CMHC to Increase Mortgage Default Insurance Premiums on June 1, 2015

Effective June 1, 2015, the Canada Mortgage and Housing Corporation (CMHC) is going to increase its mortgage default insurance premium rates.

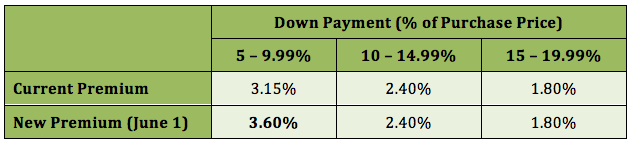

CMHC insurance, as it’s otherwise known, is mandatory insurance put in place on all high-ratio mortgages – those with down payments of between 5 and 19.99% of the purchase price of a home. The insurance protects lenders, in the event that a borrower defaults, and now it’s going to cost buyers who need it just a little bit more.

The CMHC insurance premium is a small percentage of your mortgage amount, which is then added back to your mortgage and paid off over the life of the loan. This video explains how CMHC insurance is calculated:

On June 1st, the premium for down payments of between 5 and 9.99% of the purchase price of a home are going to increase by approximately 15% – from 3.15% to 3.60%. The increase will only apply to new owner-occupied mortgages, self-employed mortgages and 1-4 unit investment property mortgages, and willnot apply to mortgages that are currently insured by CMHC.

While the increase looks dramatic, it will only result in an increase of approximately $5 per monthly mortgage payment for the average Canadian homebuyer who has less than a 10% down payment.

For example, let’s say that today you bought a home with only 5% down, after which you needed to take on a $350,000 mortgage. Because you put down between 5 and 9.99% of the purchase price, your CMHC insurance premium would be:

$350,000 x 3.15% = $11,025

If you waited until after June 1st to purchase that same home, and still put down only 5%, your new CMHC insurance premium would go up to:

$350,000 x 3.60% = $12,600

With the new CMHC insurance rate, your premium would increase by $1,575 ($12,600 – $11,025), which would be added to your mortgage and paid off over the life of the loan. If you took out a 5-year fixed term at 2.79% and amortized over 25 years, your monthly mortgage payment would increase by $7.29.

Now, even though mortgage default insurance costs buyers extra money, it’s actually beneficial to the market. Without CMHC insurance, lenders would increase mortgage rates because the risk of default would increase. Lenders are able to offer lower mortgage rates when loans are protected by mortgage default insurance because the risk of default is spread across multiple homebuyers.

The decision to increase CMHC premium rates was made so the Crown Corporation could meet its target capital requirements. The new premiums are not expected to have an impact on the housing market.