How Your Down Payment Really Affects Your CMHC Insurance

Flickr: dolmansaxlil

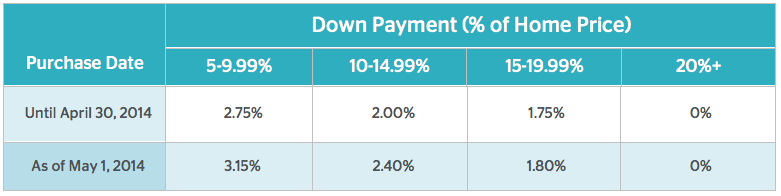

On May 1st of this year, the Canada Mortgage and Housing Corporation (CMHC) increased their mortgage default insurance premiums. Mortgage default insurance, which is more commonly known as CMHC insurance, is required of buyers who make a down payment of between 5-19.99% when they purchase a home. The new premiums went up by approximately 15% on average for all down payment scenarios, as follows:

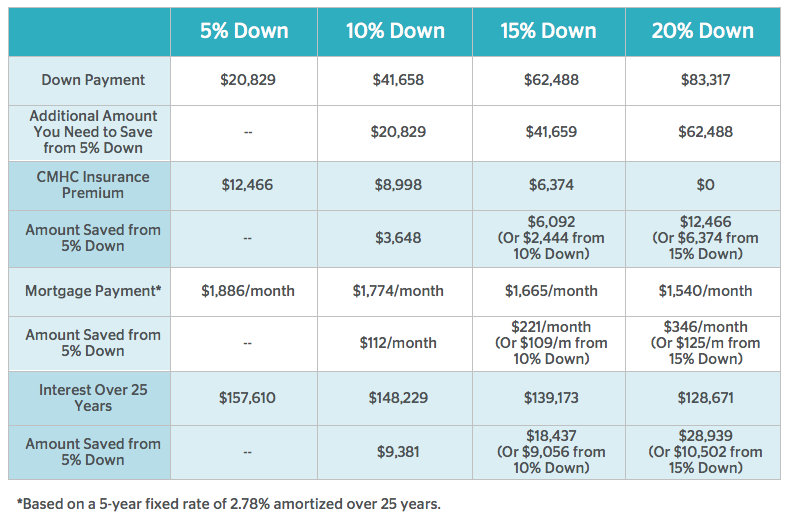

Unfortunately, this information doesn’t do much in terms of educating future homebuyers. The biggest question we hear from readers, friends, and even real estate agents is that buyers want to understand how their down paymentreally affects their CMHC insurance – and the monthly payments and interest costs that follow. To answer that question, we plugged the current national average home price ($416,584) into our mortgage payment calculator. Here’s what we can tell you:

5% Down Payment

The minimum down payment you can make in Canada is 5% of the purchase price of your home. If you can only afford to put down between 5-9.99%, you will be subject to the highest CMHC insurance premium (3.15% of your purchase price after you’ve made your down payment). In this example, if you wanted to put down 5%, you would only need to save $20,829 to buy the home but your CMHC insurance premium would be $12,466; that’s the equivalent of 3% of the purchase price ($12,466 / $416,584), which means you’re basically only putting down 2%! Your CMHC insurance premium is then added to your mortgage and paid off over the life of your loan, which is why your mortgage payment and total interest costs are highest in this scenario.

10% Down Payment

If you’re trying to decide between putting 5% down and 10% down, the answer is that you should always aim to put down more. In this example, you would need to save double the amount of money as if you’d only put down 5%, but your CMHC insurance premium would lower to $8,998; that’s only 2.2% of the purchase price ($8,998 / $416,584), which means you’re essentially putting down 7.8%. By putting down 10% instead of 5%, you’d shave off $3,648 from your CMHC insurance premium, $112 from your monthly mortgage payment amount and $9,381 from the total interest costs. Those numbers may not sound like a lot upfront, but the decreased mortgage payment amount could be the buffer you need in your new homeowner’s budget.

15% Down Payment

The differences between putting 10% down and 15% down are a little bit smaller than between 5% and 10%, however, the numbers still add up. In this example, you’d need to save triple the amount of money as if you’d only put down 5%, but your CMHC insurance premium would lower to just $6,374; that’s nearly half of what it would be with only 5% down, and is only 1.5% of the purchase price ($6,374 / $416,584), which means you’re basically putting down 13.5%. Now, by putting down 15% instead of 10%, you’d shave an additional $2,444 from your CMHC insurance premium, $109 from your monthly mortgage payment and $9,056 from your total interest costs. Like we said, those differences are a little smaller than if you’d put down 10% instead of 5%, so if you’re trying to decide between a 10% down payment and a 15% down payment, the choice may not be as easy.

20% Down Payment

Of course, if you’re able to save and put down 20% or more of the purchase price of your next home, you don’t need to worry about any of this. As soon as you hit the 20% mark, you are no longer required to purchase CMHC insurance – that’s a savings of $12,466 from the 5% down payment scenario in this example. If you have 15% saved already, the answer to whether or not you should wait to save and put down 20% becomes obvious. By putting down 20% instead of 15%, you’d shave off an additional $6,374 from your CMHC insurance premium (and go down to $0), $125 from your monthly mortgage payment amount and $10,502 from the total interest costs. See? The differences between putting down 20% versus just 15% are larger than any of the other scenarios already discussed in this example.

So, what’s the best option? You know that the more you can put down, the less you’ll pay in interest costs. And if you can put down 20% or more, you’ll avoid CMHC insurance altogether. However, if you’re trying to decide between putting down 5%, 10% or 15%, the answer may come down to how much each amount will shave off your CMHC insurance premium and monthly mortgage payment amount. If you’re trying to decide between 5% and 10%, 10% is the better option. The answer become less clear when trying to decide between 10% and 15%, as the change in numbers is slightly less (but still significant). However, if you already have 15% saved, there’s no doubt you should try to save and put down 20% instead; the difference is greater than in any other scenario, and it will always leave you with more money in your pocket, which is something every homeowner needs.