CDIC: Everything you need to know about how your money is federally insured

This post is sponsored by the CDIC.

As you go about your daily banking online or watch the ATM dutifully swallow up your deposit envelope, have you ever stopped to wonder just how safe your hard-earned money really is? Canadians are lucky to have a stable and reliable banking system so we don’t tend to spend a lot of time considering just how the banks we’ve come to trust and depend on actually safeguard our savings.

The fact is that behind Canada’s banking scene, an organization plays a vital part in protecting our deposits and our country’s financial system: the Canada Deposit Insurance Corporation.

About CDIC – A quick history

The Canada Deposit Insurance Corporation (better known as CDIC) is a federal Crown corporation that insures the money you deposit in eligible accounts at over 80 member financial institutions.

Think of CDIC as your bank’s insurance provider.

It was established by the Canadian Parliament in 1967 to protect deposits and thus increase consumer confidence in the banking industry and promote the stability of Canada’s economy and financial institutions.

Though the CDIC is a Crown corporation it’s not publicly funded. Funding is provided by premiums paid by member banks to CDIC to protect their clients’ deposits. Coverage is free and automatic for Canadians who bank at a member of the CDIC.

CDIC’s mandate is to protect deposits in the event a member financial institution fails and must be restructured or closed. If a member institution closes, you’ll have access to your insured funds within days.

Since its founding in 1967, CDIC has handled 43 bank failures and closures that affected over 2 million accountholders. But no Canadian lost a single dollar of deposits protected by CDIC.

What (and how much) is covered by CDIC?

All eligible deposits (see below) are protected by the CDIC for up to $100,000 (including principal and interest) per coverage category, per member institution. There are specific parameters that govern what type of account is covered.

Eligible deposit (cash and term deposits)

The following products are covered by CDIC:

- Chequing or savings accounts

- Deposits held in foreign currencies

- Money orders, certified cheques and bank drafts issued by CDIC members

- GICs and term deposits

These deposits are eligible for CDIC insurance even when they’re held in a registered account such as a Tax-free savings accounts (TFSAs), Registered-Retirement Savings Plans (RRSPs), or Registered Retirement Income Funds (RRIFs).

Up to $100,000 in coverage

It’s important to understand exactly how CDIC insurance works.

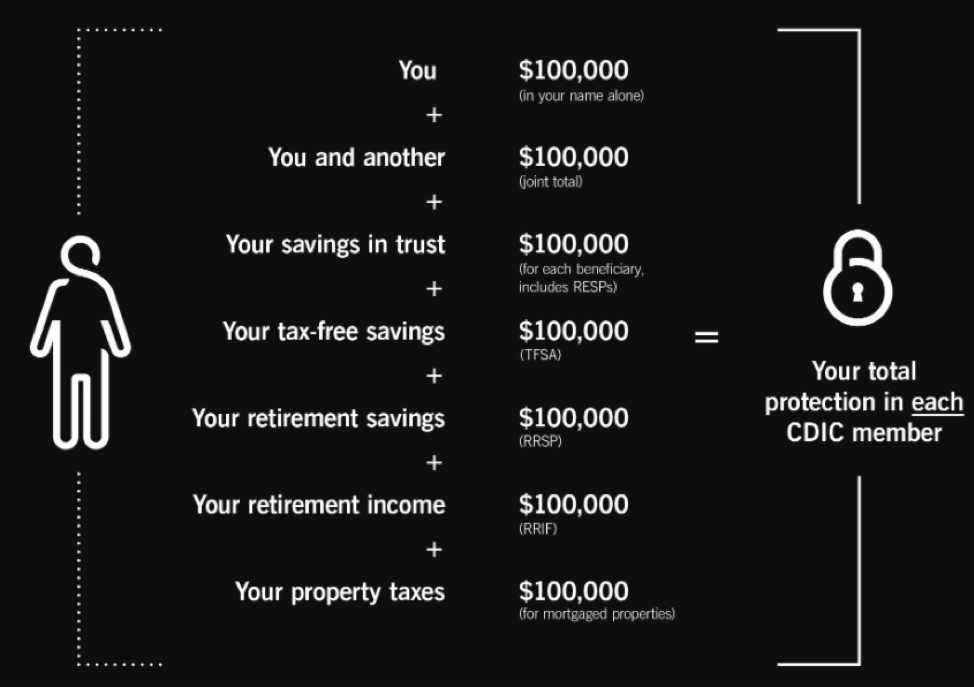

CDIC coverage is broken down into seven different eligible deposit categories. Eligible deposits are insured in each category to $100,000 at each member institution. The categories are:

