How Do RRSP Withdrawals Work?

Update: On April 11, 2024, the Federal government announced an expansion to the withdrawal limit for the RRSP Home Buyers’ Plan, to $60,000 from $35,000. This will go into effect on April 16, 2024. This is the second time the withdrawal limit has been increased since it was introduced in 1992; it was last updated from a limit of $25,000 in 2019.

The new measure will also extend the amount of time home buyers have before they need to start making repayment instalments, to five years from the current two, for those who make HBP withdrawals between January 1, 2022, and December 31, 2025.

Check out our blog to learn more about the government’s announcement.

Okay, so you’ve heard about RRSPs and how great they are. You know that they offer some amazing tax benefits and that they’re pretty much essential if you want to maximize your retirement savings. (They’re called Registered Retirement Savings Plans after all!) But how exactly do RRSP withdrawals work?

Withdrawals are a common source of confusion when it comes to RRSPs, and not knowing the rules can definitely cost you. But don’t let that stop you from getting one! In the following post, I’ll outline exactly how withdrawals work so you can get the most out of your RRSP.

When can I withdraw from my RRSP?

If you thought you had to wait until you retire to withdraw from your RRSP, you’re mistaken. Investments can be withdrawn from your RRSP at any time, but when you do make a withdrawal, those funds will be treated as income in that year.

What does that mean? Those funds will be taxed at your marginal tax rate, just like any other income you make that year.

What happens when I withdraw from my RRSP?

Let’s take a look at an example to see exactly what happens when you make an RRSP withdrawal.

Let’s say you make $73,000 a year and your top tax bracket is currently 32.98%. You decide to make a $10,000 withdrawal from a High Interest Savings Account within an RRSP.

Here’s what would happen:

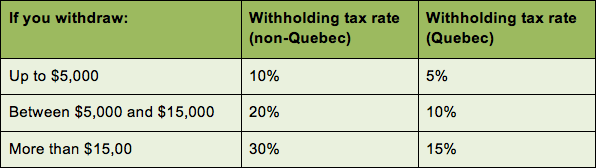

- Immediately

- Withholding tax applied: $10,000 @ 20% = $2,000

- Much like when you receive a paycheque from your employer, the bank would immediately apply a withholding tax on the withdrawal. For this amount in Ontario, the tax applied is 20%.

- At tax time

- Marginal tax rate applied: $10,000 @ 32.98% = $3,298

- At tax time, your marginal tax rate would be applied to the withdrawal, and if there’s a difference, you’ll have to pay that, or you’ll receive a tax refund.

- You owe

- Amount owed at tax time: $3,298 – $2,000 = $1,298

- In this example, you owe an additional $1,298 at tax time (since 32.98% > 20%).

Contribution room

The other important consideration to make before making an RRSP withdrawal is that you will lose your contribution room. That’s right, this contribution will be gone—permanently. This is in contrast to TFSAs, which allow you to add withdrawn funds back in the following year.

When is the best time to make an RRSP withdrawal?

Remember: the basic idea behind RRSPs is that they are a tax deferral strategy. In addition to the tax-free growth of your investments, they allow you to avoid paying taxes on your investments now and instead pay taxes when you withdraw your investments from the RRSP.

So, while you can withdraw money at any time, you’ll maximize tax savings by putting money into an RRSP when you’re in a high tax bracket (in your working years), and withdrawing the money when you’re in a lower tax bracket, (like retirement).

Special withdrawal programs

Is there any way to withdraw without a tax burden? Luckily, the government offers a couple special withdrawal programs to help you with some key life purchases.

- Home Buyer’s Plan: The first is the Home Buyer’s Plan. This allows you to withdraw up to $25,000 per spouse from your RRSP to buy a home. You don’t have to pay tax on this withdrawal immediately, and you have a total of 15 years to pay it back. Basically, 1/15 of the withdrawal is due back per year (beginning in the second year after your home purchase), otherwise you will pay tax on the amount due that year.

- Lifelong Learning Plan: The second is the Lifelong Learning Plan. This allows you to withdraw $20,000 per spouse for education. You can withdraw $10,000 per year, and you have 10 years to pay it back. Like the Home Buyer’s Plan, 1/10 of the withdrawal is due back per year (beginning in the fifth year after your first withdrawal or your first year out of school), otherwise you will pay tax on the amount due that year.

I hope I’ve given you more confidence when it comes to RRSP withdrawals. If you take one thing from this article, just remember to carefully consider the tax implications of an RRSP withdrawal before making one. And of course, don’t forget that with any withdrawals—whether you’re taking advantage of a special withdrawal program or not—you are sacrificing the potential growth of the investments.

Do you have questions about RRSP withdrawals? Will you withdraw from your RRSP to buy a home or fund education? Let me know in the comments or tweet us @RateHub!

Flickr: Ken Teegardin