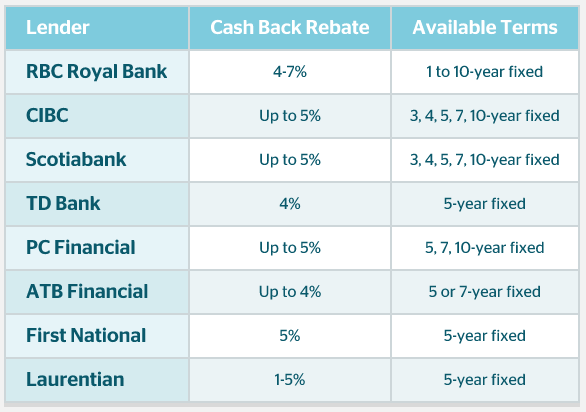

Which Lenders Offer Cash Back Mortgages

Many Canadian lenders, including RBC, CIBC and TD Bank, offer cash back mortgages with varying terms. Take a look, then let’s run some examples of how it works:

How Cash Back Mortgages Work

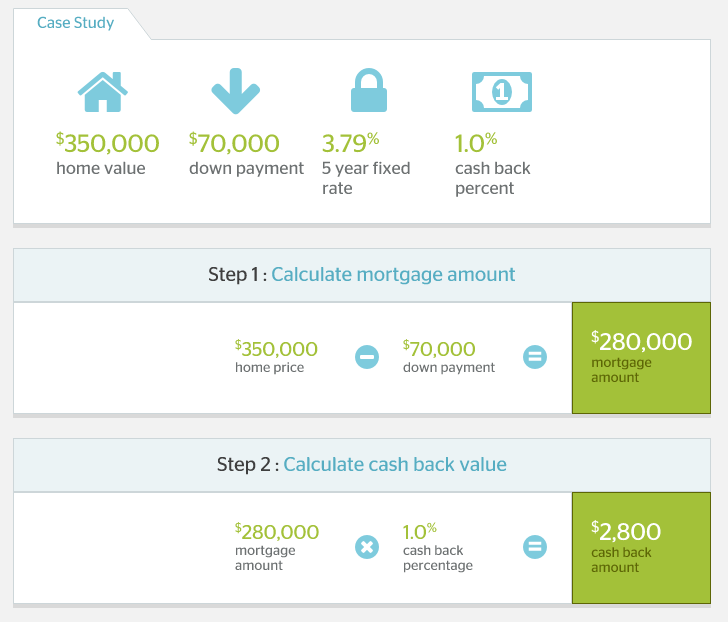

To see how a cash back mortgage works, here’s a simple example. You purchase a home for $350,000 and put down 20% ($70,000) to avoid CMHC insurance, which means you need to borrow $280,000 via a mortgage loan from the bank. If the lender you chose offers a 1.00% cash back mortgage product, you could get a $2,800 ($280,000 x 1.00%) cash back rebate when your mortgage closes and use that money for whatever you want.

What the Cash Back Rebate Will Cost You

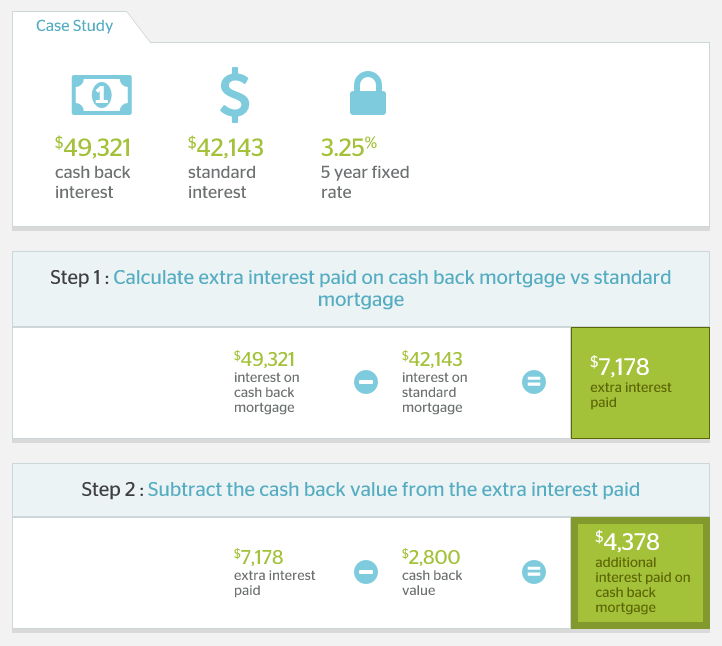

The one downside of cash back mortgage products it that they always come with a fixed mortgage rate, and the interest rate is slightly higher than what’s available for standard (non-cash back) mortgage products; this means you’ll pay more interest over the life of your mortgage, to compensate the lender for letting you borrow extra money from them.

If we continue with the same example above, because you chose the cash back mortgage product with a rate of 3.79% vs. your lender’s standard 5-year fixed mortgage product at 3.25%, you would pay your lender an additional $4,378 over 5 years – and that’s after you deduct the $2,800 cash back rebate you received from them.

What Happens if You Break Your Term Early

What Happens if You Break Your Term Early

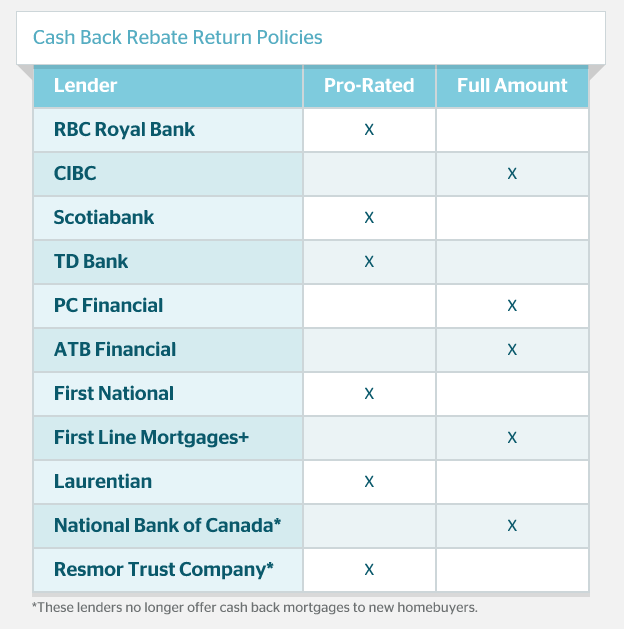

Additionally, if you need to refinance your mortgage or break your mortgage term early, you may be on the hook for a portion of your cash back rebate (a pro-rated amount based on how many months you have left in your term). Some lenders even require you to pay back the amount in full. See below.

If we continue with the example above, let’s say you had to break your mortgage 3 years into your 5-year term. Your lender originally gave you a 1.00% cash back rebate amounting to $2,800, which they now want a pro-rated amount of returned, in addition to any prepayment penalty.

With 2 years (24 months) left in your 5-year (60 month) term, you would need to pay back 40% (24 / 60) of the cash back amount you received; that’s $1,120.

While a cash back mortgage might not be an ideal choice for everyone, it can be a great option for a buyer who needs a little extra money while making such a large financial transaction. If you don’t mind the higher interest rate that comes with it, a cash back mortgage can help you pay for any number of things or simply boost your cash flow during the first few months of homeownership.

Flickr: kinematic