- Deposits held in one name

- Joint deposits (accounts held in more than one name)

- Deposits held in trust for another person

- Deposits held in Registered Retirement Savings Plans (RRSPs)

- Deposits held in Registered Retirement Income Funds (RRIFs)

- Deposits held in Tax-Free Savings Accounts (TFSAs)

- Deposits held for paying property taxes on mortgaged properties (note that as of April 30, 2022, deposits in mortgage tax accounts will no longer be a separate category but will be combined with eligible deposits in other categories)

In short, you’ll receive up to $100,000 in coverage per category, per member institution. And categories are based on how the account is held (i.e. whether it’s a TFSA or a Joint Account) not the type of deposit (i.e. whether it’s a chequing or savings account).

How coverage works within the same member institution:

Let’s say you have a chequing, savings, and GIC account – all held under your name at the same CDIC member bank.

Since all three deposits fall under one category (“deposits held in your name”) and are all held at the same bank, you’d be entitled to a total of $100,000 in coverage across all account types combined.

That said, if you were to also open a joint savings account at the same member bank, the joint savings account would fall under its own category and coverage would apply as follows:

- $100,000 in total coverage for your chequing, savings account and GIC, as these all fall under the category of “deposits held in one name”

- A separate $100,000 in coverage for the Joint Savings Account, since it’s under a different category of “Joint Deposits”

How coverage works when holding accounts with more than one CDIC member:

Let’s say you have a savings account at Bank A with $100,000 and a GIC at Bank B with $50,000.

In this scenario, all the money in these accounts would be fully protected – provided both banks are CDIC members.

That’s because you’re eligible to receive at least $100,000 in coverage on the deposits you hold at each individual CDIC institution you bank with.

What doesn’t CDIC cover?

The following accounts are not protected by the CDIC:

- Mutual funds, stocks and bonds

- Exchange Traded Funds (ETFs)

- Cryptocurrencies

- Travellers’ cheques (as of April 30, 2020; member institutions no longer issue Travellers Cheques)

- Deposits with financial institutions that are not members of the CDIC (like most credit unions, which are provincially protected)

Calculate your CDIC coverage

To recap: CDIC covers eligible deposits up to $100,000 per insurance category, per member institution. If you’re still uncertain about which of your deposits are covered and by how much, the CDIC website features an easy-to-use calculator to measure your coverage.

CDIC Members: Which financial institutions are federally insured?

Over 80 financial institution in Canada are CDIC members. Click the dropdown below to see a list of all members.

<strong>View all CDIC Members (+/-)</strong>

What happens if a CDIC Member closes its doors?

As mentioned previously, since its inception, the CDIC has overseen 43 bank failures. The CDIC’s goal is to protect the economy and the flow of financial services, while minimizing the risk to taxpayers. When a bank is no longer viable, the CDIC’s role is not restricted to closing an institution. It can also support a sale of shares or assets, restructure the bank, oversee an amalgamation with another institution and more.

When deciding what approach to take, the CDIC considers factors, such as the size of the bank, whether it has franchise value and the possibility of private sector solutions.

You can find more details on the official CDIC website here.

2020 changes: CDIC coverage expanded

In 2020, several changes were introduced to modernize the Canada Deposit Insurance Corporation. As of April 30, 2020, the CDIC expanded coverage to include deposits held in foreign currencies. Previously there was no protection for these kinds of deposits. Note that foreign deposits are not a separate category but are new ‘eligible deposits’ and would fall under whichever of the coverage categories they are deposited in.

Another big change, as of April 30, 2020 is that the 5-year term limit on GICs and other term deposits was removed. Term deposits of more than five years now fall under CDIC protection.

To read more about other changes to CDIC coverage, visit the official website and register for CDIC’s Annual Public Meeting webcast to be held on August 11, 2020 at 1:30 – 2:15 PM ET.

CDIC’s Annual Public Meeting webcast

![]()

![]()

-

- August 11, 2020 at 1:30 – 2:15 PM ET

- The Board of Directors of the Canada Deposit Insurance Corporation (CDIC) is pleased to announce that its 2020 Annual Public Meeting will be held via live webcast. The bilingual meeting will highlight how CDIC’s recent changes have improved deposit insurance.